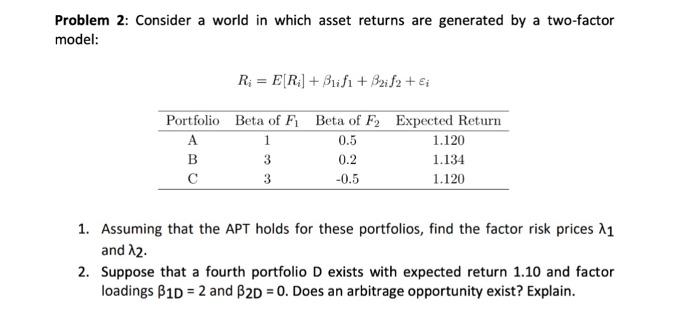

Question: Problem 2: Consider a world in which asset returns are generated by a two-factor model: R = E[Ri] + Bifi + B2if2 + Ei Portfolio

Problem 2: Consider a world in which asset returns are generated by a two-factor model: R = E[Ri] + Bifi + B2if2 + Ei Portfolio Beta of F Beta of F Expected Return A 1 0.5 1.120 B 3 0.2 1.134 3 -0.5 1.120 1. Assuming that the APT holds for these portfolios, find the factor risk prices and 2. 2. Suppose that a fourth portfolio D exists with expected return 1.10 and factor loadings B1D = 2 and 32D = 0. Does an arbitrage opportunity exist? Explain

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock