Question: Problem 5 Bookmark this page Problem 5 0 points possible (ungraded) Consider a 2-factor model. The risk free rate is ry=1%. There are two

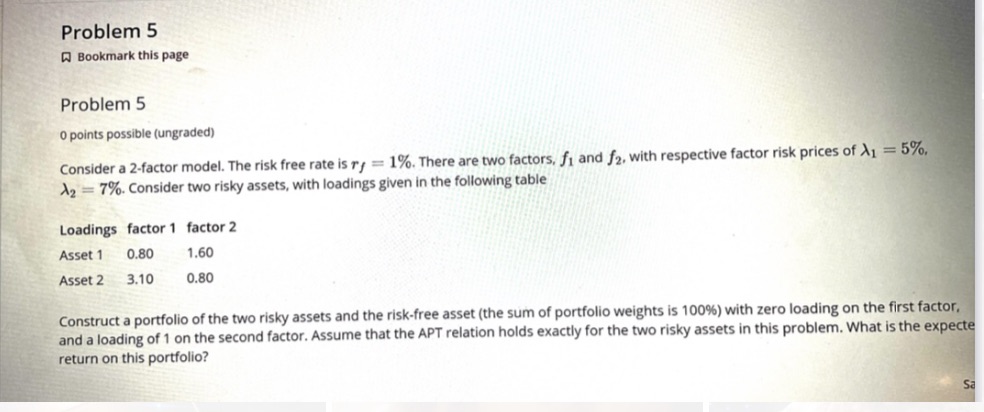

Problem 5 Bookmark this page Problem 5 0 points possible (ungraded) Consider a 2-factor model. The risk free rate is ry=1%. There are two factors, fi and f2, with respective factor risk prices of X1 = 5%, A2 7%. Consider two risky assets, with loadings given in the following table Loadings factor 1 factor 2 Asset 1 0.80 Asset 2 3.10 1.60 0.80 Construct a portfolio of the two risky assets and the risk-free asset (the sum of portfolio weights is 100 %) with zero loading on the first factor, and a loading of 1 on the second factor. Assume that the APT relation holds exactly for the two risky assets in this problem. What is the expecte return on this portfolio?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts