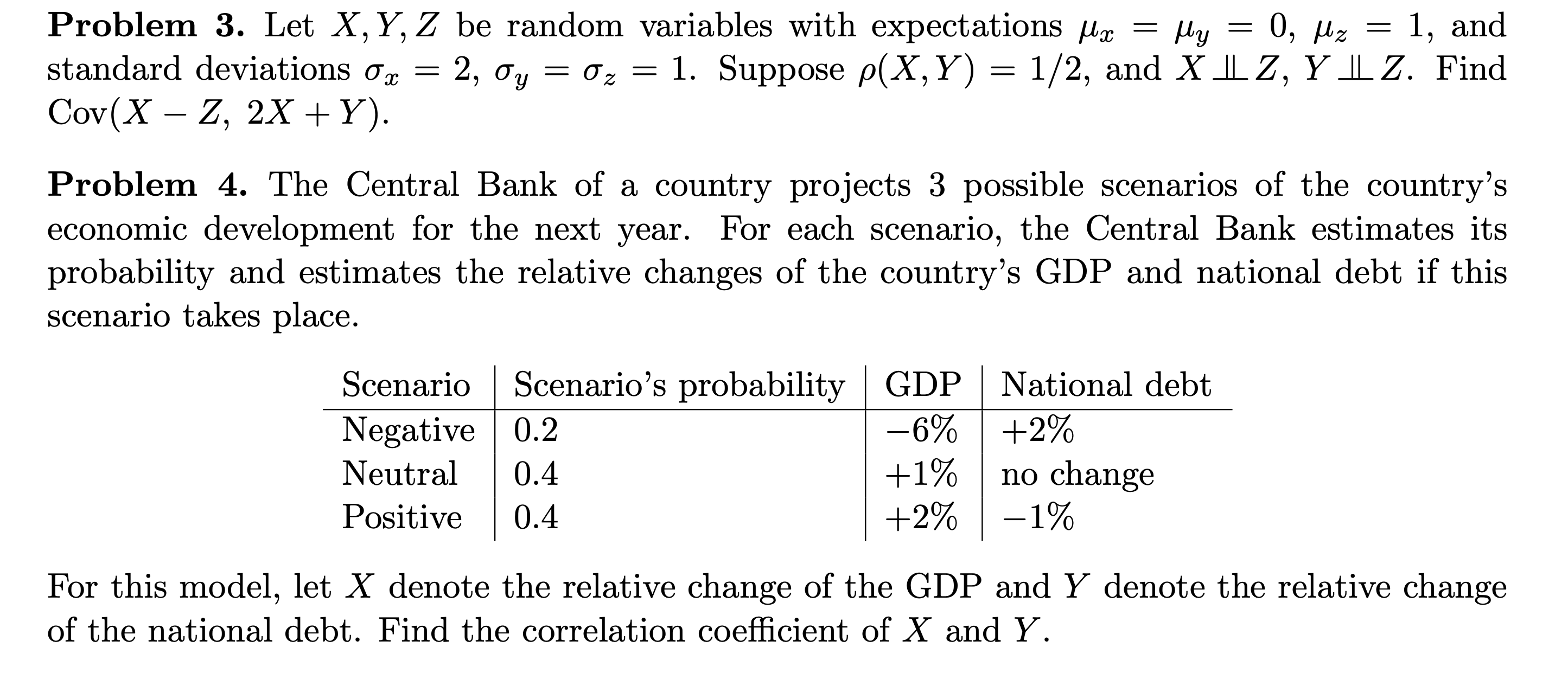

Question: Problem 3. Let X,Y,Z be random variables With expectations pm = My 2 0, ,uz = 1, and standard deviations am 2 2, 0y 2

Problem 3. Let X,Y,Z be random variables With expectations pm = My 2 0, ,uz = 1, and standard deviations am 2 2, 0y 2 02 = 1. Suppose p(X, Y) = 1/2, and XJLZ, YJLZ. Find Cov(X Z, 2X + Y). Problem 4. The Central Bank of a country projects 3 possible scenarios of the country's economic development for the next year. For each scenario, the Central Bank estimates its probability and estimates the relative changes of the country's GDP and national debt if this scenario takes place. Scenario GDP National debt Scenario's probability Negative +2% Neutral no change Positive 1% For this model, let X denote the relative change of the GDP and Y denote the relative change of the national debt. Find the correlation coefcient of X and Y

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts