Question: Problem 2 We consider an agent and two assets, A and B, and two states of the world, s1 and s2. Asset A is a

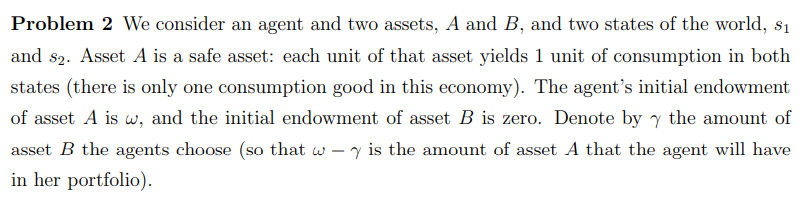

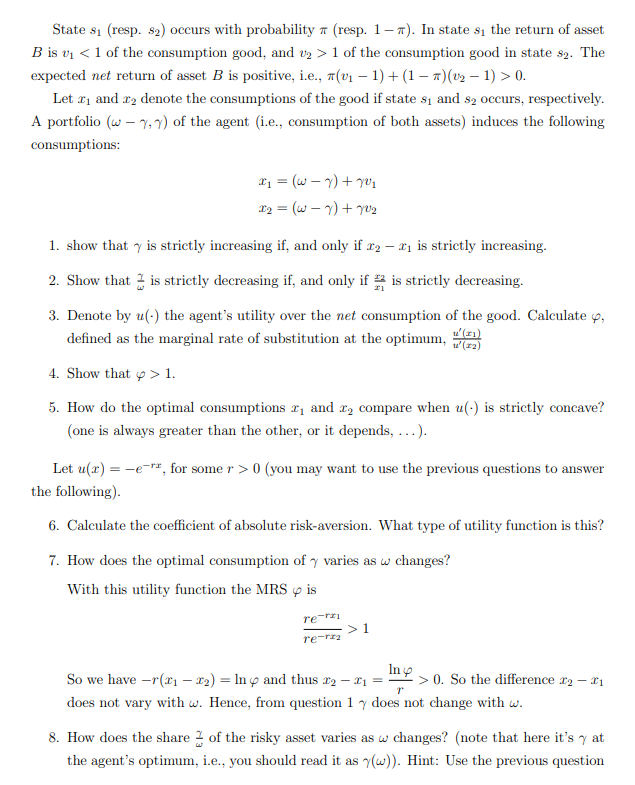

Problem 2 We consider an agent and two assets, A and B, and two states of the world, s1 and s2. Asset A is a safe asset: each unit of that asset yields 1 unit of consumption in both states (there is only one consumption good in this economy). The agent's initial endowment of asset A is , and the initial endowment of asset B is zero. Denote by the amount of asset B the agents choose (so that is the amount of asset A that the agent will have in her portfolio). State s1 (resp. s2 ) occurs with probability (resp. 1 ). In state s1 the return of asset B is v11 of the consumption good in state s2. The expected net return of asset B is positive, i.e., (v11)+(1)(v21)>0. Let x1 and x2 denote the consumptions of the good if state s1 and s2 occurs, respectively. A portfolio (,) of the agent (i.e., consumption of both assets) induces the following consumptions: x1=()+v1x2=()+v2 1. show that is strictly increasing if, and only if x2x1 is strictly increasing. 2. Show that is strictly decreasing if, and only if x1x2 is strictly decreasing. 3. Denote by u() the agent's utility over the net consumption of the good. Calculate , defined as the marginal rate of substitution at the optimum, u(x2)u(x1) 4. Show that >1. 5. How do the optimal consumptions x1 and x2 compare when u() is strictly concave? (one is always greater than the other, or it depends, ...). Let u(x)=erx, for some r>0 (you may want to use the previous questions to answer the following). 6. Calculate the coefficient of absolute risk-aversion. What type of utility function is this? 7. How does the optimal consumption of varies as changes? With this utility function the MRS is rerx2rerx1>1 So we have r(x1x2)=ln and thus x2x1=rln>0. So the difference x2x1 does not vary with . Hence, from question 1 does not change with . 8. How does the share of the risky asset varies as changes? (note that here it's at the agent's optimum, i.e., you should read it as () ). Hint: Use the previous question Problem 2 We consider an agent and two assets, A and B, and two states of the world, s1 and s2. Asset A is a safe asset: each unit of that asset yields 1 unit of consumption in both states (there is only one consumption good in this economy). The agent's initial endowment of asset A is , and the initial endowment of asset B is zero. Denote by the amount of asset B the agents choose (so that is the amount of asset A that the agent will have in her portfolio). State s1 (resp. s2 ) occurs with probability (resp. 1 ). In state s1 the return of asset B is v11 of the consumption good in state s2. The expected net return of asset B is positive, i.e., (v11)+(1)(v21)>0. Let x1 and x2 denote the consumptions of the good if state s1 and s2 occurs, respectively. A portfolio (,) of the agent (i.e., consumption of both assets) induces the following consumptions: x1=()+v1x2=()+v2 1. show that is strictly increasing if, and only if x2x1 is strictly increasing. 2. Show that is strictly decreasing if, and only if x1x2 is strictly decreasing. 3. Denote by u() the agent's utility over the net consumption of the good. Calculate , defined as the marginal rate of substitution at the optimum, u(x2)u(x1) 4. Show that >1. 5. How do the optimal consumptions x1 and x2 compare when u() is strictly concave? (one is always greater than the other, or it depends, ...). Let u(x)=erx, for some r>0 (you may want to use the previous questions to answer the following). 6. Calculate the coefficient of absolute risk-aversion. What type of utility function is this? 7. How does the optimal consumption of varies as changes? With this utility function the MRS is rerx2rerx1>1 So we have r(x1x2)=ln and thus x2x1=rln>0. So the difference x2x1 does not vary with . Hence, from question 1 does not change with . 8. How does the share of the risky asset varies as changes? (note that here it's at the agent's optimum, i.e., you should read it as () ). Hint: Use the previous

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts