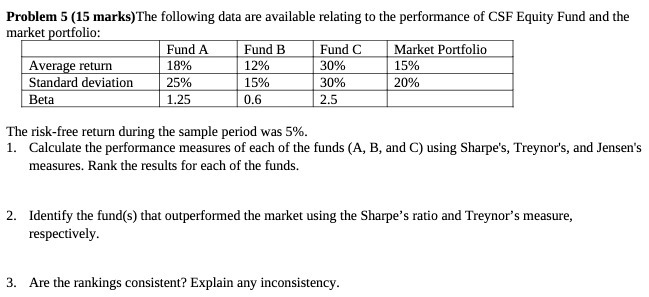

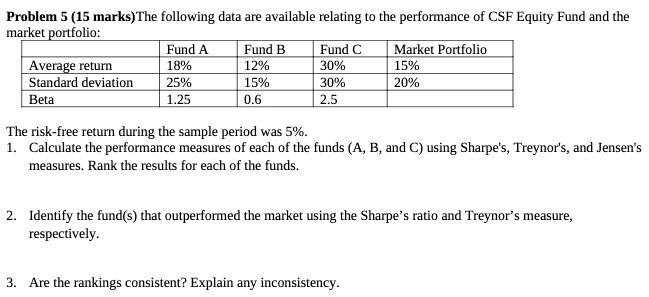

Question: Problem 5 (15 marks) The following data are available relating to the performance of CSF Equity Fund and the market portfolio: Fund A Fund B

Problem 5 (15 marks) The following data are available relating to the performance of CSF Equity Fund and the market portfolio: Fund A Fund B Fund C Market Portfolio Average return 18% 12% 30% 15% Standard deviation 25% 15% 30% 20% Beta 1.25 0.6 2.5 The risk-free return during the sample period was 5%. 1. Calculate the performance measures of each of the funds (A, B, and C) using Sharpe's, Treynor's, and Jensen's measures. Rank the results for each of the funds. 2. Identify the fund(s) that outperformed the market using the Sharpe's ratio and Treynor's measure, respectively. 3. Are the rankings consistent? Explain any inconsistency

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts