Question: Problem 5 We have one risk-free asset with a return rf=0.06 (i.e., 6% ) and one risky asset. There are three states of nature. State

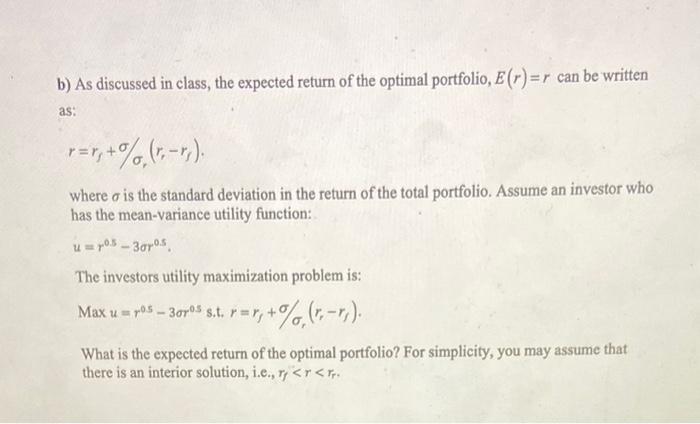

Problem 5 We have one risk-free asset with a return rf=0.06 (i.e., 6% ) and one risky asset. There are three states of nature. State 1 occurs with a probability of p1=0.25, State 2 occurs with a probability of p2=0.50, and State 3 with a probability of p3=0.25. The rate of return in the different states are r1=0.00,r2=0.12, and r3=0.20. b) As discussed in class, the expected return of the optimal portfolio, E(r)=r can be written as: r=rf+/r(rrrf) where is the standard deviation in the return of the total portfolio. Assume an investor who has the mean-variance utility function: u=r0.53r0.5. The investors utility maximization problem is: Maxu=r0.53r05s.t.r=rf+/r(rrrf). What is the expected return of the optimal portfolio? For simplicity, you may assume that there is an interior solution, i.e., rf

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts