Question: Problem One - Chapter 7: Part. A: You are the lead auditor for the Bella Luna Tree Company, Inc. in Bethel, CT. The company has

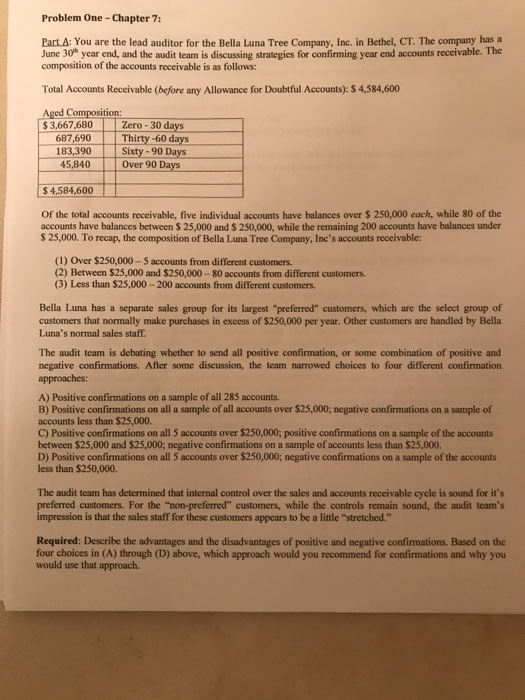

Problem One - Chapter 7: Part. A: You are the lead auditor for the Bella Luna Tree Company, Inc. in Bethel, CT. The company has a June 30" year end, and the audit team is discussing strategies for confirming year end accounts receivable. The composition of the accounts receivable is as follows: Total Accounts Receivable (before any Allowance for Doubtful Accounts): $4,584,600 Aged Composition: $ 3.667.680 Zero - 30 days 687,690 Thirty-60 days 183,390 Sixty - 90 Days 45,840 Over 90 Days $ 4,584,600 of the total accounts receivable, five individual accounts have balances over $ 250,000 each, while 80 of the accounts have balances between $ 25,000 and $ 250,000, while the remaining 200 accounts have balances under $ 25,000. To recap, the composition of Bella Luna Tree Company, Inc's accounts receivable: (1) Over $250,000 -- 5 accounts from different customers. (2) Between $25,000 and $250,000 -80 accounts from different customers. (3) Less than $25,000 - 200 accounts from different customers. Bella Luna has a separate sales group for its largest "preferred" customers, which are the select group of customers that normally make purchases in excess of $250,000 per year. Other customers are handled by Bella Luna's normal sales staff. The audit team is debating whether to send all positive confirmation, or some combination of positive and negative confirmations. After some discussion, the team narrowed choices to four different confirmation approaches: A) Positive confirmations on a sample of all 285 accounts. B) Positive confirmations on all a sample of all accounts over $25,000; negative confirmations on a sample of accounts less than $25,000. C) Positive confirmations on all 5 accounts over $250,000: positive confirmations on a sample of the accounts between $25,000 and $25,000; negative confirmations on a sample of accounts less than $25,000. D) Positive confirmations on all 5 accounts over $250,000; negative confirmations on a sample of the accounts less than $250,000. The audit team has determined that internal control over the sales and accounts receivable cycle is sound for it's preferred customers. For the "non-preferred" customers, while the controls remain sound, the audit team's impression is that the sales staff for these customers appears to be a little "stretched." Required: Describe the advantages and the disadvantages of positive and negative confirmations. Based on the four choices in (A) through (D) above, which approach would you recommend for confirmations and why you would use that approach. Problem One - Chapter 7 (Continued): Part B: You are evaluating the positive confirmations that have been returned. Most have been returned confirming the balances at June 30, however, the following four have been returned with these comments (A) "This amount was paid on June 30th." (B) "We received this shipment on July 2nd." (C) "These goods were returned for credit on June 15th." (D) "The balance does not reflect our sales discount for paying by July 5th." Required: Evaluate each of the four confirmation responses. Which of the following confirmation responses at June 30" would cause an audit team the most concern, and why? Problem Two - Chapter 8: Part A: When performing procedures in a search of unrecorded liabilities, auditors can utilize various sources of evidence/information (e.g., documents, files, management and clerical personnel) Required: List and describe at least five sources of evidence and/or information for the search for unrecorded Tbilities Part B: You are in the last part of audit evidence gathering for the Bosco Corporation with a year-end of June 30, 2019. Bosco's CEO, Rachel Bosco, states that any invoices relating to the June 30, 2019 year end that were received after the year-end voucher register was closed for the June 30, 2019 year were recorded by Bosco's CFO via a year-end adjusting journal for the year under audit. Bosco's internal audit team also tested for unrecorded liabilities after the June 30, 2019 year-end close. Rachel has indicated she will also provide a letter certifying there are no unrecorded liabilities for the June 30, 2019 year-end. vers for profices, to the bele) should peasoning for Required: (a) Should your procedures for unrecorded liabilities be affected by the fact that the client made a journal entry to record June 30, 2019 that were received later? Explain your reasoning for your answer. (b) Should your test for unrecorded liabilities be affected by the fact that a letter is obtained in which responsible management official certifies, to the best of that person's knowledge, all liabilities that have been recorded? Explain your reasoning for your answer. (c) Should your test for unrecorded liabilities be eliminated or reduced because of the internal audit work? Explain your reasoning for your answer. (d) What sources, in addition to the voucher register for the new year end, should you consider for locating possible unrecorded liabilities? for locating Problem Three - Chapter 9: You are the senior auditor with WCSU LLC CPAs and have been assigned to an inventory observation for the Accell Picnic Table Company, Inc., specifically for the Picnic Table inventory, its major product. Accell has two types of picnic tables, each with a different assigned inventory cost and description: (a) wooden picnie tables and (b) metal and composite plastic picnic tables. Accell has a main location in Danbury CT where the picnic table parts are ordered and then the two types of picnic tables are assembled by Accell's assemblers. The assemblers are full-time employees of Accell. Because the picnic tables are assembled continuously throughout the fiscal year, there is normally an inventory of parts on hand throughout the year. Approximately 40% of the total value of the finished picnic tables are located in the Danbury location, as well as the unassembled parts. Because of space limitations, however, the remaining 60% of the finished picnic tables are sent to three warehouses located in Connecticut, New Hampshire and Pennsylvania. Accell staff plans to count inventory at all their locations on the same day at the company's fiscal year end. It appears the shared warehouses all have equal amounts of finished picnic tables. You're concerned there is not enough audit staff at WCSU to cover all the inventory observations at the four different locations. You have been provided with the following information at the audit planning meeting: . A detailed Picnie Table inventory record detailing all picnic tables expected to be at each location on the date of the inventory observation. The client's Picnic Table manual describing the two types of tables, their descriptions and their standard costs. A map of cach location showing the expected area where the inventories are located. Required: (a) What evidence would you expect to find indicating that the observation of Accell's physical count of inventory was well planned and that Accell's staff were properly supervised? (b) What substantive procedures should you find in the audit documentation of Accell management's assertions about existence and completeness of inventory quantities at year end? You may use Appendix 98 of your McGraw Hill textbook for the audit plan's procedures. (c) If WCSU LLC does not have sufficient audit staff to observe inventories at all locations, what strategies could you use to possibly compensate for the shortfall in audit staffing

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts