Question: Problem 6 - 5 ( Algo ) The standard deviation of the market - index portfolio is 2 0 % . Stock A has a

Problem Algo

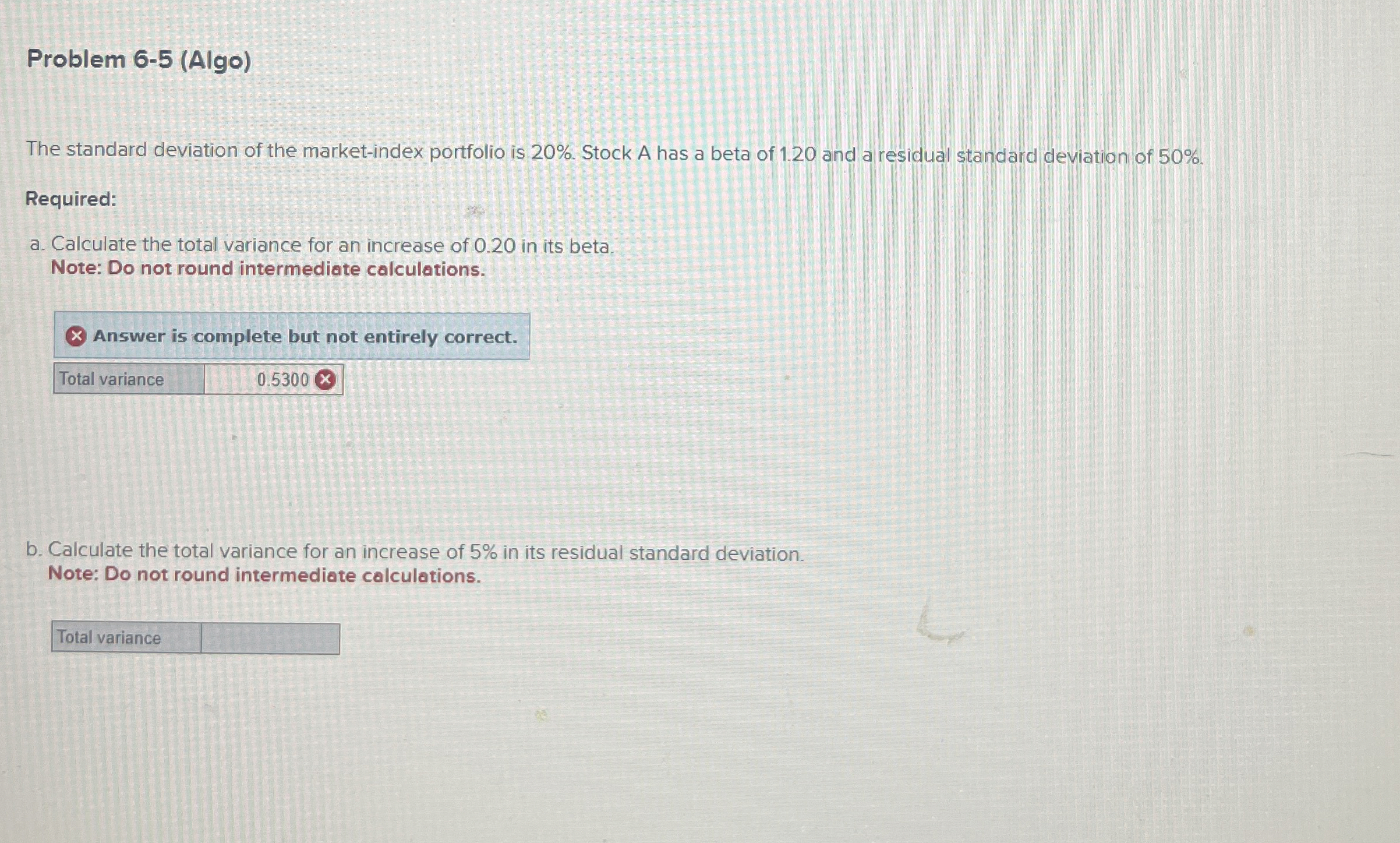

The standard deviation of the marketindex portfolio is Stock A has a beta of and a residual standard deviation of

Required:

a Calculate the total variance for an increase of in its beta.

Note: Do not round intermediate calculations.

Answer is complete but not entirely correct.

tableTotal variance,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock