Question: Product Innovation and Management Home Task # 1 (Case Study # 1) Fall 2020-2021 Section: A Marks: 15 The Story of bKash bKash Limited (bKash)

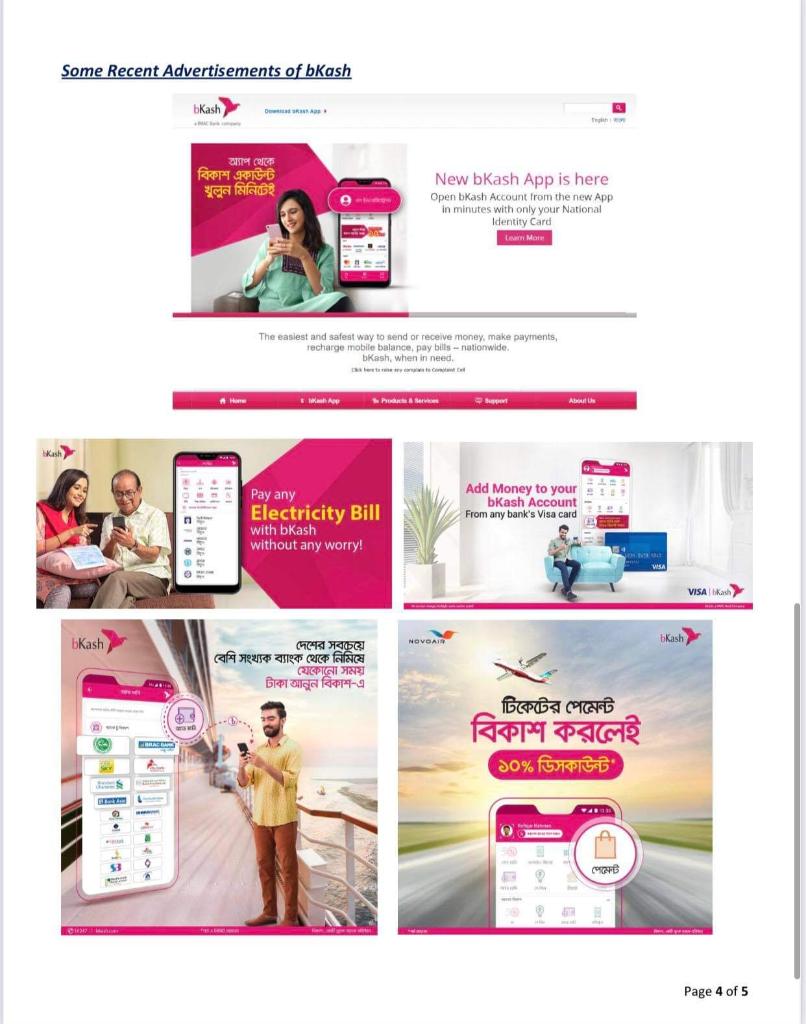

Product Innovation and Management Home Task \# 1 (Case Study \# 1) Fall 2020-2021 Section: A Marks: 15 The Story of bKash bKash Limited (bKash) is a Bank-led Mobile Financial Service (MFS) Provider in Bangladesh operating under the license and approval of the Bangladesh Bank, as a subsidiary of BRAC Bank Limited. bKash provides safe, convenient and easy ways to make payments and money transfer a BRAC Bank company services via mobile phones to both the unbanked and the banked people of Bangladesh. At present, bKash is one of the leading Mobile Financial Services Providers in the world. bKash started as a joint venture between BRAC Bank Limited, Bangladesh and Money in Motion LLC, USA in 2010. In April 2013, International Finance Corporation (IFC), a member of the World Bank Group, became an equity partner and in March 2014, Bill \& Melinda Gates Foundation became the investor of the company. In April 2018, Ant Financial (Ali Pay), an affiliate of globally reputed Alibaba Group, became an investor in bKash. The ultimate objective of bKash is to ensure access to a broader range of financial services for the people of Bangladesh. It has a special focus to serve the low-income masses of the country to achieve broader financial inclusion by providing services that are convenient, affordable and reliable. More than 70% of the population of Bangladesh lives in rural areas where access to formal financial services is difficult. Yet these are the people who are in most need of such services, either for receiving funds from loved ones in distant locations or to access financial tools to improve their economic condition. Less than 15% of Bangladeshis are connected to the formal banking system whereas over 68% have mobile phones. These phones are not merely devices for talking but can be used for more useful and sophisticated processing tasks. bKash was conceived primarily to utilize these mobile devices and the universal telecom networks to extend financial services in a secure manner to the under-served remote population of Bangladesh. bKash can be accessed via all the mobile networks operating in Bangladesh. Currently, bKash is running a network of more than 180,000 agents throughout urban and rural areas of Bangladesh with over 30 million registered accounts. In 2017, bKash was ranked as the 23rd company in the annual list of Fortune Magazine's 'Change the World in 2017' among the top 50 companies to make changes based on social issues. Through partnerships with all major mobile operators of Bangladesh, bKash's technology allows 98% of the country's mobile users to access its service via very basic handsets. Bangladesh, home to more than 165 million people, represents a unique opportunity for a mobile money platform: universal wireless network coverage, widespread personal ownership of mobile phones, a cash economy, poor physical infrastructure, and a favorable regulatory environment for a bank-led initiative. bKash presents a compelling business plan and social uplifting agenda which capitalizes on these factors to dramatically expand access to formal financial services for the people of Bangladesh, less than 10% of them so far have encountered any formal banking facility. Reasons for the poor penetration of the banking sector are partly due to Bangladesh's weak infrastructure, conventional banking practice of not catering the poor, and lack of technology that could reach the poor. While these factors have created a fertile environment for microfinance, they have left little incentive for formal banks to venture out of the large cities. As such, poor and rural populations rarely encounter the formal banking sector. A bKash mobile wallet is customer's financial account, into which money can be deposited and out of which money can be withdrawn or used for various services. Customers can receive electronic money into their bKash accounts through salary, loan, domestic remittance, and other disbursements and eventually cash-out the electronic money at any of bKash's vast of agent network of 90 thousand retail points. One of the reasons for bKash's success is its focus on serving the poor. It was important to come up with a simple interface that can be accessed by the cheapest (i.e. $15 ) handset. Smartphones would make it easy to implement mobile money, but the service would then be limited to only affluent customers and would defeat the purpose of reaching the Page 1 of 5 unbanked and poor. bKash opted for USSD (Unstructured Supplementary Service Data) that allowed anybody to access bKash platform by dialing an access code, regardless of the sophistication of the handset. bKash's focus on reaching the poor distinguishes it from services that have fees for cash-in or minimum cash-out fee. bKash was conceived primarily to utilize these devices and telecom networks to extend financial services securely to the remote general masses of Bangladesh. bKash, as a mobile financial service provider promises its users five core benefits which are fast, affordable, secure, convenient, and nationwide. These benefits are described in a brief below: Fast bKash promises its consumers to be the fastest transaction process. One can send and receive the money within minutes through bKash. Affordable The sending and receiving money through bKash is very low in the cost comparing with global standards. It has been a great advantage for the general people of the country. Secure Each transaction of bKash is based on a PIN or personal identification number which is very secure. Moreover, the bKash account will be fully secure even if one lost his or her mobile. So bKash is promising the best security in the transaction of money. Convenient bKash is highly convenient for its users. People can send and receive money anywhere and anytime. bKash is serving its consumers 24 hours a day and 7 days a week. Nationwide bKash has more than 160,000 agents nationwide and more than 300 ATMs. So, the availability of the service is very high nationwide. Products and Services bKash is offering various mobile financial services to its consumers which is quick, affordable, convenient, and safe. A list of product and services offered by bKash Limited are as follows: Cash-in bKash account holders can deposit money into their bKash account through the Cash-out Consumers can withdraw money anytime from their bKash account from bKash agent points. Send Money Through bKash money can be transferred from one account to another which is cost-effective and comfortable. Payment bKash users can make payment to the merchant who accepts bKash payment. Buy airtime Users of Grameenphone, Robi, Airtel, Banglalink, and Teletalk mobile operators can recharge their mobile balance through bKash. Remittances People can receive money in their bKash account from their family members who are living in foreign countries. Pay Bill A recent inclusion of bKash is service paying Electricity bill, Gas bill, Water bill, Credit Card bills, and many more. Add Money People can add money to bKash through the bKash app from Bank account or Debit/Credit Cards. Users can easily add money to their bKash account through the application of 'Bank to bKash' or 'Card to bKash' Account. When using the 'Card to bKash' Account interface, users having any partnered bank's Mastercard or VISA card can add money to their bKash Account. When using the 'Bank to bKash' Account option, users will be having the options of adding money through the 'Bank Account' or 'Internet Banking' applications. Recently, the 'Internet Banking' application has been updated, where the account holders of 20 Banks are allowed to add money to their bKash account giving more options for the users to avail the services of the mobile financial services. Page 2 of 5 Some Recent Advertisements of bKash New bKash App is Open bKash Account from the in minutes with only your N Identity Card Inaini Mati The easiest and safeat way to aend or receive money, make payments, recharge mobile balance, pay bills - nationwide. bKash, when in need. 1. Discuss the different types of Uncertainties (Market Uncertainty, Technological Uncertainty, and Organizational Uncertainty) that "bKash" have encountered in their business operations (from its inception till now) in the local market. Discuss with some real or hypothetical reasons to explain the three types of Uncertainties from the organization's perspective. (6 Marks) 2. Explain what type/s of Innovation that bKash have initiated when it first started to operate in the local market and continuing till now. Briefly describe the specific type/s with appropriate reasoning. (Refer to Slides from 21 to 26 - Chapter \# 1) (3 Marks) 3. When companies are having the "New-Product Planning" strategies, they consider three categories of Innovations namely Continuous Innovations, Dynamically Continuous Innovations, and Discontinuous Innovations. Discuss all the three categories with appropriate reasoning how "bKash" have applied these innovations in their operations from the beginning till now. (Refer to Slides from 14 to 19 Chapter \# 2) (6 Marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts