Question: Problem 2 (Challenge). Asset Pricing (16 points) Assume that the CAPM holds. Assume also that there are only two risky assets in the economy,

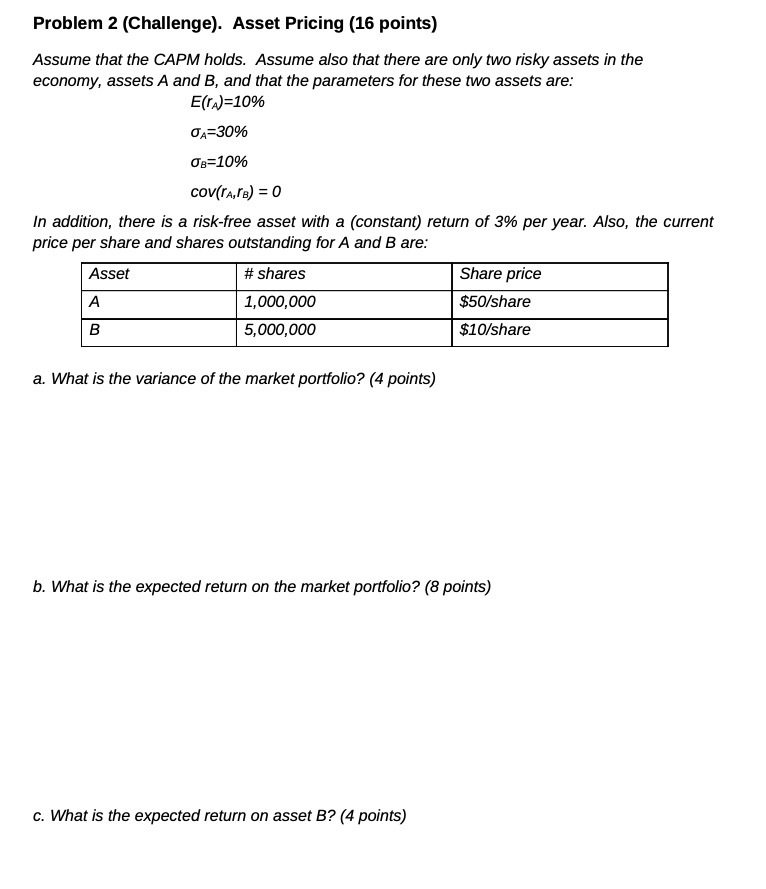

Problem 2 (Challenge). Asset Pricing (16 points) Assume that the CAPM holds. Assume also that there are only two risky assets in the economy, assets A and B, and that the parameters for these two assets are: E(TA)=10% A-30% 08-10% Cov(rA, B) = 0 In addition, there is a risk-free asset with a (constant) return of 3% per year. Also, the current price per share and shares outstanding for A and B are: Asset A B # shares 1,000,000 5,000,000 Share price $50/share $10/share a. What is the variance of the market portfolio? (4 points) b. What is the expected return on the market portfolio? (8 points) c. What is the expected return on asset B? (4 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts