Question: Problem 2 The analyst uses the historical returns to estimate the expected return for the US Large Cap fund as follows: r i - r

Problem

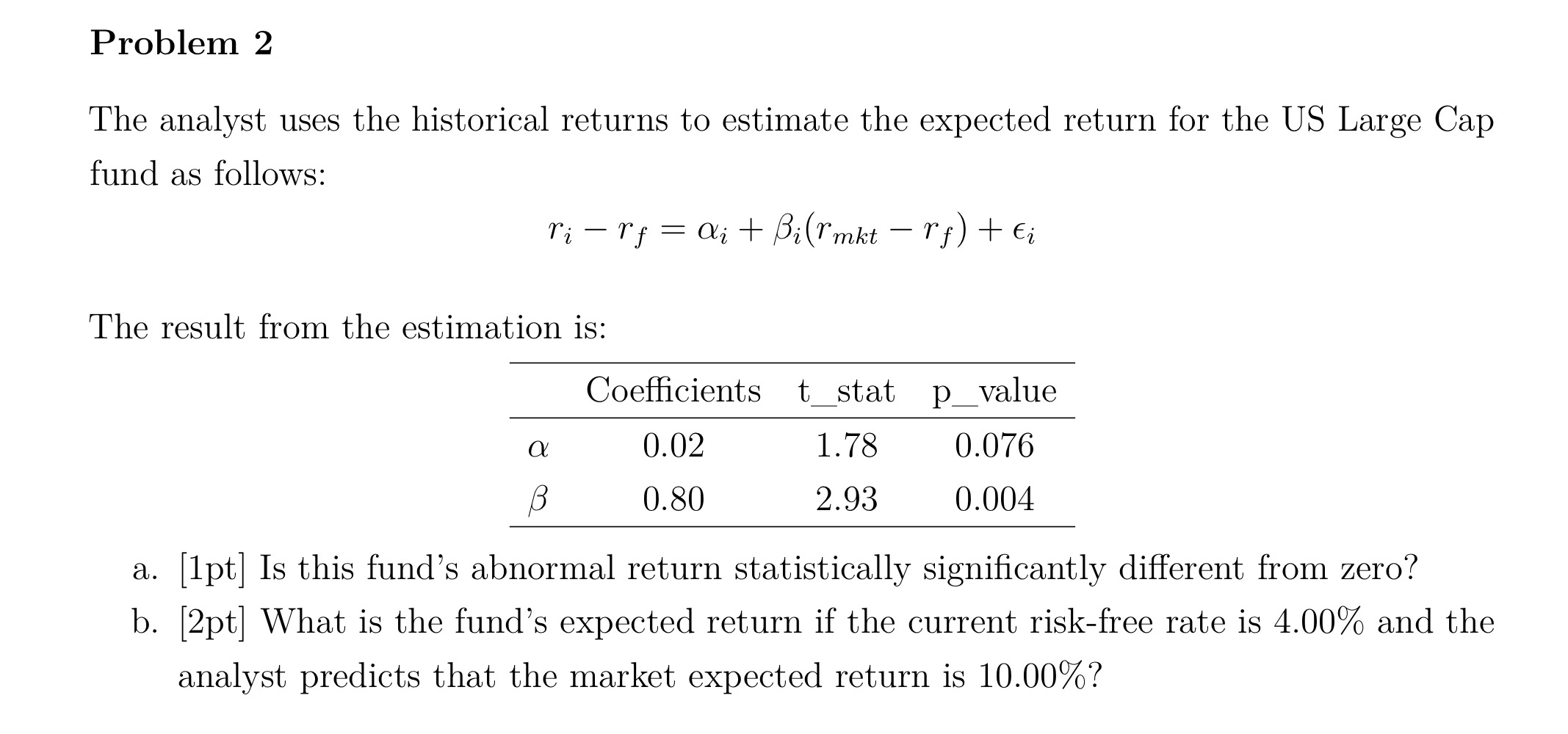

The analyst uses the historical returns to estimate the expected return for the US Large Cap fund as follows:

The result from the estimation is:

tableCoefficients,tstat,pvalue

a Is this fund's abnormal return statistically significantly different from zero?

bpt What is the fund's expected return if the current riskfree rate is and the analyst predicts that the market expected return is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock