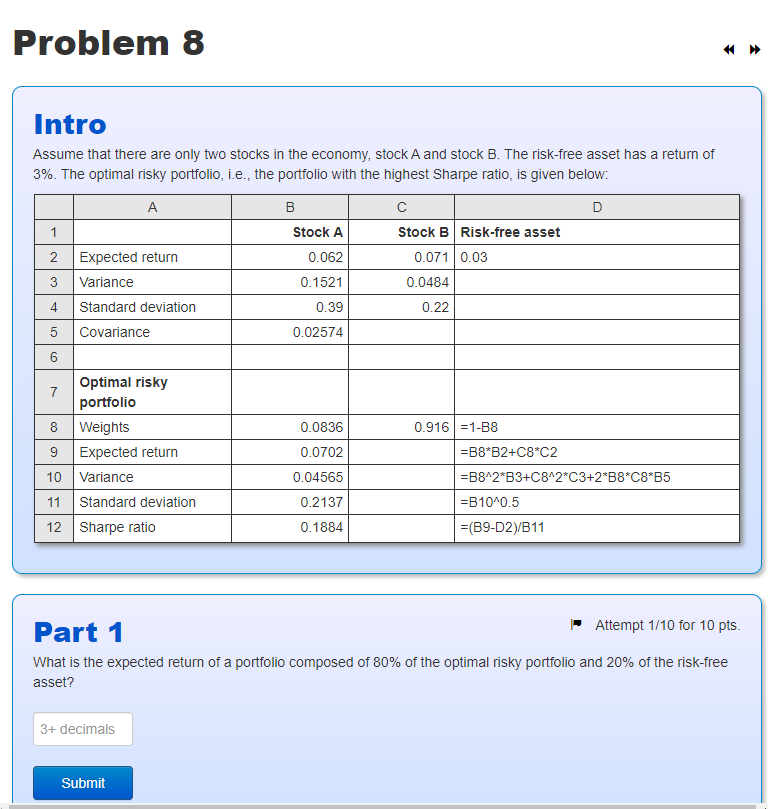

Question: Problem 8 Intro Assume that there are only two stocks in the economy, stock A and stock B. The risk-free asset has a return of

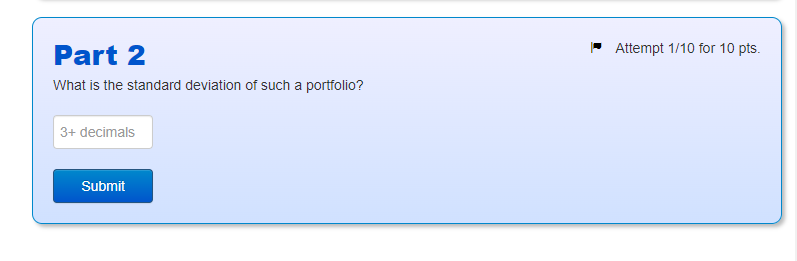

Problem 8 Intro Assume that there are only two stocks in the economy, stock A and stock B. The risk-free asset has a return of 3%. The optimal risky portfolio, i.e., the portfolio with the highest Sharpe ratio, is given below: B D 1 Stock A 0.062 Stock B Risk-free asset 0.071 0.03 0.0484 0.22 3 0.1521 0.39 0.02574 2 Expected return 3 Variance 4 Standard deviation 5 Covariance 6 Optimal risky 7 portfolio 8 Weights 9 Expected return 10 Variance 11 Standard deviation 12 Sharpe ratio 0.0836 0.0702 0.04565 0.916 =1-B8 =B8*B2+C8 C2 =B842*B3+C842*C3+2*B8*C8%B5 =B10^0.5 =(B9-D2/B11 0.2137 0.1884 Part 1 Attempt 1/10 for 10 pts. What is the expected return of a portfolio composed of 80% of the optimal risky portfolio and 20% of the risk-free asset? 3+ decimals Submit Attempt 1/10 for 10 pts. Part 2 What is the standard deviation of such a portfolio? 3+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts