Question: Problem 5.1 (21.29 in Hull) Answer the following questions concerned with the alternative procedures for constructing trees in Section 21.4. See below for the relevant

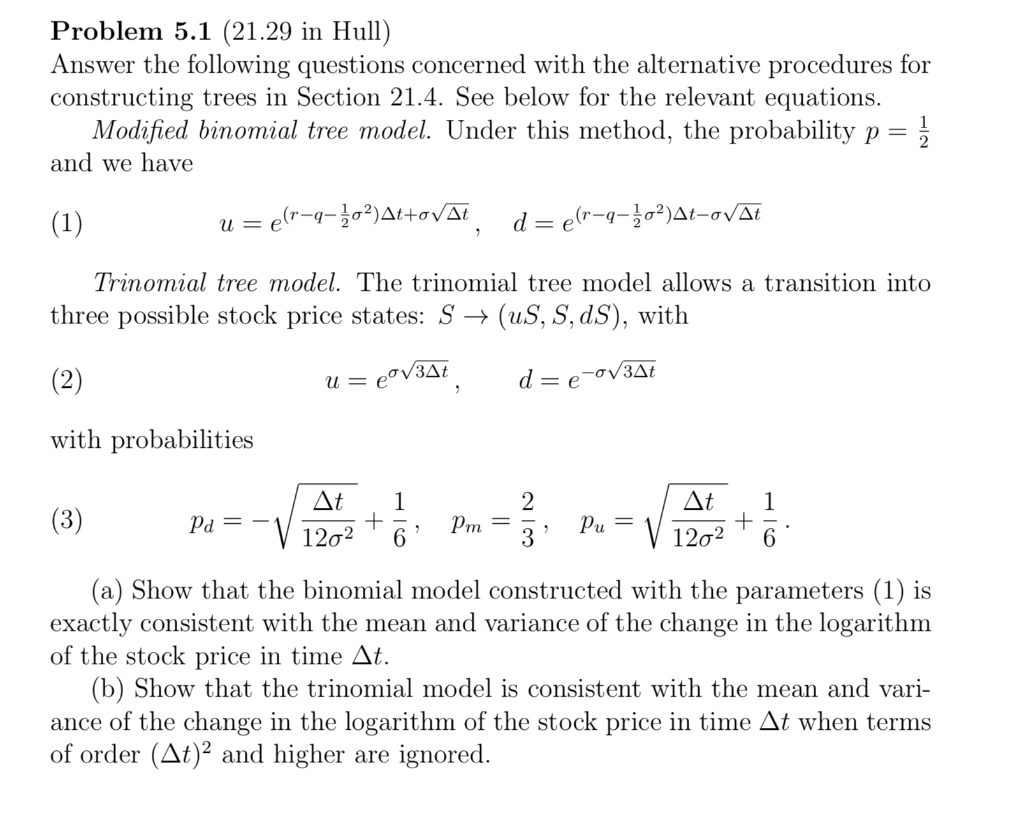

Problem 5.1 (21.29 in Hull) Answer the following questions concerned with the alternative procedures for constructing trees in Section 21.4. See below for the relevant equations. Modified binomial tree model. Under this method, the probability p= } and we have (1) u= e(r-9-102)At+ovat d= e(r-9-102)At-ovat Trinomial tree model. The trinomial tree model allows a transition into three possible stock price states: S + (US, S, dS), with (2) u= pov3At, d=e-0/3At with probabilities (3) (a) Show that the binomial model constructed with the parameters (1) is exactly consistent with the mean and variance of the change in the logarithm of the stock price in time At. (b) Show that the trinomial model is consistent with the mean and vari- ance of the change in the logarithm of the stock price in time At when terms of order (At)2 and higher are ignored. Problem 5.1 (21.29 in Hull) Answer the following questions concerned with the alternative procedures for constructing trees in Section 21.4. See below for the relevant equations. Modified binomial tree model. Under this method, the probability p= } and we have (1) u= e(r-9-102)At+ovat d= e(r-9-102)At-ovat Trinomial tree model. The trinomial tree model allows a transition into three possible stock price states: S + (US, S, dS), with (2) u= pov3At, d=e-0/3At with probabilities (3) (a) Show that the binomial model constructed with the parameters (1) is exactly consistent with the mean and variance of the change in the logarithm of the stock price in time At. (b) Show that the trinomial model is consistent with the mean and vari- ance of the change in the logarithm of the stock price in time At when terms of order (At)2 and higher are ignored

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts