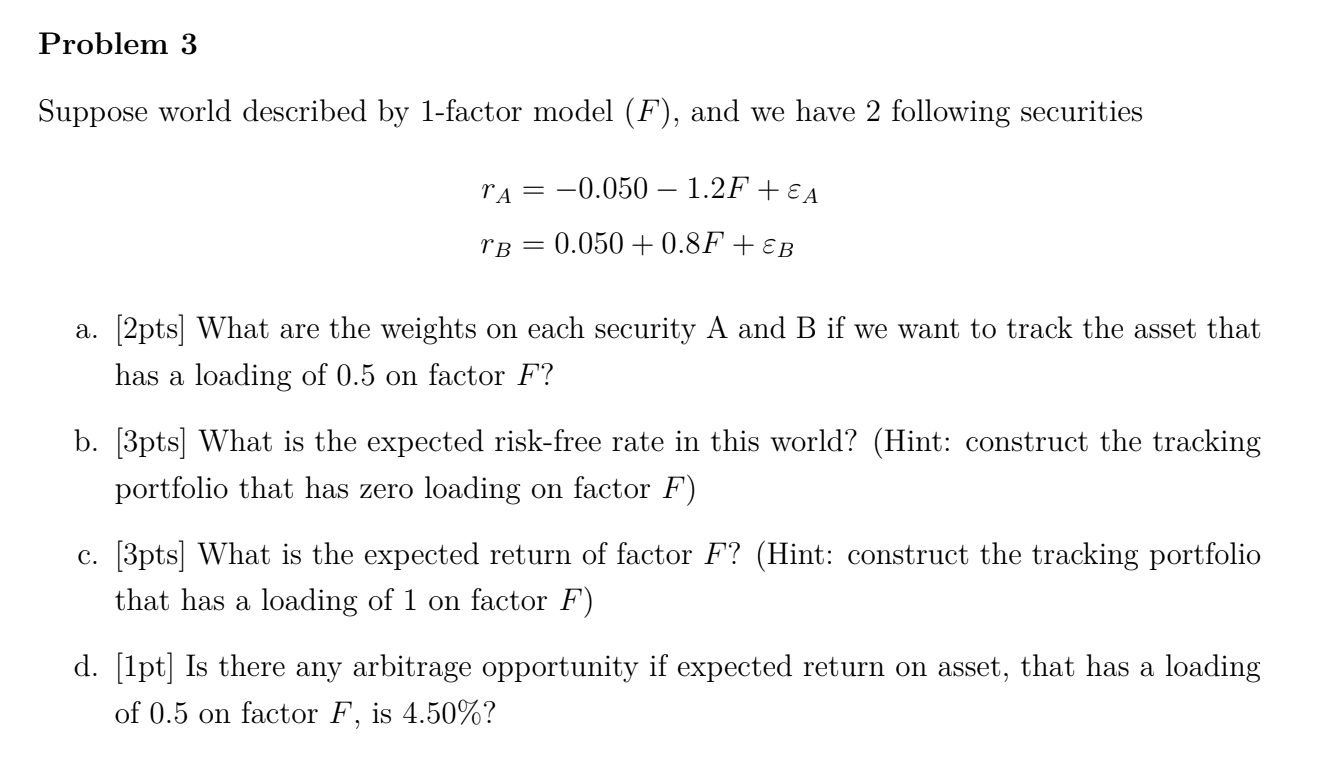

Question: Problem 3 Suppose world described by 1-factor model (F), and we have 2 following securities ra = -0.050 1.2F +EA rb = 0.050 + 0.8F

Problem 3 Suppose world described by 1-factor model (F), and we have 2 following securities ra = -0.050 1.2F +EA rb = 0.050 + 0.8F +B a. [2pts] What are the weights on each security A and B if we want to track the asset that has a loading of 0.5 on factor F? b. [3pts) What is the expected risk-free rate in this world? (Hint: construct the tracking portfolio that has zero loading on factor F) C. [3pts. What is the expected return of factor F? (Hint: construct the tracking portfolio that has a loading of 1 on factor F) d. [1pt] Is there any arbitrage opportunity if expected return on asset, that has a loading of 0.5 on factor F, is 4.50%? Problem 3 Suppose world described by 1-factor model (F), and we have 2 following securities ra = -0.050 1.2F +EA rb = 0.050 + 0.8F +B a. [2pts] What are the weights on each security A and B if we want to track the asset that has a loading of 0.5 on factor F? b. [3pts) What is the expected risk-free rate in this world? (Hint: construct the tracking portfolio that has zero loading on factor F) C. [3pts. What is the expected return of factor F? (Hint: construct the tracking portfolio that has a loading of 1 on factor F) d. [1pt] Is there any arbitrage opportunity if expected return on asset, that has a loading of 0.5 on factor F, is 4.50%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts