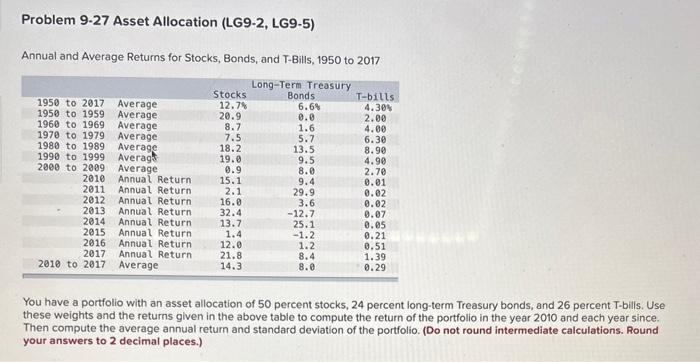

Question: Problem 9-27 Asset Allocation (LG9-2, LG9-5) Annual and Average Returns for Stocks, Bonds, and T-Bills, 1950 to 2017 You have a portfolio with an asset

Problem 9-27 Asset Allocation (LG9-2, LG9-5) Annual and Average Returns for Stocks, Bonds, and T-Bills, 1950 to 2017 You have a portfolio with an asset allocation of 50 percent stocks, 24 percent long-term Treasury bonds, and 26 percent T-bills. Use these weights and the returns given in the above table to compute the return of the portfolio in the year 2010 and each year since. Then compute the average annual return and standard deviation of the portfolio. (Do not round intermediate calculations. Round your answers to 2 decimal places.) \begin{tabular}{|l|l|l|} \hline & \multicolumn{2}{|c|}{ Portfolio Return } \\ \hline 2010 & & % \\ \hline 2011 & & % \\ \hline 2012 & & % \\ \hline 2013 & & % \\ \hline 2014 & & % \\ \hline 2015 & & % \\ \hline 2016 & & % \\ \hline 2017 & & % \\ \hline Average & & % \\ \hline & & \\ \hline Standard deviation & & \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts