Question: Problem 5 An analyst wants to evaluate portfolio X, consisting entirely of U.S. common stocks, using both the Treynor and Sharpe measures of portfolio performance.

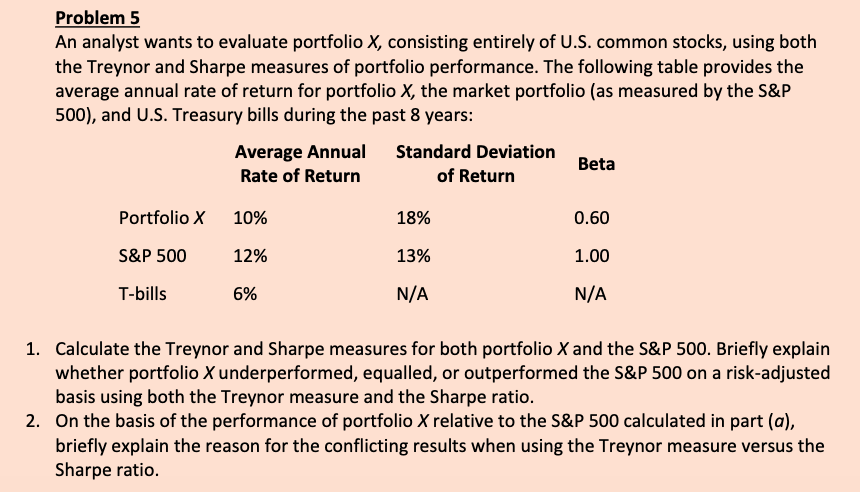

Problem 5 An analyst wants to evaluate portfolio X, consisting entirely of U.S. common stocks, using both the Treynor and Sharpe measures of portfolio performance. The following table provides the average annual rate of return for portfolio X, the market portfolio (as measured by the S&P 500), and U.S. Treasury bills during the past 8 years: Average Annual Standard Deviation Beta Rate of Return of Return Portfolio x 10% 18% 0.60 S&P 500 12% 13% 1.00 T-bills 6% N/A N/A 1. Calculate the Treynor and Sharpe measures for both portfolio X and the S&P 500. Briefly explain whether portfolio X underperformed, equalled, or outperformed the S&P 500 on a risk-adjusted basis using both the Treynor measure and the Sharpe ratio. 2. On the basis of the performance of portfolio X relative to the S&P 500 calculated in part (a), briefly explain the reason for the conflicting results when using the Treynor measure versus the Sharpe ratio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts