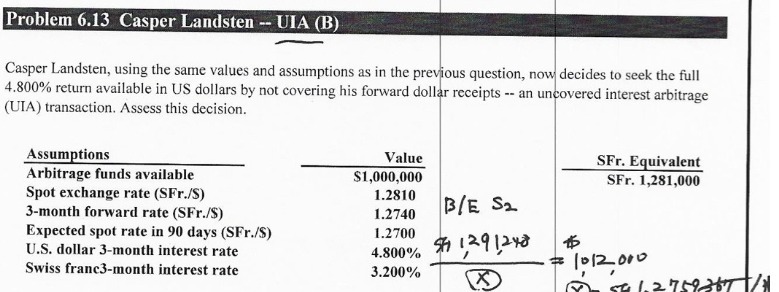

Question: Problem 6.13 Casper Landsten -- UIA (B) Casper Landsten, using the same values and assumptions as in the previous question, now decides to seek the

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock