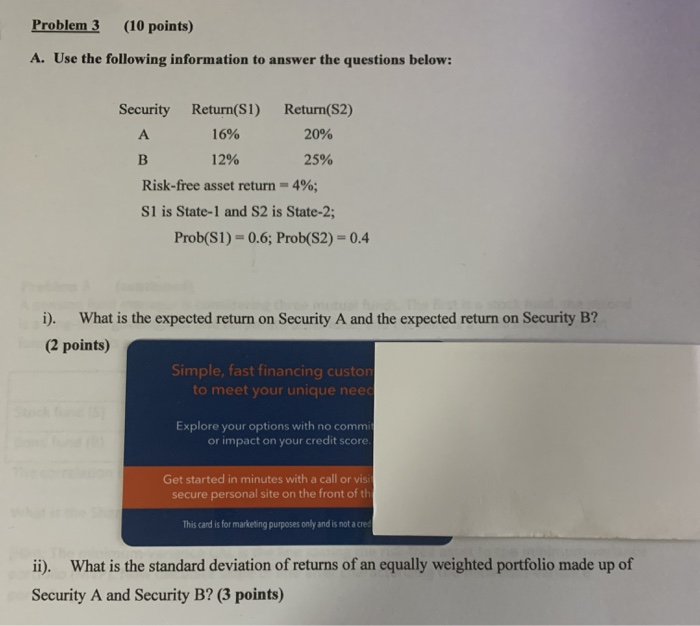

Question: Problem 3 (10 points) A. Use the following information to answer the questions below: Security Return(S1) Return(S2) A 16% 20% B 12% 25% Risk-free asset

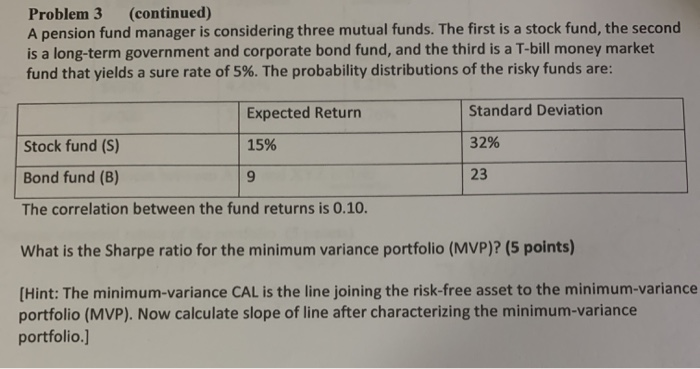

Problem 3 (10 points) A. Use the following information to answer the questions below: Security Return(S1) Return(S2) A 16% 20% B 12% 25% Risk-free asset return -4%; Si is State-1 and S2 is State-2; Prob(S1) = 0.6; Prob(S2) = 0.4 i). What is the expected return on Security A and the expected return on Security B? (2 points) Simple, fast financing custon to meet your unique need Explore your options with no commit or impact on your credit score. Get started in minutes with a call or visi secure personal site on the front of thi This card is for marketing purposes only and is not a cred ii). What is the standard deviation of returns of an equally weighted portfolio made up of Security A and Security B? (3 points) Problem 3 (continued) A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5%. The probability distributions of the risky funds are: Expected Return Standard Deviation 32% Stock fund (5) 15% Bond fund (B) 9 The correlation between the fund returns is 0.10. 23 What is the Sharpe ratio for the minimum variance portfolio (MVP)? (5 points) [Hint: The minimum-variance CAL is the line joining the risk-free asset to the minimum-variance portfolio (MVP). Now calculate slope of line after characterizing the minimum-variance portfolio.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts