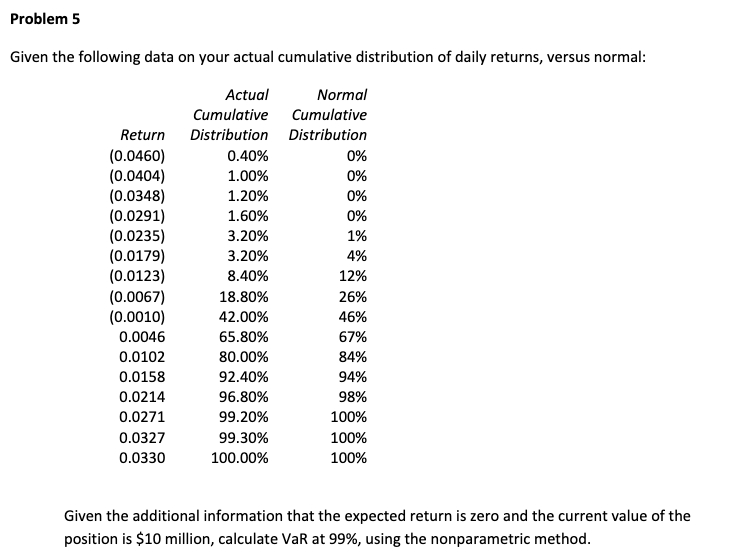

Question: Problem 5 Given the following data on your actual cumulative distribution of daily returns, versus normal: 0% Return (0.0460) (0.0404) (0.0348) (0.0291) (0.0235) (0.0179) (0.0123)

Problem 5 Given the following data on your actual cumulative distribution of daily returns, versus normal: 0% Return (0.0460) (0.0404) (0.0348) (0.0291) (0.0235) (0.0179) (0.0123) (0.0067) (0.0010) 0.0046 0.0102 0.0158 0.0214 0.0271 0.0327 0.0330 Actual Normal Cumulative Cumulative Distribution Distribution 0.40% 0% 1.00% 1.20% 0% 1.60% 0% 3.20% 1% 3.20% 4% 8.40% 12% 18.80% 26% 42.00% 46% 65.80% 67% 80.00% 84% 92.40% 94% 96.80% 98% 99.20% 100% 99.30% 100% 100.00% 100% Given the additional information that the expected return is zero and the current value of the position is $10 million, calculate VaR at 99%, using the nonparametric method. Problem 5 Given the following data on your actual cumulative distribution of daily returns, versus normal: 0% Return (0.0460) (0.0404) (0.0348) (0.0291) (0.0235) (0.0179) (0.0123) (0.0067) (0.0010) 0.0046 0.0102 0.0158 0.0214 0.0271 0.0327 0.0330 Actual Normal Cumulative Cumulative Distribution Distribution 0.40% 0% 1.00% 1.20% 0% 1.60% 0% 3.20% 1% 3.20% 4% 8.40% 12% 18.80% 26% 42.00% 46% 65.80% 67% 80.00% 84% 92.40% 94% 96.80% 98% 99.20% 100% 99.30% 100% 100.00% 100% Given the additional information that the expected return is zero and the current value of the position is $10 million, calculate VaR at 99%, using the nonparametric method

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts