Question: Problem 4B-6 Step-Down Method versus Direct Method; Predetermined Overhead Rates [LO4-10, LO4-11) The Sendai Co., Ltd., of Japan has budgeted costs in its various departments

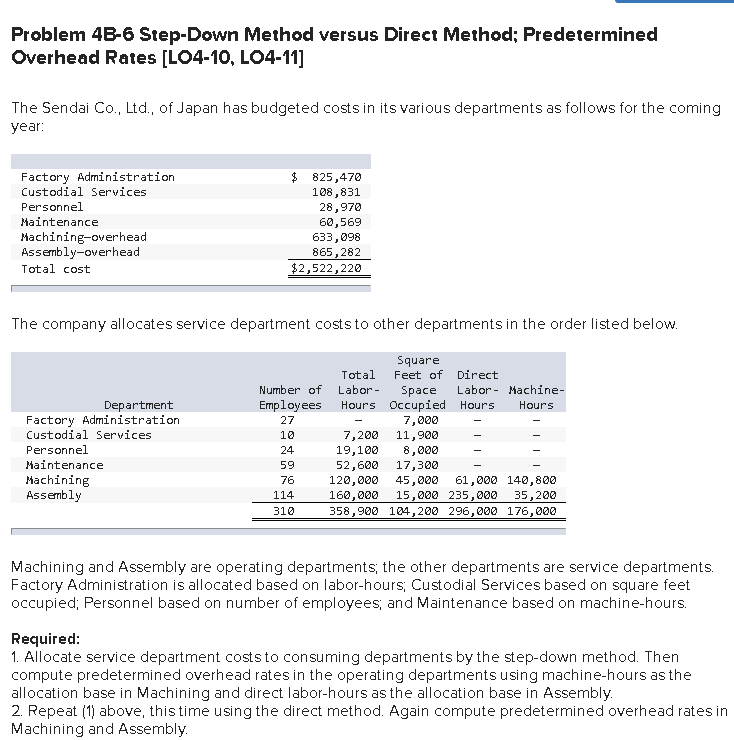

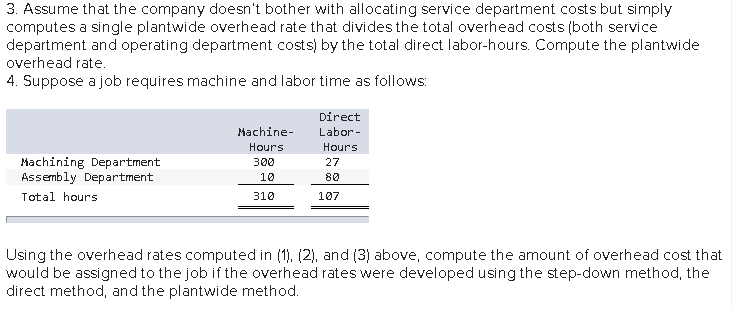

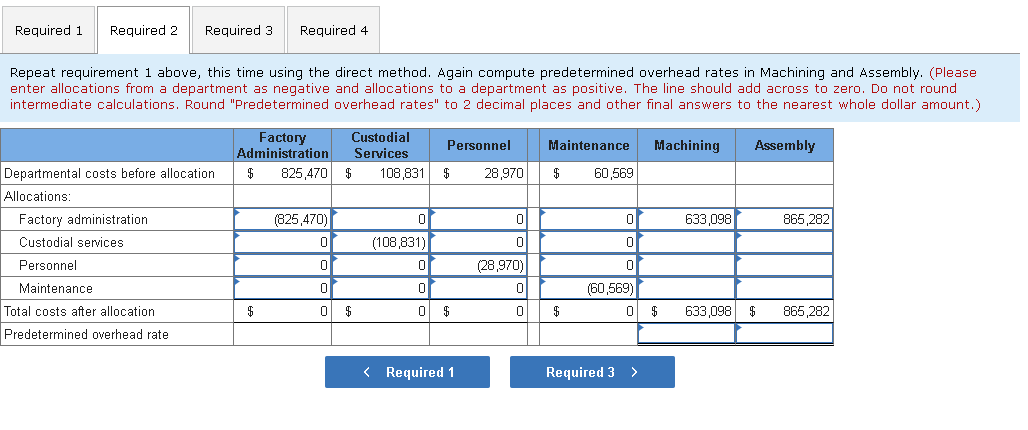

Problem 4B-6 Step-Down Method versus Direct Method; Predetermined Overhead Rates [LO4-10, LO4-11) The Sendai Co., Ltd., of Japan has budgeted costs in its various departments as follows for the coming year: Factory Administration Custodial Services Personnel Maintenance Machining-overhead Assembly-overhead Total cost $ 825,470 108,831 28,970 60,569 633,098 865,282 $2,522,220 The company allocates service department costs to other departments in the order listed below. 27 Department Factory Administration Custodial Services Personnel Maintenance Machining Assembly Square Total Feet of Direct Number of Labor Space Labor- Machine- Employees Hours Occupied Hours Hours - 7,000 10 7,200 11,900 24 19,100 8,000 - 52,600 17,300 76 120,000 45,000 61,000 140,800 114 160,000 15,000 235,000 35,200 310 358,900 104,200 296,000 176,000 59 Machining and Assembly are operating departments, the other departments are service departments. Factory Administration is allocated based on labor-hours Custodial Services based on square feet occupied; Personnel based on number of employees and Maintenance based on machine-hours. Required: 1. Allocate service department costs to consuming departments by the step-down method. Then compute predetermined overhead rates in the operating departments using machine-hours as the allocation base in Machining and direct labor-hours as the allocation base in Assembly. 2. Repeat (1) above, this time using the direct method. Again compute predetermined overhead rates in Machining and Assembly. 3. Assume that the company doesn't bother with allocating service department costs but simply computes a single plantwide overhead rate that divides the total overhead costs (both service department and operating department costs) by the total direct labor-hours. Compute the plantwide overhead rate. 4. Suppose a job requires machine and labor time as follows: Direct Labor - Hours 27 80 Machine- Hours 300 10 310 Machining Department Assembly Department Total hours 107 Using the overhead rates computed in (1). (2), and (3) above, compute the amount of overhead cost that would be assigned to the job if the overhead rates were developed using the step-down method, the direct method, and the plantwide method. Required 1 Required 2 Required 3 Required 4 Repeat requirement 1 above, this time using the direct method. Again compute predetermined overhead rates in Machining and Assembly. (Please enter allocations from a department as negative and allocations to a department as positive. The line should add across to zero. Do not round intermediate calculations. Round "Predetermined overhead rates" to 2 decimal places and other final answers to the nearest whole dollar amount.) Machining Assembly Factory Administration | $ 825,470 Custodial Services $ 108,831 Personnel Maintenance $ 28,970|| $ 60,569 633,098 865,282 Departmental costs before allocation Allocations: Factory administration Custodial services Personnel Maintenance Total costs after allocation Predetermined overhead rate (825,470)| 0 0 0 0 (108,831)| 0 0 0 0 (28,970) 0 0 0 0 (60,569) 0 $ 633,098 $ 865,282 Problem 4B-6 Step-Down Method versus Direct Method; Predetermined Overhead Rates [LO4-10, LO4-11) The Sendai Co., Ltd., of Japan has budgeted costs in its various departments as follows for the coming year: Factory Administration Custodial Services Personnel Maintenance Machining-overhead Assembly-overhead Total cost $ 825,470 108,831 28,970 60,569 633,098 865,282 $2,522,220 The company allocates service department costs to other departments in the order listed below. 27 Department Factory Administration Custodial Services Personnel Maintenance Machining Assembly Square Total Feet of Direct Number of Labor Space Labor- Machine- Employees Hours Occupied Hours Hours - 7,000 10 7,200 11,900 24 19,100 8,000 - 52,600 17,300 76 120,000 45,000 61,000 140,800 114 160,000 15,000 235,000 35,200 310 358,900 104,200 296,000 176,000 59 Machining and Assembly are operating departments, the other departments are service departments. Factory Administration is allocated based on labor-hours Custodial Services based on square feet occupied; Personnel based on number of employees and Maintenance based on machine-hours. Required: 1. Allocate service department costs to consuming departments by the step-down method. Then compute predetermined overhead rates in the operating departments using machine-hours as the allocation base in Machining and direct labor-hours as the allocation base in Assembly. 2. Repeat (1) above, this time using the direct method. Again compute predetermined overhead rates in Machining and Assembly. 3. Assume that the company doesn't bother with allocating service department costs but simply computes a single plantwide overhead rate that divides the total overhead costs (both service department and operating department costs) by the total direct labor-hours. Compute the plantwide overhead rate. 4. Suppose a job requires machine and labor time as follows: Direct Labor - Hours 27 80 Machine- Hours 300 10 310 Machining Department Assembly Department Total hours 107 Using the overhead rates computed in (1). (2), and (3) above, compute the amount of overhead cost that would be assigned to the job if the overhead rates were developed using the step-down method, the direct method, and the plantwide method. Required 1 Required 2 Required 3 Required 4 Repeat requirement 1 above, this time using the direct method. Again compute predetermined overhead rates in Machining and Assembly. (Please enter allocations from a department as negative and allocations to a department as positive. The line should add across to zero. Do not round intermediate calculations. Round "Predetermined overhead rates" to 2 decimal places and other final answers to the nearest whole dollar amount.) Machining Assembly Factory Administration | $ 825,470 Custodial Services $ 108,831 Personnel Maintenance $ 28,970|| $ 60,569 633,098 865,282 Departmental costs before allocation Allocations: Factory administration Custodial services Personnel Maintenance Total costs after allocation Predetermined overhead rate (825,470)| 0 0 0 0 (108,831)| 0 0 0 0 (28,970) 0 0 0 0 (60,569) 0 $ 633,098 $ 865,282

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts