Question: Problem 3 Estimating volatility and Value-at- Risk 3(a) Estimating volatility 2 points Suppose at time t = 0 we have an annual log return volatility

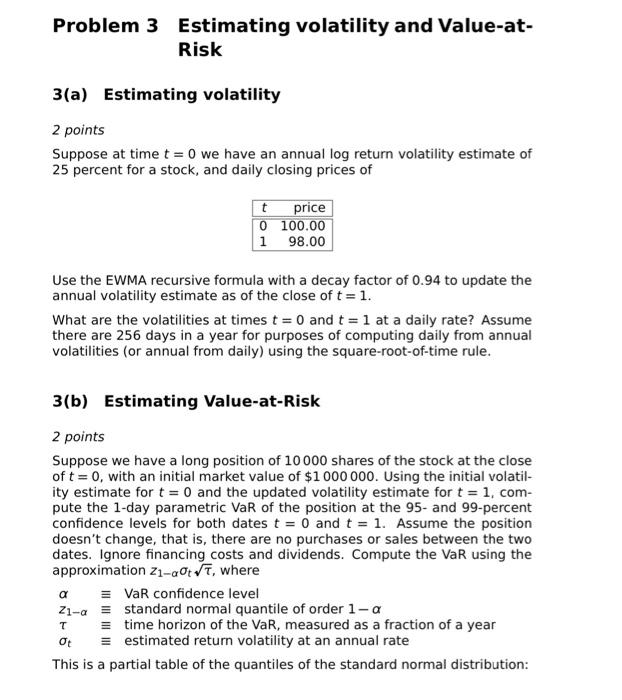

Problem 3 Estimating volatility and Value-at- Risk 3(a) Estimating volatility 2 points Suppose at time t = 0 we have an annual log return volatility estimate of 25 percent for a stock, and daily closing prices of t price 0 100.00 1 98.00 Use the EWMA recursive formula with a decay factor of 0.94 to update the annual volatility estimate as of the close of t = 1. What are the volatilities at times t = 0 and t = 1 at a daily rate? Assume there are 256 days in a year for purposes of computing daily from annual volatilities (or annual from daily) using the square-root-of-time rule. 3(b) Estimating Value-at-Risk 2 points Suppose we have a long position of 10 000 shares of the stock at the close of t = 0, with an initial market value of $ 1 000 000. Using the initial volatil- ity estimate for t = 0 and the updated volatility estimate for t = 1, com- pute the 1-day parametric VaR of the position at the 95- and 99-percent confidence levels for both dates t = 0 and t = 1. Assume the position doesn't change, that is, there are no purchases or sales between the two dates. Ignore financing costs and dividends. Compute the VaR using the approximation 21-01VT, where = VaR confidence level 21-a = standard normal quantile of order 1-a = time horizon of the VaR, measured as a fraction of a year = estimated return volatility at an annual rate This is a partial table of the quantiles of the standard normal distribution: a Ot

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts