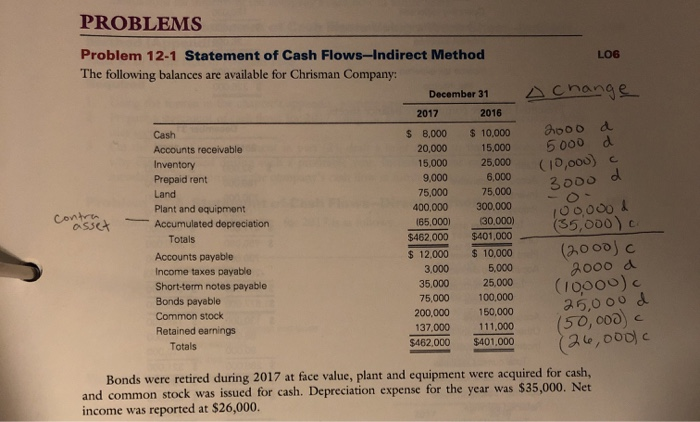

Question: PROBLEMS LOG A change 2000 a 5000 d (10,000) c 3000 d Problem 12-1 Statement of Cash Flows-Indirect Method The following balances are available for

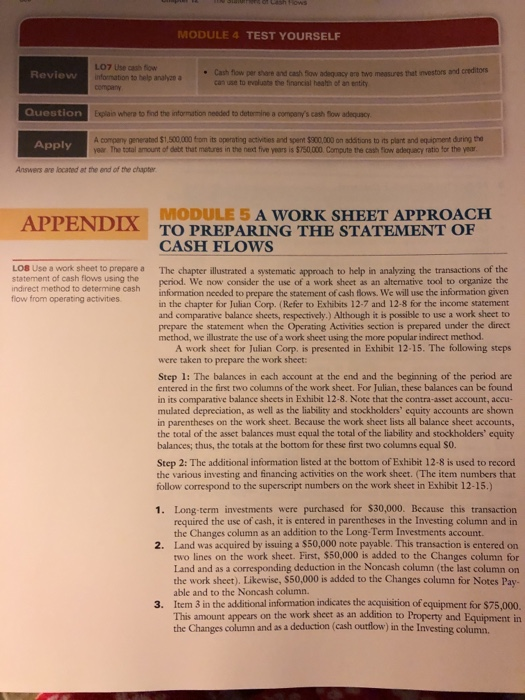

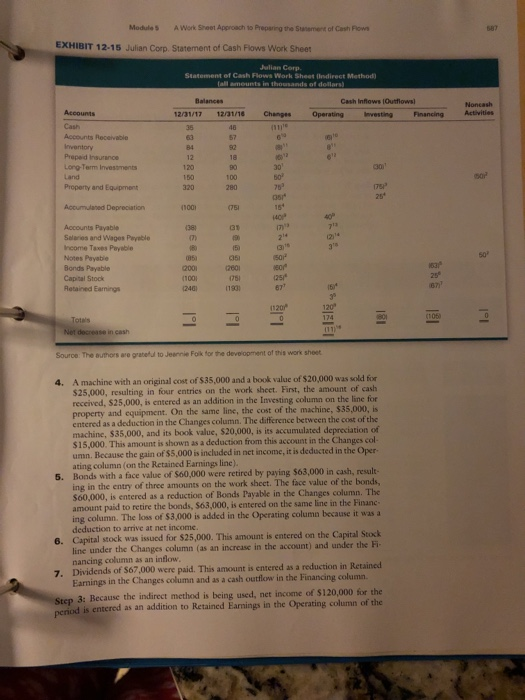

PROBLEMS LOG A change 2000 a 5000 d (10,000) c 3000 d Problem 12-1 Statement of Cash Flows-Indirect Method The following balances are available for Chrisman Company: December 31 2017 2016 Cash $ 8.000 $10,000 Accounts receivable 20,000 15,000 Inventory 15,000 25,000 Prepaid rent 9,000 6,000 Land 75,000 75,000 Plant and equipment 400,000 300,000 Accumulated depreciation 165,000 (30.000) Totals $462,000 $401,000 Accounts payable $ 12,000 $ 10,000 Income taxes payablo 3.000 5,000 Short-term notes payable 35,000 25,000 Bonds payable 75,000 100,000 Common stock 200,000 150.000 Retained earnings 137.000 111,000 Totals $462,000 $401.000 ooooo 1 (35,000) (2000) 2000 a (10ooo). 25,000 d 150,ood). 726,ooolc Bonds were retired during 2017 at face value, plant and equipment were acquired for cash, and common stock was issued for cash. Depreciation expense for the year was $35,000. Net income was reported at $26,000. Refer to all of the facts in Problem 12-1. Required 1. Using the format in the chapter's appendix, prepare a statement of cash flows work sheet. 2. Prepare a statement of cash flows for 2017 using the indirect method in the Operating Activ- ities section. 3. Did Chrisman generate sufficient cash from operations to pay for its investing activities? How did it generate cash other than from operations? Explain your answers. MODULE 4 TEST YOURSELF Review LO7 Use cash flow Information to help analyze a Cash flow per there and cash flow do you two measures that investors and creditors can use to evoluate the financial heat of an entity Question Explain where to find the information needed to determine a company's cash flow adequacy. Apply A comery generated $1.500.000 from its operating activities and spent $900.000 onsdations to its plant and equipment during the Year The total amount of dete that matures in the need five years is $750.000. Compute the cash flow adequacy ratio for the year Answers are located at the end of the chapter APPENDIX MODULE 5 A WORK SHEET APPROACH TO PREPARING THE STATEMENT OF CASH FLOWS LOB Use a worksheet to prepare a statement of cash flows using the indirect method to determine cash flow from operating activities The chapter illustrated a systematic approach to help in analyzing the transactions of the period. We now consider the use of a work sheet as an alternative tool to organize the information needed to prepare the statement of cash flows. We will use the information given in the chapter for Julian Corp. (Refer to Exhibits 12-7 and 12-8 for the income statement and comparative balance sheets, respectively.) Although it is possible to use a work sheet to prepare the statement when the Operating Activities section is prepared under the direct method, we illustrate the use of a work sheet using the more popular indirect method A work sheet for Julian Corp. is presented in Exhibit 12-15. The following steps were taken to prepare the work sheet: Step 1: The balances in each account at the end and the beginning of the period are entered in the first two columns of the work sheet. For Julian, these balances can be found in its comparative balance sheets in Exhibit 12-8. Note that the contra-asset account, accu- mulated depreciation, as well as the liability and stockholders' equity accounts are shown in parentheses on the work shect. Because the work sheet lists all balance sheet accounts, the total of the asset balances must equal the total of the liability and stockholders' equity balances; thus, the totals at the bottom for these first two columns equal SO. Step 2: The additional information listed at the bottom of Exhibit 12-8 is used to record the various investing and financing activities on the work sheet. (The item numbers that follow correspond to the superscript numbers on the work sheet in Exhibit 12-15.) 1. Long-term investments were purchased for $30,000. Because this transaction required the use of cash, it is entered in parentheses in the Investing column and in the Changes column as an addition to the Long-Term Investments account. 2. Land was acquired by issuing a $50,000 note payable. This transaction is entered on two lines on the work sheet. First, $50,000 is added to the Changes column for Land and as a corresponding deduction in the Noncash column (the last column on the work sheet). Likewise, $50,000 is added to the Changes column for Notes Pay able and to the Noncash column. 3. Item 3 in the additional information indicates the acquisition of equipment for $75.00 This amount appears on the work sheet as an addition to Property and Equipment in the Changes column and as a deduction (cash outflow) in the Investing column Modules A Work Shoot Approach to Preparing the Somerol Cash Pows EXHIBIT 12-15 Julian Corp. Statement of Cash Flows Work Sheet Julian Corp Statement of Cash Flows Work Sheet indirect Method) all amounts in thousands of dollars Balances Cash inflows Outflows Operating testing Financing Accounts 12/31/17 12/31/16 Changes Activities Accounts Receivable Inventory Proped insurance Long Term Investments Land Property and Equipment 100 Accumulated Depreciation 1100 15 Accounts Payable Salaries and Wages Payable Income Taxes Payable Notes Payable Bonds Payable Capital Stock Retained Earnings Il 32838 8888 50 (1001 (240) 11901 11201 To's Net decrease in cash 111 Source: The uthors are grateful to Jeanne Fork for the development of this work sheet 4. A machine with an original cost of $35,000 and a book value of $20,000 was sold for $25,000, resulting in four entries on the work sheet. First, the amount of cash received, $25,000, is entered as an addition in the Investing column on the line for property and equipment. On the same line, the cost of the machine, $35,000, is entered as a deduction in the Changes column. The difference between the cost of the machine, $35,000, and its book value, $20,000, is its accumulated depreciation of $15.000. This amount is shown as a deduction from this account in the Changes sol umn. Because the gain of $5,000 is included in net income, it is deducted in the Oper ating column on the Retained Earnings line). 5. Bonds with a face value of $60,000 were retired by paying $63,000 in cash, result- ing in the entry of three amounts on the work sheet. The face value of the bonds $60,000, is entered as a reduction of Bonds Payable in the Changes column. The amount paid to retire the bonds, 563,000, is entered on the same line in the Financ- ing column. The loss of $3,000 is added in the Operating column because it was a deduction to arrive at net income. 6. Capital stock was issued for $25,000. This amount is entered on the Capital Stock line under the Changes column (as an increase in the account and under the Fi- mancing column as an intlow. 7 Dividends of $67,000 were paid. This amount is entered as a reduction in Retained Famings in the Changes column and as a cash outflow in the Financing column Step 3: Because the indirect method is being used, net income of $120,000 for the period is entered as an addition to Retained Earnings in the Operating column of the

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts