Question: Problem I. Part A. Use the following fact pattern to answer the following 7 questions, with sub-instructions for particular questions: On January 1, 2018, Parent

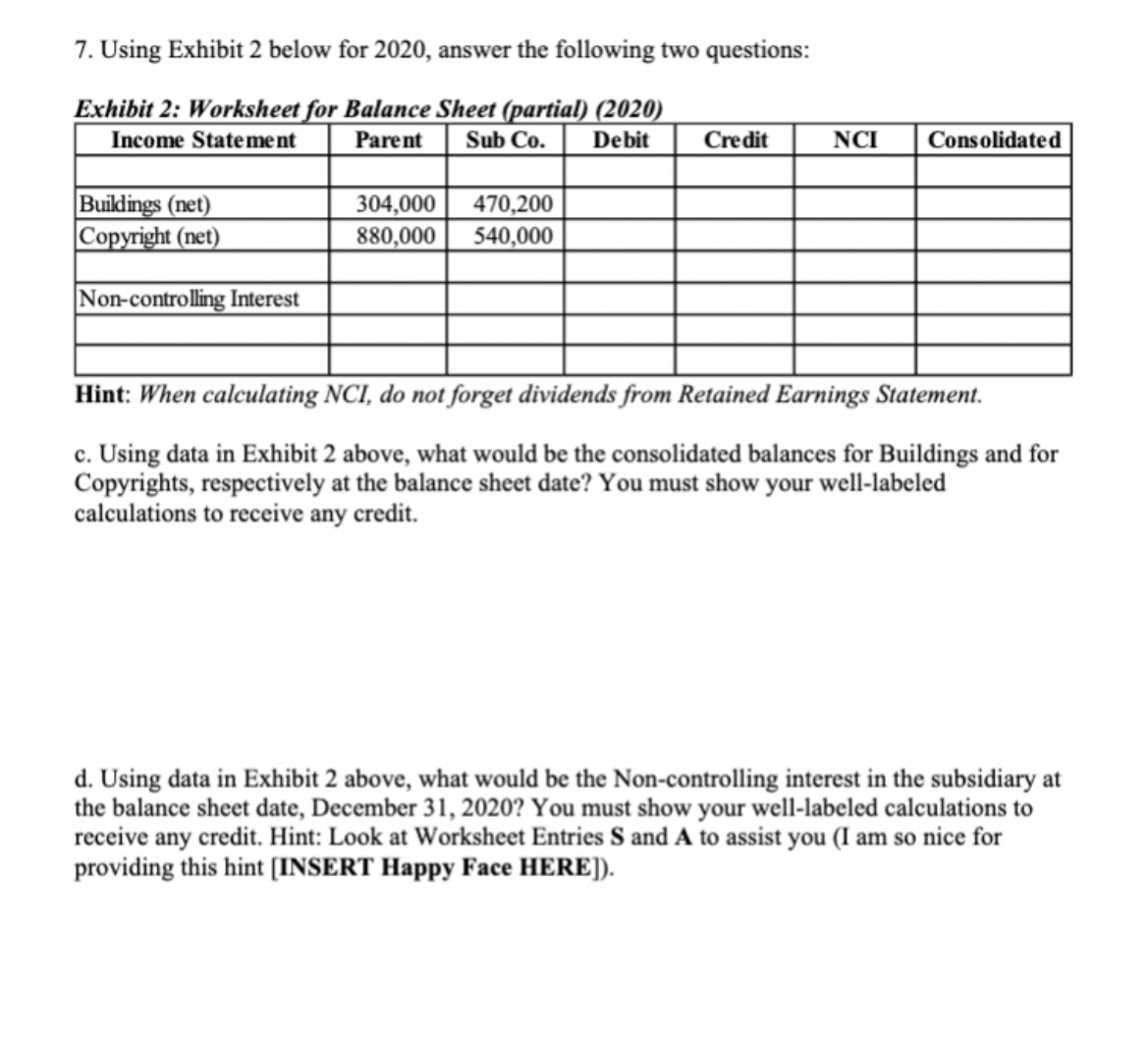

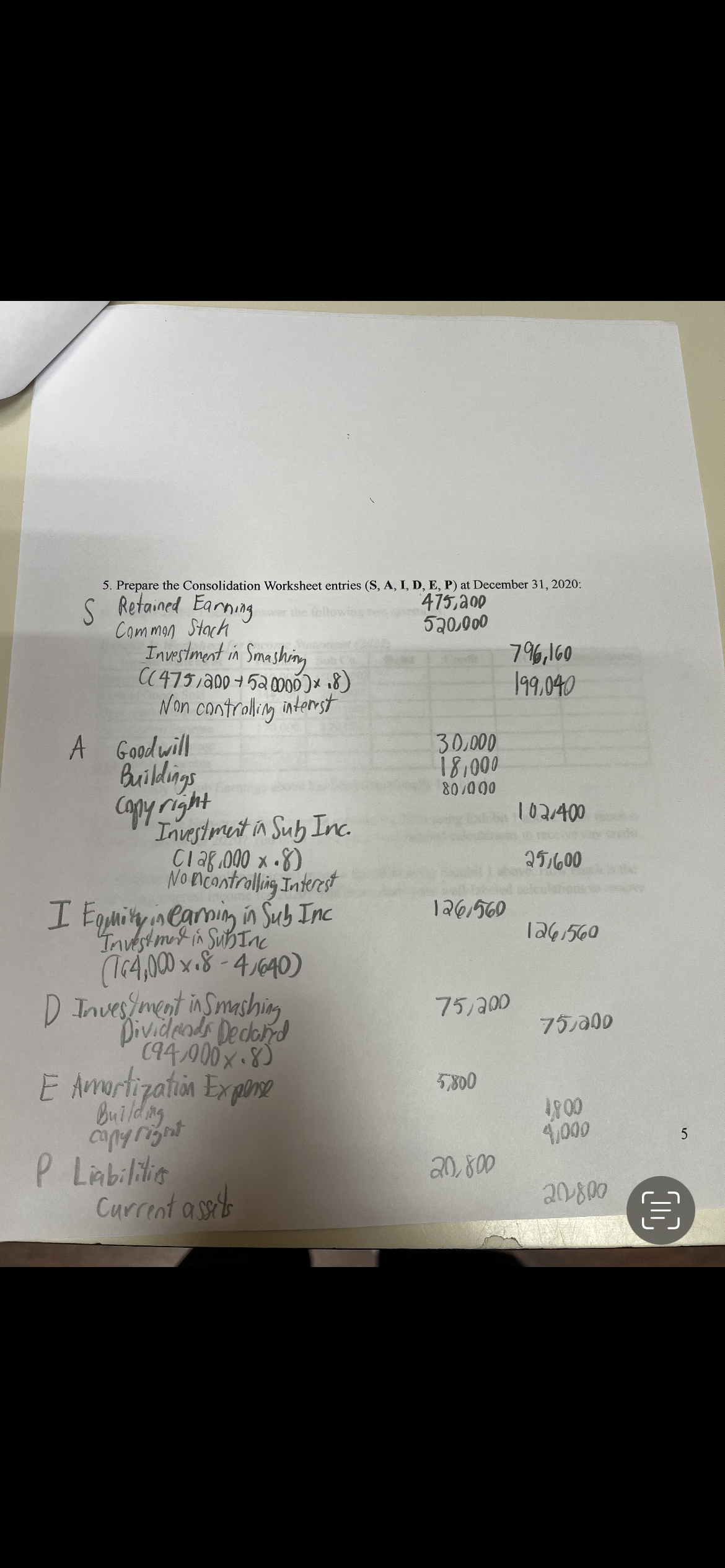

Problem I. Part A. Use the following fact pattern to answer the following 7 questions, with sub-instructions for particular questions: On January 1, 2018, Parent Co. acquired 80% of Sub Inc. by paying $800,000. Non-controlling interest was valued at $200,000. Sub reported common stock on that date of $520,000 with retained earnings of $352,000. A building was undervalued in the company's financial records by $18,000. This building had a ten-year remaining life. Copyrights of $80,000 were not recognized and should be amortized over 20 years. Sub earned income and paid cash dividends as follows: Net Income Dividends Paid 2018 $115,000 $64,600 2019 $144,400 $71,600 2020 $164,000 $94,000 On December 31, 2020, the Parent owed $20,800 to Sub Inc. There have been no changes in Sub's common stock account since the acquisition. 1. Prepare the allocation of the acquisition on January 1, 2018. In your presentation, but sure to show the excess fair value over cost allocated to the identifiable assets, and any resulting goodwill. In addition, for the identifiable assets, be sure to calculate the annual amortization of excess fair value over book value. FV of consideration paid = $800,000 $520, 000 non controlling interest 200,000 + $1352, 000 Total consideration 0 00 '000' 1 5 $1872, 000 Excess of FV over BV 251 100 $ 1,000,000 - 15872,000 =$128, 000 Allocation of Excess FV : Building: $118,000 _$1,800 eachyr x 3 yrs = $5, 400 10 Copyrights : $80, 000 = $4,000 eachyr x 3 yrs = $12, 000 20 Goodwill: $128,000- 15,400 - 512,000 = $110,600 26. Using Exhibit 1 below, answer the following two questions: Exhibit 1: Worksheet for Income Statement (2020) Income Statement Parent Sub Co. Debit Credit NCI Consolidated Revenues (810,000) (504,000) Cost of Goods Sold 344,000 200,000 Depreciation Expense 60,000 20,000 Amortization Expense 170,000 120,000 Equity in Sub Earnings Separate Net Income Note: Equity in Sub Earnings above has been intentionally left blank. a. Calculate the Non-controlling interest income for 2020 using Exhibit 1 above. How much is the NCI income for 2020? You must show your well-labeled calculations to receive any credit. b. Calculate the controlling interest income for 2020 using Exhibit 1 above. How much is the controlling interest income for 2020? You must show your well-labeled calculations to receive any credit.2. Prepare journal entries that Parent is required to record associated with the investment under the Equity Method in 2020 before preparing the consolidation worksheet. Investment in Sub co 131/200 Equity in sub earnings 131/200 ( 164,009 x18) Dividends Receivable 75,200 Investment in SubCo 75 200 (94000 *. 80) Equity in Sub earning 4/ 640 Investment in SubCo 4640 (5800 x. 8 ) 3. Prepare a T-account for the Investment in Sub Co. account from the acquisition in 2018 up through the end of 2020. Be sure to neatly label each item, showing account balances at the end of each year (2018, 2019, and 2020). Investment in Subco. 1/1/18 $ 890,000 92.090 12/31/28 $4 640 (5, 800 x18) 12/3418 ( 115, 000 x.8 ) 51/ 480 Bal 12/3 1/18 $835, 680 (64/600 x8) 12/31/19 115, 520 12/31/19 4 6 40 ( 114 , 400 x-8 ) 57, 280 (71, 600 x.8) Bal 12/31/ 19 $ 889, 280 12/31/20 131, 200 12/31/20 3 ( 164 ,000 x18) 75,209 (94, 000 x8 ) Bal 12631/ 20 $ 940, 6404. Prepare a T-account for the Retained Earnings of Sub Co. account from 2018 up through the end of 2020. Be sure to neatly label each item, showing account balances at the end of each year. (2018, 2019, and 2020). Retained earning 1, 2020 3521000 1/1/ 18 50/400 ( 115, 00 0- 64, 600 ) 2018 402 / 400 12/31/18 721 800 C 144, 400- 71, 600) 2019 475 200 12/31/19 70, 000 (164,000 -94, 009) 2020 545, 200 12/31/20 end balance7. Using Exhibit 2 below for 2020, answer the following two questions: Exhibit 2: Worksheet for Balance Sheet (partial) (2020) Income Statement Parent Sub Co. Consolidated Buildings (net) 304,000 470,200 Copyright (net) 880,000 540,000 Non-controlling Interest c. Using data in Exhibit 2 above, what would be the consolidated balances for Buildings and for Copyrights, respectively at the balance sheet date? You must show your well-labeled calculations to receive any credit. d. Using data in Exhibit 2 above, what would be the Non-controlling interest in the subsidiary at the balance sheet date, December 31, 2020? You must show your well-labeled calculations to receive any credit. Hint: Look at Worksheet Entries S and A to assist you (I am so nice for providing this hint [INSERT Happy Face HERE]).5. Prepare the Consolidation Worksheet entries (S, A, I, D, E, P) at December 31, 2020: S Retained Earning over the following 475,200 Common stack 520,000 Investment in Smashing 796, 160 ((475, 200 + 520000 ) x 18 ) 199, 040 Non controlling interest A Goodwill 30, 000 Buildings 181000 copyright 80/0 00 Investment in Sub Inc. 102/400 (1 281090 x . 8) 25/600 No mcontrolling Interest I Equity in earning in Sub Inc 126/560 Investment in SubInc 1241560 (164, 000 x18- 4/640) D Investment in Smashing 75, 200 Dividends Declared 75/200 (94, 900 x . 8) E Amortization Expense 5, 800 Building 4800 copyright 41000 U P Liabilities 20, 800 current assets 20800

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!