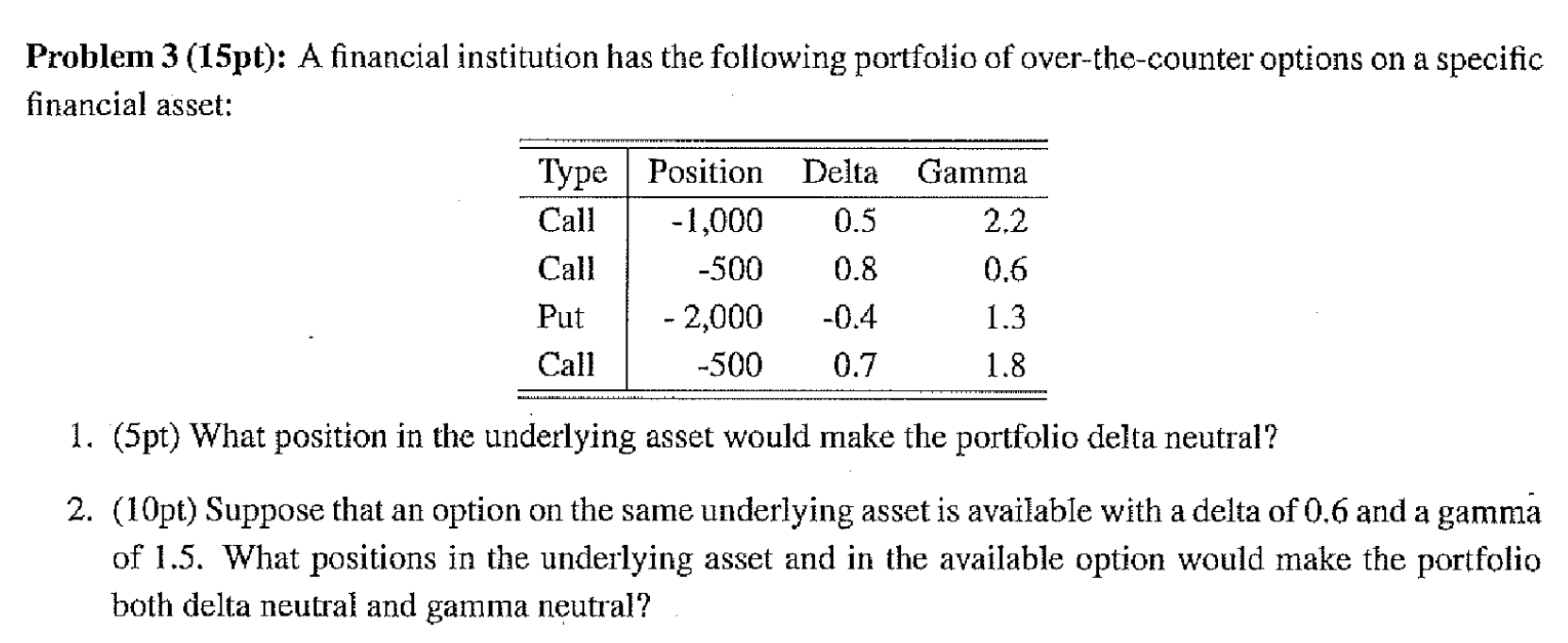

Question: Problem 3 ( 1 5 pt ) : A financial institution has the following portfolio of over - the - counter options on a specific

Problem pt: A financial institution has the following portfolio of overthecounter options on a specific

financial asset:

pt What position in the underlying asset would make the portfolio delta neutral?

pt Suppose that an option on the same underlying asset is available with a delta of and a gamma

of What positions in the underlying asset and in the available option would make the portfolio

both delta neutral and gamma neutral?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock