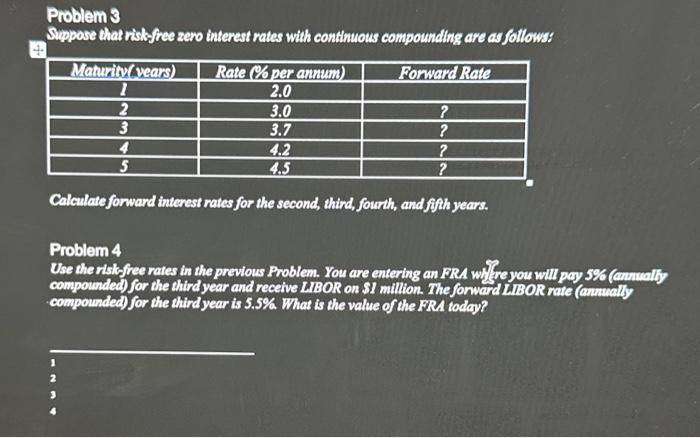

Question: Problem 3 Suppose that rish-free zero interest rates with continuous compounding are as follows: Calculate forward interest rates for the second, thind, fourth, and fifh

Problem 3 Suppose that rish-free zero interest rates with continuous compounding are as follows: Calculate forward interest rates for the second, thind, fourth, and fifh years. Problem 4 Use the risks free rates in the prewtous Problem. You are entering an FRA wil'se you will pay 5% (anmually, compounded) for the third year and receive LIBOR on SI million. The forward WBOR rate (anually compounded) for the third year is 5.5%. What is the value of the FRA today

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock