Question: Problem 3 (20 points). A CPA has been engaged to audit the financial statements ofCousy Distributors, Inc., a continuing audit client, for the year ended

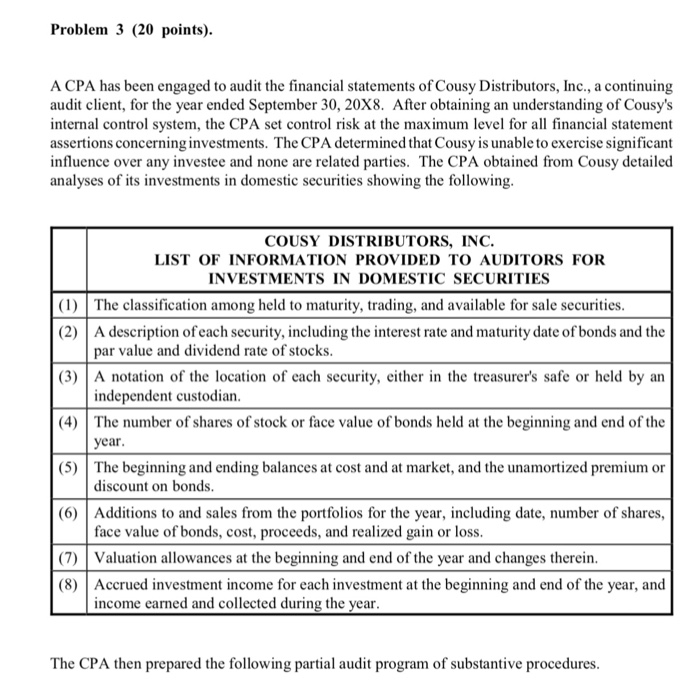

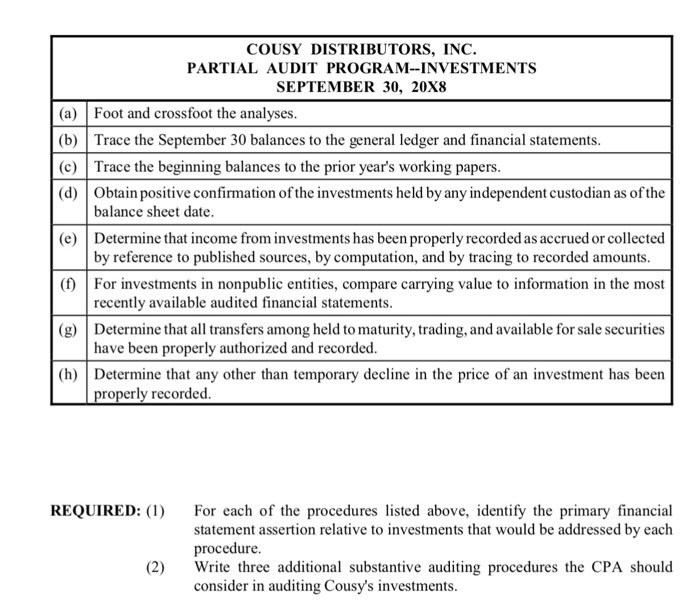

Problem 3 (20 points). A CPA has been engaged to audit the financial statements ofCousy Distributors, Inc., a continuing audit client, for the year ended September 30,20X8. After obtaining an understanding of Cousy's internal control system, the CPA set control risk at the maximum level for all financial statement assertions concerning investments. The CPA determined that Cousy is unable to exercise significant influence over any investee and none are related parties. The CPA obtained from Cousy detailed analyses of its investments in domestic securities showing the following COUSY DISTRIBUTORS, INC LIST OF INFORMATION PROVIDED TO AUDITORS FOR NVESTMENTS IN DOMESTIC SECURITIES (1) The classification among held to maturity, trading, and available for sale securities (2) A description of each security, including the interest rate and maturity date of bonds and the (3) A notation of the location of each security, either in the treasurer's safe or held by arn (4) The number of shares of stock or face value of bonds held at the beginning and end of the (5) The beginning and ending balances at cost and at market, and the unamortized premium or (6) Additions to and sales from the portfolios for the year, including date, number of shares, (7 Valuation allowances at the beginning and end of the year and changes therein. (8) Accrued investment income for each investment at the beginning and end of the year, and par value and dividend rate of stocks independent custodian year discount on bonds. face value of bonds, cost, proceeds, and realized gain or loss income earned and collected during the year The CPA then prepared the following partial audit program of substantive procedures COUSY DISTRIBUTORS, INC. PARTIAL AUDIT PROGRAM-INVESTMENTS SEPTEMBER 30, 20X8 (a) Foot and crossfoot the analyses (b) Trace the September 30 balances to the general ledger and financial statements. (c) Trace the beginning balances to the prior year's working papers. (d Obtain positive confirmation of the investments held by any independent custodian as of the balance sheet date. (e) Determine that income from investments has been properly recorded as accrued or collected (f For investments in nonpublic entities, compare carrying value to information in the most (g)Determine that al transfers among held to maturity, trading, and available for sale securities (h) Determine that any other than temporary decline in the price of an investment has been by reference to published sources, by computation, and by tracing to recorded amounts. recently available audited financial statements. have been properly authorized and recorded. properly recorded REQUIRED: (1) For each of the procedures listed above, identify the primary financial statement assertion relative to investments that would be addressed by each procedure (2 Write three additional substantive auditing procedures the CPA should consider in auditing Cousy's investments

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts