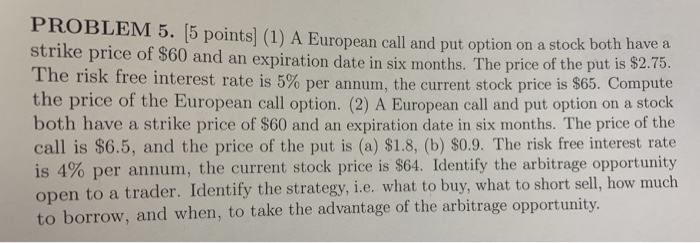

Question: PROBLEM 5 15 points| (1) A European call and put option on a stock both havea e price of $60 and an expiration date in

PROBLEM 5 15 points| (1) A European call and put option on a stock both havea e price of $60 and an expiration date in six months. The price of the put is $2.75. The risk free interest rate is 5% per annum, the current stock price is $65. Compute the price of the European call option. (2) A European call and put option on a stock both have a strike price of $60 and an expiration date in six months. The price of the call is $6.5, and the price of the put is (a) $1.8, (b) $0.9. The risk free interest rate is 4% per annum, the current stock price is $64. Identify the arbitrage opportunity open to a trader to borrow, and when, to take the advantage of the arbitrage opportunity. . Identify the strategy, i.e. what to buy, what to short sell, how much

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts