Question: Problem 4 Part A.3 (Exercise CFA n.10.a the book) Assume that both X and Y are well-diversfied port- folios and the risk-free rate is 8%

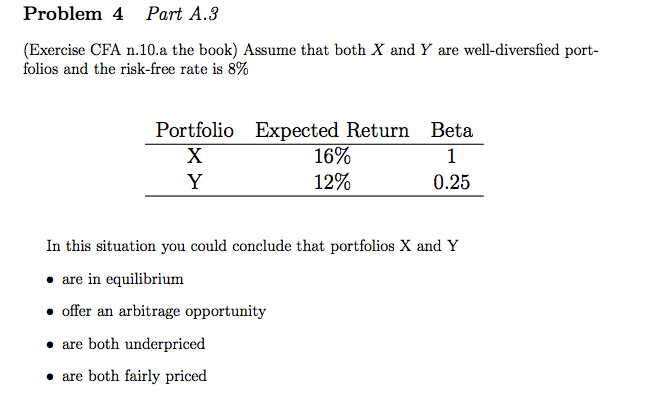

Problem 4 Part A.3 (Exercise CFA n.10.a the book) Assume that both X and Y are well-diversfied port- folios and the risk-free rate is 8% Portfolio Expected Return Beta 16% 12% 0.25 In this situation you could conclude that portfolios X and Y are in equilibrium offer an arbitrage opportunity are both underpriced are both fairly priced

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock