Question: Problem 4. (10 pts) Consider the market model with 3 stocks given below: Stock Returns R1 R2 R3 Expected Return 0.80 0.60 1.10 Ri 0.20

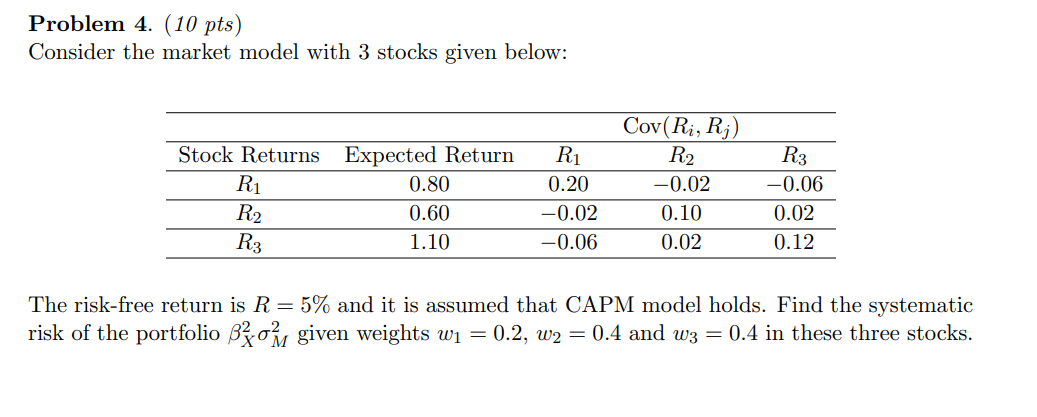

Problem 4. (10 pts) Consider the market model with 3 stocks given below: Stock Returns R1 R2 R3 Expected Return 0.80 0.60 1.10 Ri 0.20 -0.02 -0.06 Cov(Ri, Rj) R2 -0.02 0.10 0.02 R3 -0.06 0.02 0.12 The risk-free return is R = 5% and it is assumed that CAPM model holds. Find the systematic risk of the portfolio Bom given weights wi = 0.2, W2 = 0.4 and w3 = 0.4 in these three stocks. Problem 4. (10 pts) Consider the market model with 3 stocks given below: Stock Returns R1 R2 R3 Expected Return 0.80 0.60 1.10 Ri 0.20 -0.02 -0.06 Cov(Ri, Rj) R2 -0.02 0.10 0.02 R3 -0.06 0.02 0.12 The risk-free return is R = 5% and it is assumed that CAPM model holds. Find the systematic risk of the portfolio Bom given weights wi = 0.2, W2 = 0.4 and w3 = 0.4 in these three stocks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts