Question: Problem 2 Given the following data, price the Credit Default Swap on the following bond. Assume that default may occur at year-end, that is, at

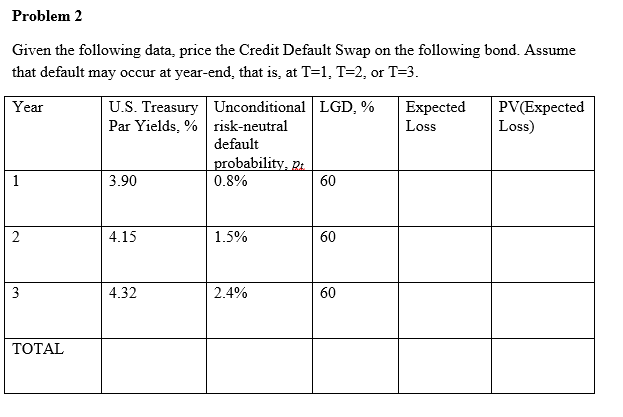

Problem 2 Given the following data, price the Credit Default Swap on the following bond. Assume that default may occur at year-end, that is, at T-, T 2, or T-3 Year U.S. Treasury | Unconditional | LGD, % Par Yields, % | risk-neutral | Expected | PV(Expected Loss Loss) default probability,2 0.8% 3.90 60 4.15 1.5% 60 4.32 2.4% 60 TOTAL

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock