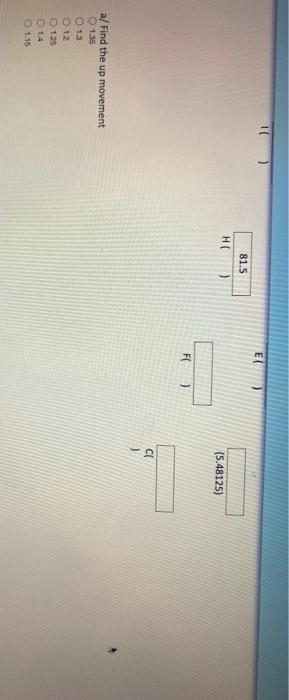

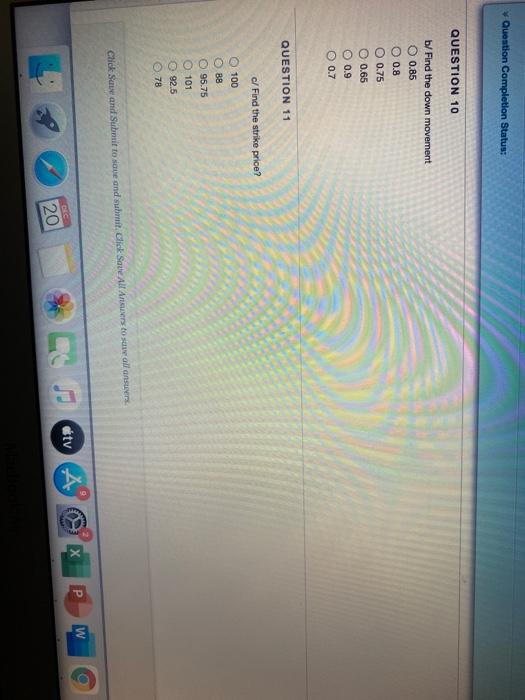

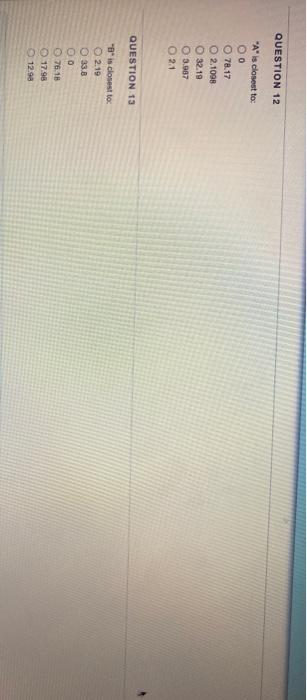

Question: Problem 3/ Given the following information, answer the below questions based on the following incomplete 3-period American put option binomial tree: The risk free rate

Problem 3/ Given the following information, answer the below questions based on the following incomplete 3-period American put option binomial tree: The risk free rate is 2% Time to expiration equals 9 months . The risk neutral probability of the up movement is "p" = 0.45 . The risk neutral probability of the down movement is "q" Up = (2down) - 0.15 2*10.5+q) - up + down . AI ) DY G C > B 10 ) El ) R15 Sund Submitove and it Click Salle El 81.5 HO) (5.48125) FC ) CE ) a/ Find the up movement @ 1.35 13 12 1:25 1.4 1.15 Question Completion Status: QUESTION 10 b/Find the down movement 0.85 O 0.8 O 0.75 0 0.65 O 0.9 0 0.7 QUESTION 11 c/ Find the strike price? 100 BB 95.75 101 92.5 0.78 Click Save and Submit to save and submit. Click Save All Answers to sew all answers W etv 20 QUESTION 12 "A" is closest to: O 78.17 2.1098 32.19 3.987 21 QUESTION 13 "B" is closest to 2.19 33.8 00 76.18 17.98 12.98

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts