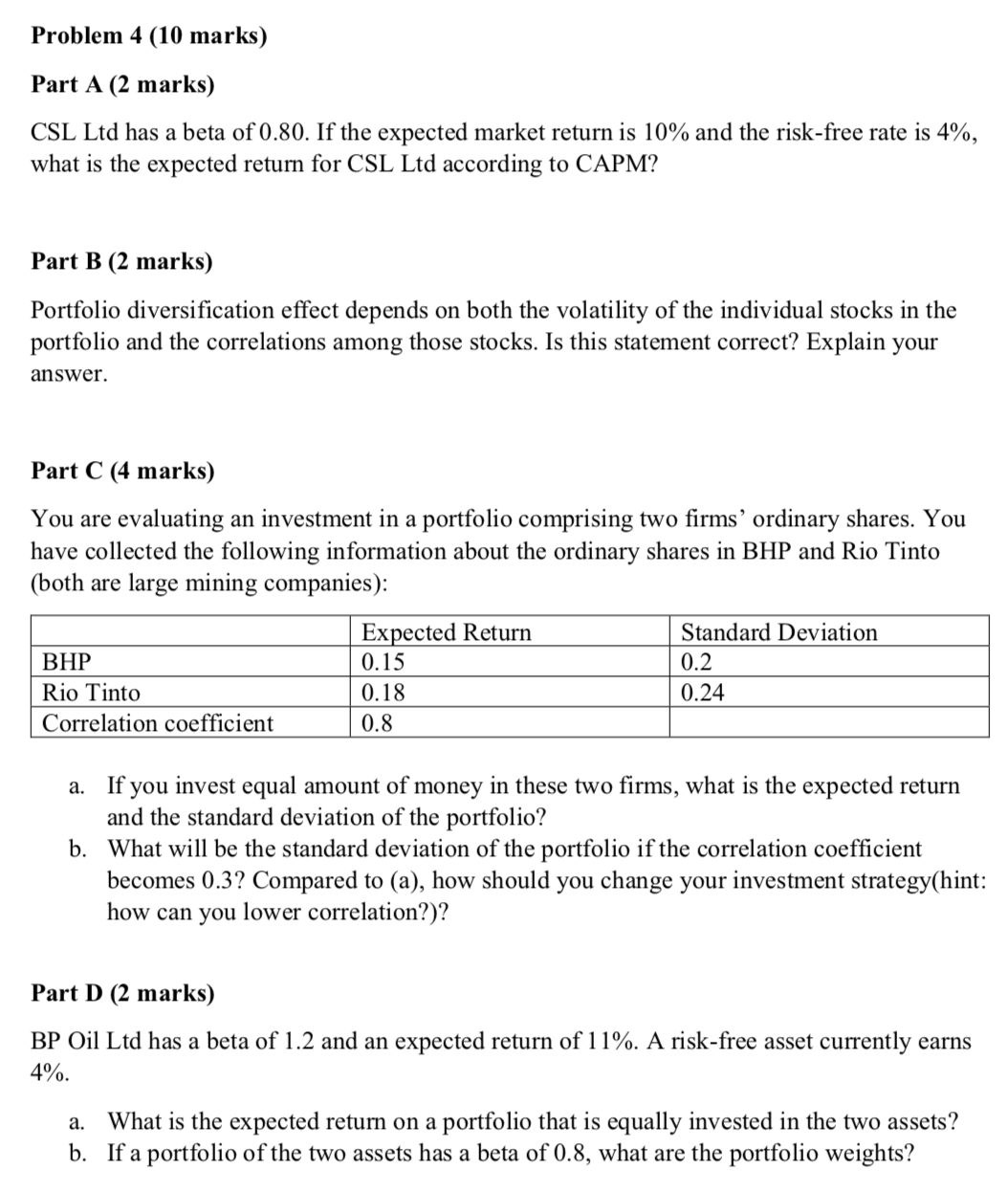

Question: Problem 4 (10 marks) Part A (2 marks) CSL Ltd has a beta of 0.80. If the expected market return is 10% and the risk-free

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts