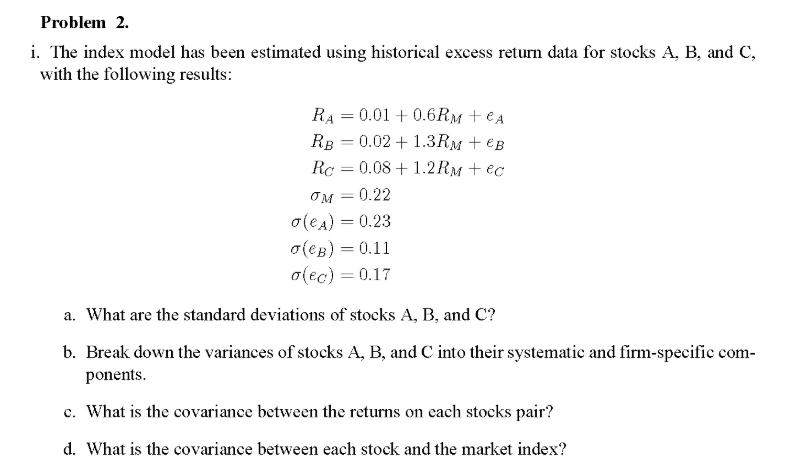

Question: Problem 2. i. The index model has been estimated using historical excess return data for stocks A, B, and C, with the following results: RA

Problem 2. i. The index model has been estimated using historical excess return data for stocks A, B, and C, with the following results: RA = 0.01 + 0.6 RM + A RB = 0.02 + 1.3Rm +eB Rc = 0.08 + 1.2 RM + ec OM= 0.22 olea) = 0.23 (b) = 0.11 (ec) = 0.17 a. What are the standard deviations of stocks A, B, and C? b. Break down the variances of stocks A, B, and C into their systematic and firm-specific com- ponents. c. What is the covariance between the returns on each stocks pair? d. What is the covariance between each stock and the market index? Problem 2. i. The index model has been estimated using historical excess return data for stocks A, B, and C, with the following results: RA = 0.01 + 0.6 RM + A RB = 0.02 + 1.3Rm +eB Rc = 0.08 + 1.2 RM + ec OM= 0.22 olea) = 0.23 (b) = 0.11 (ec) = 0.17 a. What are the standard deviations of stocks A, B, and C? b. Break down the variances of stocks A, B, and C into their systematic and firm-specific com- ponents. c. What is the covariance between the returns on each stocks pair? d. What is the covariance between each stock and the market index

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts