Question: PROBLEM 7 Consider a two-state Markov chain. Suppose that each state E {1,2} offers with the following two (1) choices of rewards r. and transition

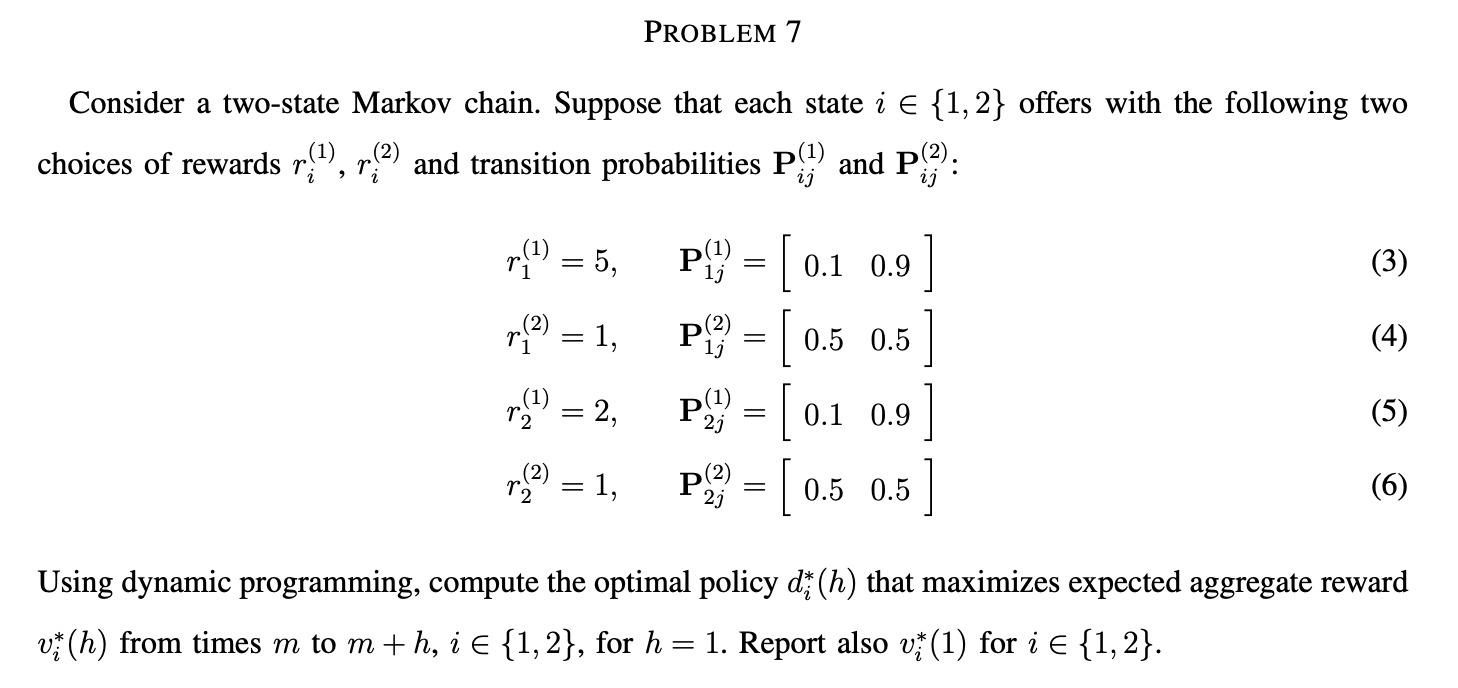

PROBLEM 7 Consider a two-state Markov chain. Suppose that each state E {1,2} offers with the following two (1) choices of rewards r. and transition probabilities P{}) and P?): 2 i (3) r!) = 5, (2) = 1, (4) P} = [0.1 0.9] pl? = [0.5 0.5 ] P = [ 0.1 0.9 ] P= (0.5 0.5 0.5] 2) = 2, (5) m2 = 1, (6) Using dynamic programming, compute the optimal policy di (h) that maximizes expected aggregate reward vi (h) from times m to m+h, i E {1,2}, for h = 1. Report also vf (1) for i E {1,2}. PROBLEM 7 Consider a two-state Markov chain. Suppose that each state E {1,2} offers with the following two (1) choices of rewards r. and transition probabilities P{}) and P?): 2 i (3) r!) = 5, (2) = 1, (4) P} = [0.1 0.9] pl? = [0.5 0.5 ] P = [ 0.1 0.9 ] P= (0.5 0.5 0.5] 2) = 2, (5) m2 = 1, (6) Using dynamic programming, compute the optimal policy di (h) that maximizes expected aggregate reward vi (h) from times m to m+h, i E {1,2}, for h = 1. Report also vf (1) for i E {1,2}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts