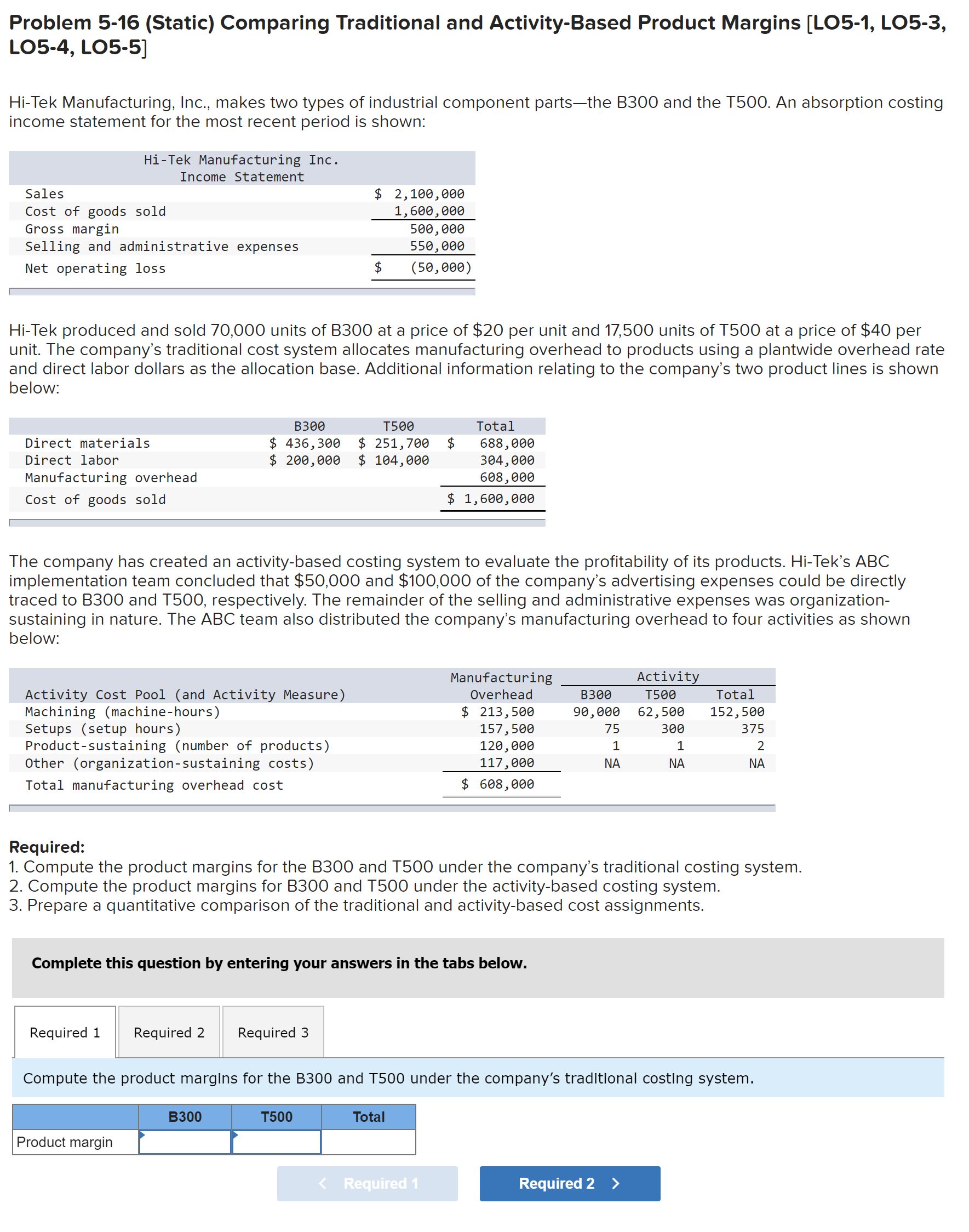

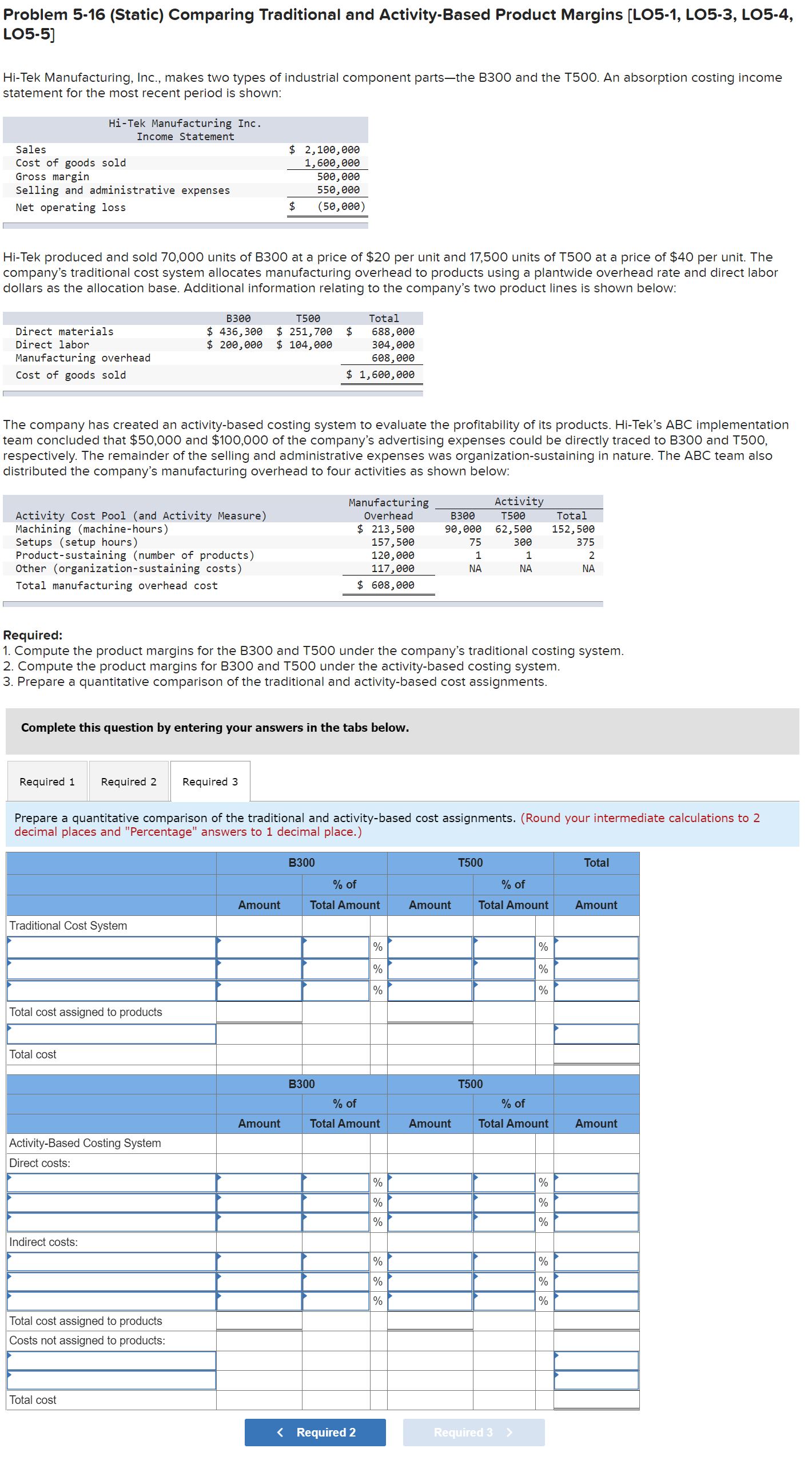

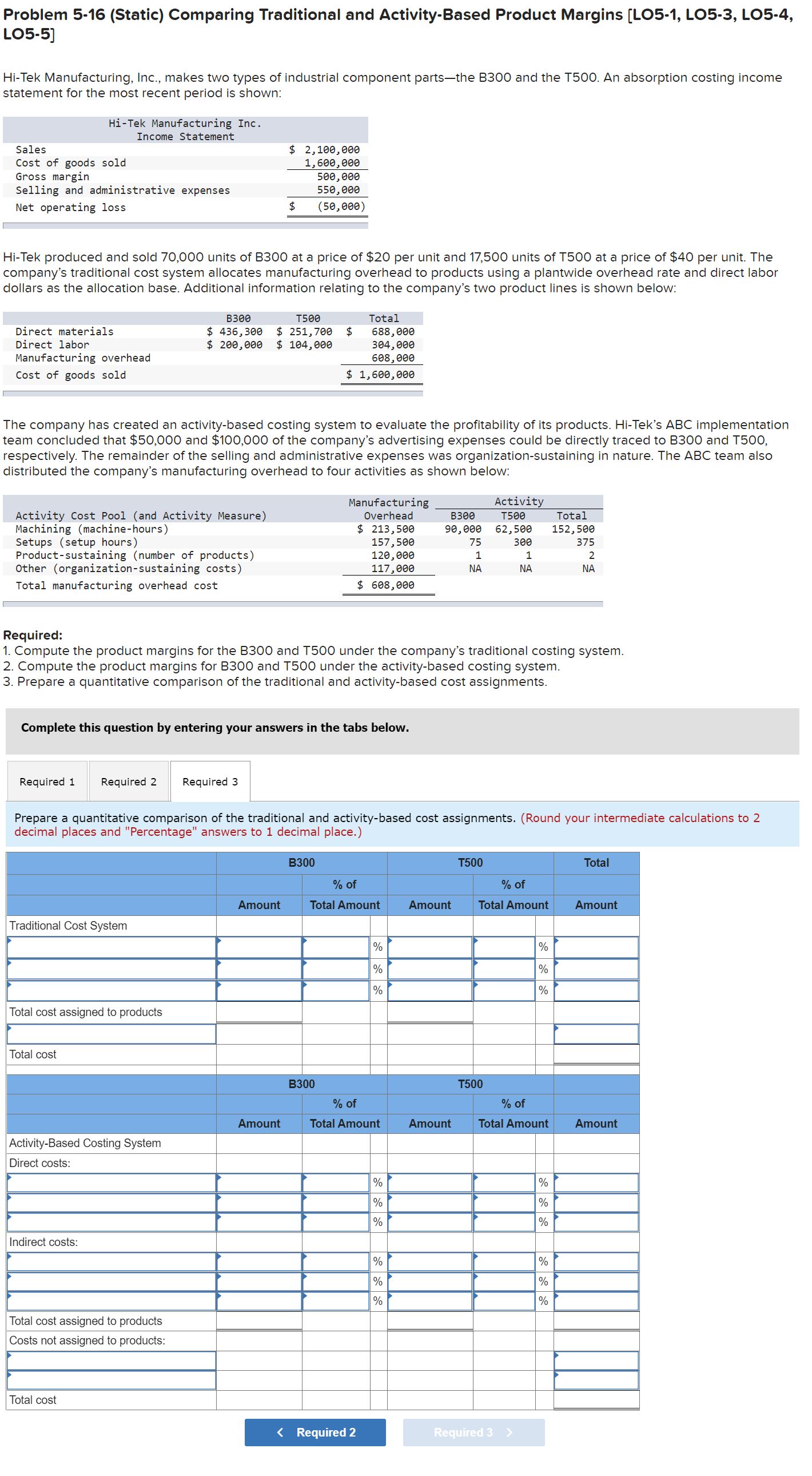

Question: Problem 5-16 (Static) Comparing Traditional and Activity-Based Product Margins [L05-1, L05-3, L05-4, L05-5] HiTek Manufacturing, Inc., makes two types of industrial component partsthe B300 and

![L05-4, L05-5] HiTek Manufacturing, Inc., makes two types of industrial component partsthe](https://s3.amazonaws.com/si.experts.images/answers/2024/06/667b5b57b1d20_343667b5b57984d5.jpg)

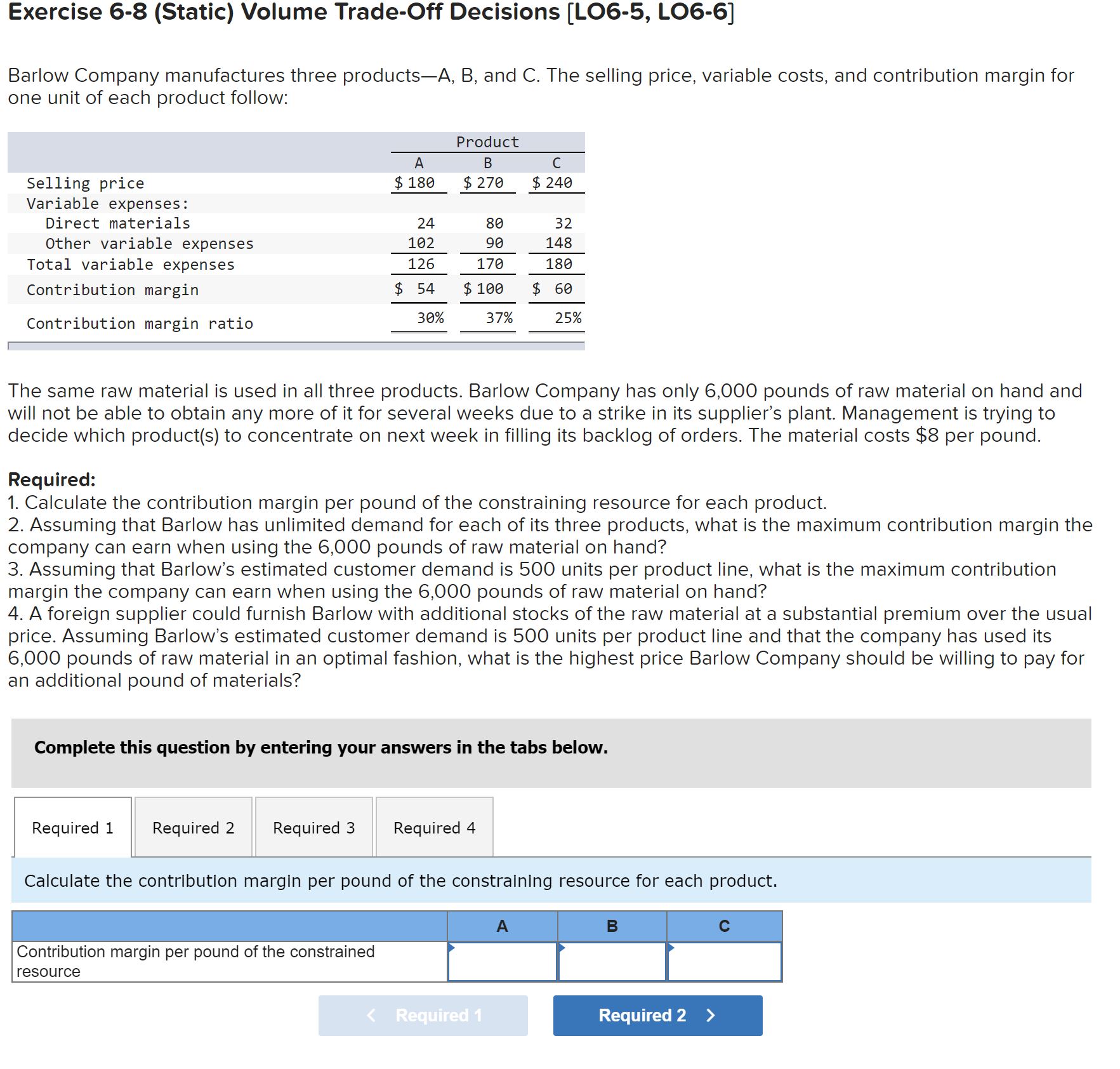

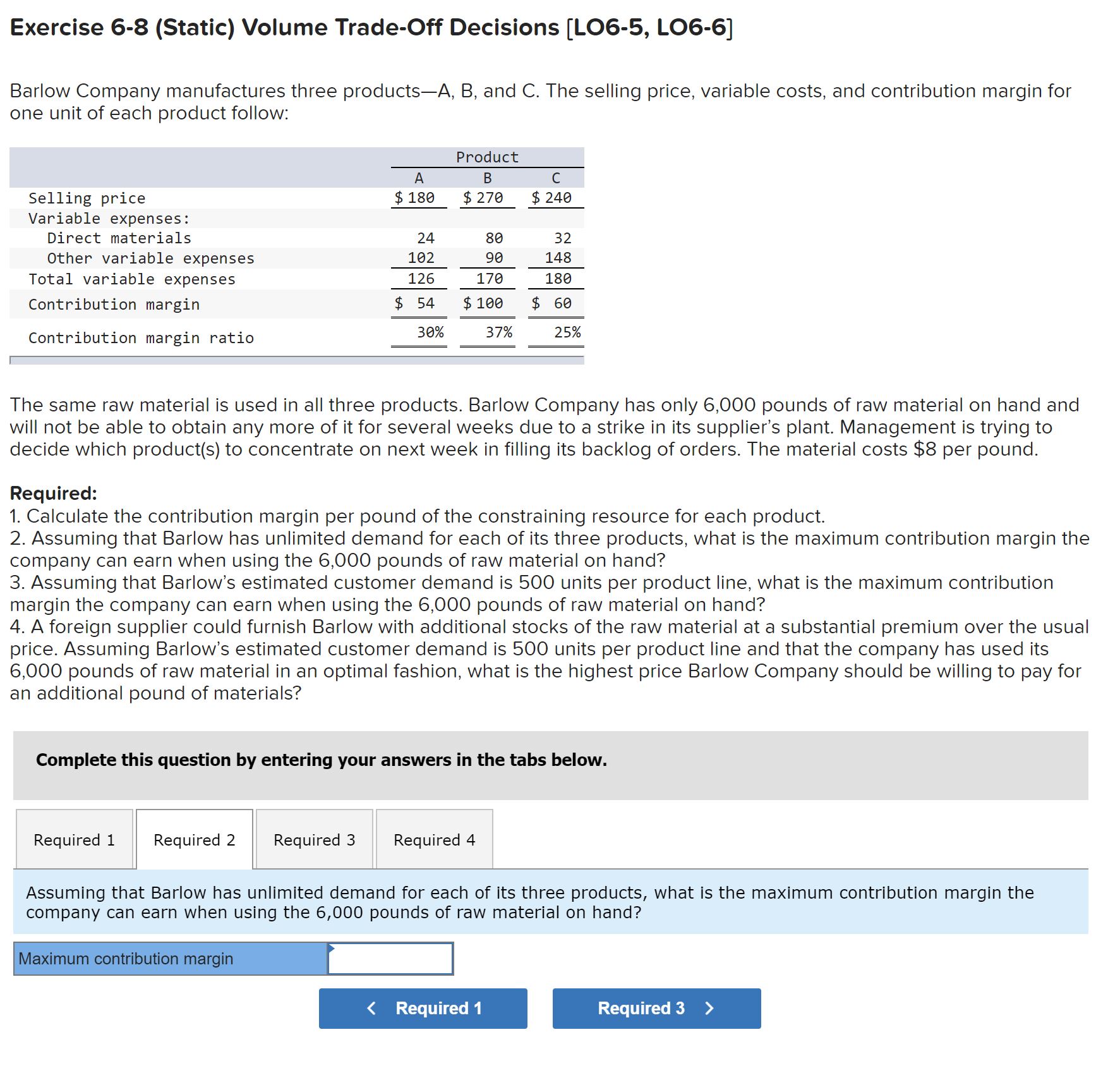

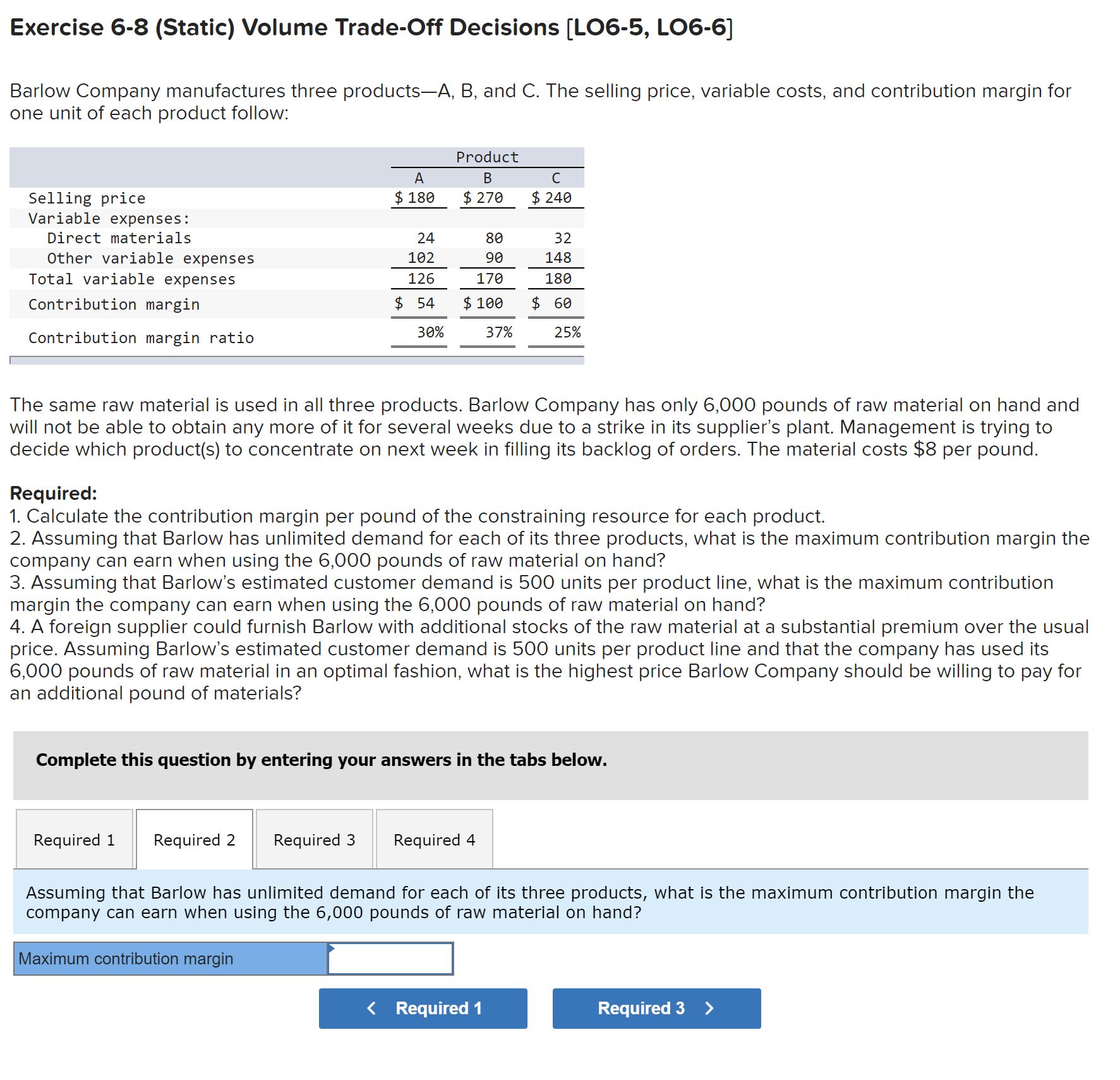

Problem 5-16 (Static) Comparing Traditional and Activity-Based Product Margins [L05-1, L05-3, L05-4, L05-5] HiTek Manufacturing, Inc., makes two types of industrial component partsthe B300 and the T500. An absorption costing income statement for the most recent period is shown: HiTek Manufacturing Inc. Income Statement Sales :3 2,199,999 Cost of goods sold 1,666,666 Gross margin 566,666 Selling and administrative expenses 556,666 Net operating loss $ (56,666) HiTek produced and sold 70,000 units of B300 at a price of $20 per unit and 17,500 units of T500 at a price of $40 per unit. The company's traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company's two product lines is shown below: B366 T566 Total Direct materials 3 436,366 $ 251,766 $ 688,666 Direct labor $ 266,666 $ 164,666 364,666 Manufacturing overhead 668,666 Cost of goods sold $ 1,666,666 The company has created an activitybased costing system to evaluate the profitability of its products. HiTek's ABC implementation team concluded that $50,000 and $100,000 of the company's advertising expenses could be directly traced to B300 and T500, respectively. The remainder of the selling and administrative expenses was organization sustaining in nature. The ABC team also distributed the company's manufacturing overhead to four activities as shown below: Manufacturing $ Activity Cost Pool (and Activity Measure) Overhead B366 T566 Total Machining (machinehours) $ 213,566 96,666 62,566 152,566 Setups (setup hours) 157,566 75 366 375 Productsustaining (number of products) 126,666 1 1 2 other (organizationsustaining costs) 117,666 NA NA NA Total manufacturing overhead cost $ 668,666 Required: 1. Compute the product margins for the B300 and T500 under the company's traditional costing system. 2. Compute the product margins for 8300 and T500 under the activitybased costing system. 3. Prepare a quantitative comparison of the traditional and activitybased cost assignments. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Compute the product margins for the B300 and T500 under the company's traditional costing system. Required 2 > Problem 5-16 (Static) Comparing Traditional and Activity-Based Product Margins [L05-1, L05-3, L05-4, L05-5] Hi-Tek Manufacturing, Inc., makes two types of industrial component partsthe B300 and the T500. An absorption costing income statement for the most recent period is shown: HiTek Manufacturing Inc. Income Statement Sales $ 2,100,000 Cost O'F goods sold 1,600,000 Gross margin 500,000 Selling and administrative expenses 550,000 Net operating loss $ (50,000) HiTek produced and sold 70,000 units of B300 at a price of $20 per unit and 17,500 units of T500 at a price of $40 per unit. The company's traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company's two product lines is shown below: 3300 T500 Total Direct materials $ 436,300 $ 251,700 $ 688,000 Direct labor $ 200,000 $ 104,000 304,000 Manufacturing overhead 608,000 Cost of goods sold $ 1,600,000 The company has created an activitybased costing system to evaluate the profitability of its products. HiTek's ABC implementation team concluded that $50,000 and $100,000 of the company's advertising expenses could be directly traced to 8300 and T500, respectively. The remainder of the selling and administrative expenses was organization sustaining in nature. The ABC team also distributed the company's manufacturing overhead to four activities as shown below: Manufacturing $ Activity Cost Pool (and Activity Measure) Overhead 3300 T500 Total Machining (machinehours) $ 213,500 90,000 62,500 152,500 Setups (setup hours) 157,500 75 300 375 Productsustaining (number of products) 120,000 1 1 2 Other (organizationsustaining costs) 117,000 NA NA NA Total manufacturing overhead cost $ 698,999 Required: 1, Compute the product margins for the B300 and T500 under the company's traditional costing system. 2. Compute the product margins for B300 and T500 under the activitybased costing system. 3. Prepare a quantitative comparison of the traditional and activitybased cost assignments Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Compute the product margins for B300 and T500 under the activitybased costing system. (Negative product margins should be indicated by a minus sign. Round your intermediate calculations to 2 decimal places.) Problem 5-16 (Static) Comparing Traditional and Activity-Based Product Margins [L05-1, L05-3, L05-4. LOB-5] Hi-Tek Manufacturing, lnc., makes two types of industrial component partsthe B300 and the T500. An absorption costing income statement for the most recent period is shown: Hi-Tli ManufaCturing Inc. Income statement Sales 3 2,199,999 Cost of goods sold 1,688,888 Gross margin 588,888 Selling and administrative expenses 558,888 Net operating loss $ (58,888) Hi-Tek produced and sold 70,000 units of B300 at a price of $20 per unit and 17,500 units of T500 at a price of $40 per unit. The company's traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company's two product lines is shown below: 5399 T599 Tutal Direct materials 3 436,388 $ 251,788 $ 688,888 Direct labor 3 299,999 $ 194,999 394,999 Manufacturing overhead 688,888 Cost of goods sold 3 1,688,888 The company has created an activity-based costing system to evaluate the profitability of its products. Hi-Tek's ABC implementation team concluded that $50,000 and $100,000 of the company's advertising expenses could be directly traced to B300 and T500, respectively. The remainder of the selling and administrative expenses was organization-sustaining in nature. The ABC team also distributed the company's manufacturing overhead to four activities as shown below: , ,_ _, Manufacturing Activity Cost Pool (and Activity Measure) Overhead 5399 159,9 Tptal Machining (machine-hours) $ 215,588 98,888 62,588 152,588 Setups (setup hours) 157,588 75 388 375 Product-sustaining (number of products) 128,888 1 1 2 other (organization-sustaining costs) 117,888 NA NA NA Total manufacturing overhead cost $ 688,888 Required: 1. Compute the product margins for the 8300 and T500 under the compa ny's traditional costing system. 2. Compute the product margins for B300 and T500 under the activity-based costing system. 3. Prepare a quantitative comparison of the traditional and activity-based cost assignments. Complete this question by entering your answers in die tabs below. ' Required 1 ' Required 2 Required3 Prepare a quantitative comparison of the traditional and activity-based cost assignments. (Round your intermediate calculations to 2 decimal places and "Percentage" answers to 1 decimal place.) Traditional Cost System Total cost assigned to products :| Total cost Activity-Based Costing System Direct costs: % % % % % % indirect costs: % " % % % % Total cost assigned to products Costs not assigned to products: Total cost Exercise 6-8 (Static) Volume Trade-Off Decisions [LOG-5, LO6-6] Barlow Company manufactures three productsA, B, and C. The selling price, variable costs, and contribution margin for one unit of each product follow: Product A B C Selling price $ 186 $ 279 $ 240 Variable expenses: Direct materials 24 8a 32 other variable expenses 162 99 148 Total variable expenses 126 179 180 Contribution margin $ 54 $199 $ 66 Contribution margin ratio 39% 37% 25% The same raw material is used in all three products. Barlow Company has only 6,000 pounds of raw material on hand and will not be able to obtain any more of it for several weeks due to a strike in its suppliers plant. Management is trying to decide which product(s) to concentrate on next week in filling its backlog of orders. The material costs $8 per pound. Required: 1. Calculate the contribution margin per pound of the constraining resource for each product. 2. Assuming that Barlow has unlimited demand for each of its three products, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? 3. Assuming that Barlow's estimated customer demand is 500 units per product line, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? 4. A foreign supplier could furnish Barlow with additional stocks of the raw material at a substantial premium over the usual price. Assuming Barlow's estimated customer demand is 500 units per product line and that the company has used its 6,000 pounds of raw material in an optimal fashion, what is the highest price Barlow Company should be willing to pay for an additional pound of materials? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Assuming that Barlow has unlimited demand for each of its three products, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? Required 3 Required 4 Exercise 6-8 (Static) Volume Trade-Off Decisions [LOG-5, LOG-6] Barlow Company manufactures three productsA, B, and C. The selling price, variable costs, and contribution margin for one unit of each product follow: Product A B C Selling price $180 $ 279 $240 Variable expenses: Direct materials 24 8e 32 Other variable expenses 162 90 148 Total variable expenses 126 179 186 Contribution margin $ 54 $ 100 $ 69 Contribution margin ratio 39% 37% 25% The same raw material is used in all three products. Barlow Company has only 6,000 pounds of raw material on hand and will not be able to obtain any more of it for several weeks due to a strike in its supplier's plant. Management is trying to decide which product(s) to concentrate on next week in filling its backlog of orders. The material costs $8 per pound. Required: 1. Calculate the contribution margin per pound of the constraining resource for each product. 2. Assuming that Barlow has unlimited demand for each of its three products, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? 3. Assuming that Barlow's estimated customer demand is 500 units per product line, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? 4. A foreign supplier could furnish Barlow with additional stocks of the raw material at a substantial premium over the usual price. Assuming Barlow's estimated customer demand is 500 units per product line and that the company has used its 6,000 pounds of raw material in an optimal fashion, what is the highest price Barlow Company should be willing to pay for an additional pound of materials? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Required 4 Assuming that Barlow's estimated customer demand is 500 units per product line, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? Exercise 6-8 (Static) Volume Trade-Off Decisions [LO6-5, LOG-6] Barlow Company manufactures three productsA, B, and C. The selling price, variable costs, and contribution margin for one unit of each product follow: Product A B C Selling price $ 186 $ 279 $ 240 Variable expenses: Direct materials 24 89 32 Other variable expenses 162 98 148 Total variable expenses 126 179 186 Contribution margin $ 54 $ 108 $ 6% Contribution margin ratio 36% 37% 25% The same raw material is used in all three products. Barlow Company has only 6,000 pounds of raw material on hand and will not be able to obtain any more of it for several weeks due to a strike in its supplier's plant. Management is trying to decide which product(s) to concentrate on next week in filling its backlog of orders. The material costs $8 per pound. Required: 1. Calculate the contribution margin per pound of the constraining resource for each product. 2. Assuming that Barlow has unlimited demand for each of its three products, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? 3. Assuming that Barlow's estimated customer demand is 500 units per product line, what is the maximum contribution margin the company can earn when using the 6,000 pounds of raw material on hand? 4. A foreign supplier could furnish Barlow with additional stocks of the raw material at a substantial premium over the usual price. Assuming Barlow's estimated customer demand is 500 units per product line and that the company has used its 6,000 pounds of raw material in an optimal fashion, what is the highest price Barlow Company should be willing to pay for an additional pound of materials? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Required 4 A foreign supplier could furnish Barlow with additional stocks of the raw material at a substantial premium over the usual price. Assuming Barlow's estimated customer demand is 500 units per product line and that the company has used its 6,000 pounds of raw material in an optimal fashion, what is the highest price Barlow Company should be willing to pay for an additional pound of materials? Show lessA

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts