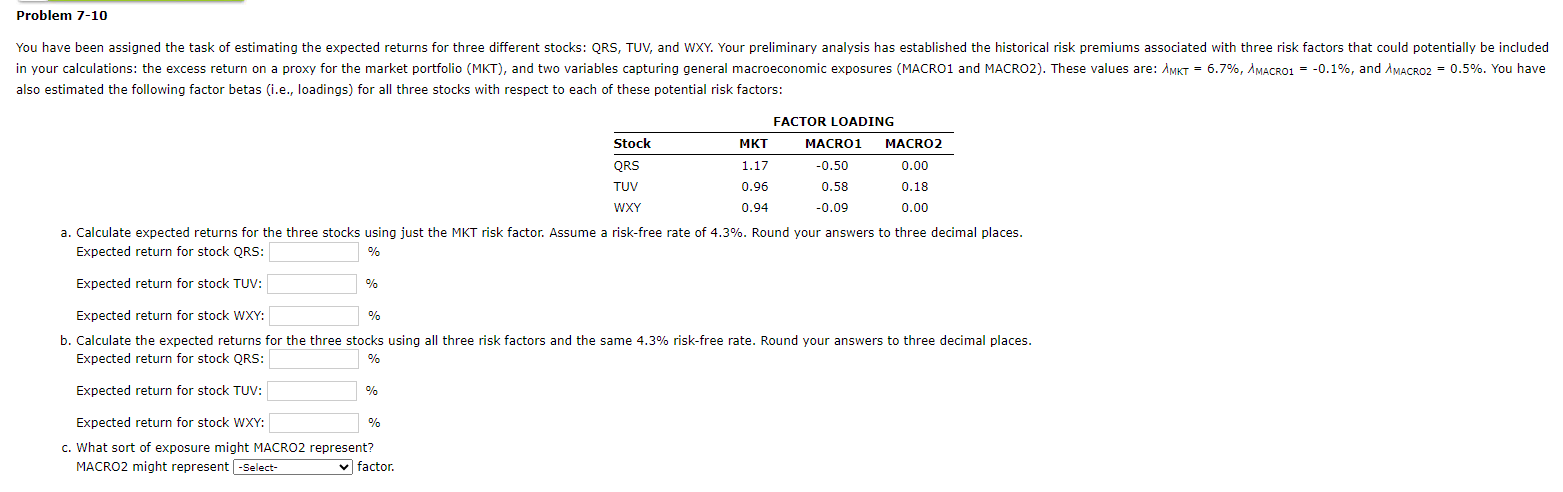

Question: Problem 7 - 1 0 also estimated the following factor betas ( i . e . , loadings ) for all three stocks with respect

Problem

also estimated the following factor betas ie loadings for all three stocks with respect to each of these potential risk factors:

FACTOR LOADING

a Calculate expected returns for the three stocks using just the MKT risk factor. Assume a riskfree rate of Round your answers to three decimal places.

Expected return for stock QRS:

Expected return for stock TUV:

Expected return for stock WXY:

b Calculate the expected returns for the three stocks using all three risk factors and the same riskfree rate. Round your answers to three decimal places.

Expected return for stock QRS:

Expected return for stock TUV:

Expected return for stock WXY:

c What sort of exposure might MACRO represent?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock