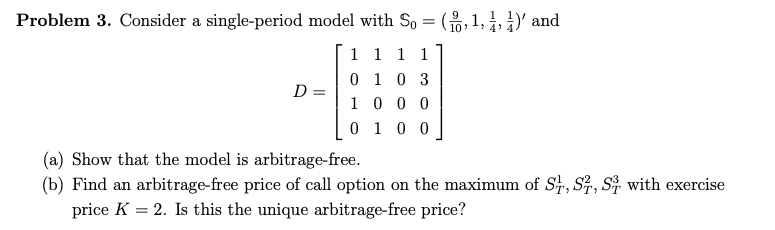

Question: Problem 3. Consider a single-period model with So = (0,1, , )' and 1 1 1 1 D= 0 1 0 3 1 0 0

Problem 3. Consider a single-period model with So = (0,1, , )' and 1 1 1 1 D= 0 1 0 3 1 0 0 0 0 1 0 0 (a) Show that the model is arbitrage-free. (b) Find an arbitrage-free price of call option on the maximum of S1, S2, S with exercise price K = 2. Is this the unique arbitrage-free price? Problem 3. Consider a single-period model with So = (0,1, , )' and 1 1 1 1 D= 0 1 0 3 1 0 0 0 0 1 0 0 (a) Show that the model is arbitrage-free. (b) Find an arbitrage-free price of call option on the maximum of S1, S2, S with exercise price K = 2. Is this the unique arbitrage-free price

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock