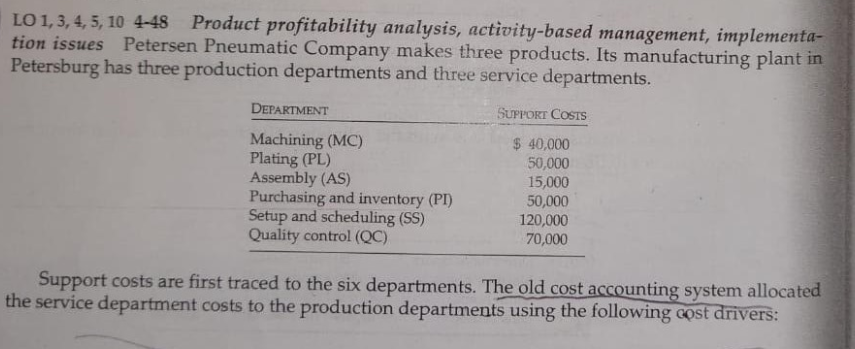

Question: Product profitability analysis, activity-based management, implementa- LO 1, 3, 4, 5, 10 4-48 tion issues Petersen Pneumatic Company makes three products. Its manufacturing plant in

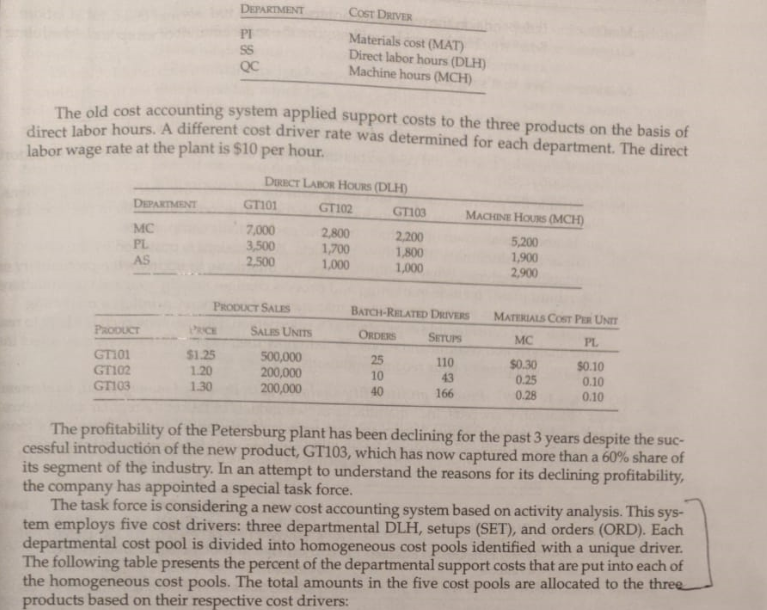

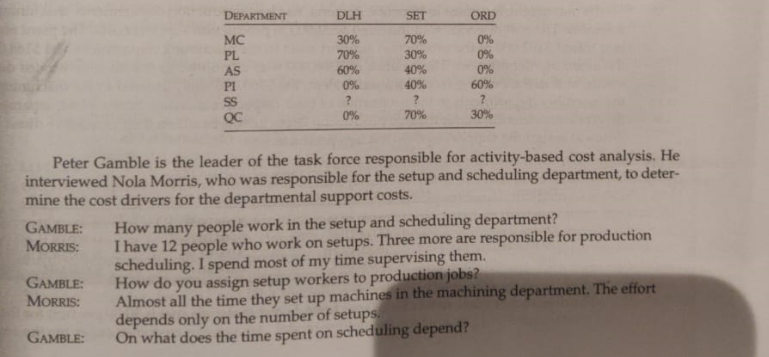

Product profitability analysis, activity-based management, implementa- LO 1, 3, 4, 5, 10 4-48 tion issues Petersen Pneumatic Company makes three products. Its manufacturing plant in Petersburg has three production departments and three service departments. DEPARTMENT SUPPORT COSTS Machining (MC) Plating (PL) Assembly (AS) Purchasing and inventory (PI) Setup and scheduling (SS) Quality control (QC) 40,000 50,000 15,000 50,000 120,000 70,000 Support costs are first traced to the six departments. The old cost accounting system allocated the service department costs to the production departments using the following cost drivers: DEPARTMENT COST DRIVER Materials cost (MAT) Direct labor hours (DLH) Machine hours (MCH) PI QC The old cost accounting system applied support costs to the three products on the basis of diroct labor hours. A different cost driver rate was determined for each department. The direct labor wage rate at the plant is $10 per hour DRECT LABOR HOURS (DLH) DEPARTMENT GT101 GT102 GT103 MACHINE HOURS (MCH) 7,000 3,500 2,500 MC 2,800 1,700 1,000 2,200 1,800 5,200 1,900 2,900 PL AS 1,000 PRODUCT SALES BATCH-RELATED DRIVERS MATERIALS COST PER UNIT PRODUCT SALES UNITS PRICE ORDERS SETUPS MC PL 500,000 200,000 200,000 GT101 $1.25 1.20 1.30 25 110 $0.30 50.10 GT102 10 43 0.25 0.10 GT103 40 166 0.28 0.10 The profitability of the Petersburg plant has been declining for the past 3 years despite the suc- cessful introductin of the new product, GT103, which has now captured more than a 60% share of its segment of the industry. In an attempt to understand the reasons for its declining profitability the company has appointed a special task force. The task force is considering a new cost accounting system based on activity analysis. This sys- tem employs five cost drivers: three departmental DLH, setups (SET), and orders (ORD). Each departmental cost pool is divided into homogeneous cost pools identified with a unique driver. The following table presents the percent of the departmental support costs that are put into each of the homogeneous cost pools. The total amounts in the five cost pools are allocated to the three products based on their respective cost drivers: DEPARTMENT DLH SET ORD 30% 0% 0% MC 70% 70% 60% 0% 30% PL 40% 0% AS PI 60% 40% 7 30% 70% 0% QC Peter Gamble is the leader of the task force responsible for activity-based cost analysis. He interviewed Nola Morris, who was responsible for the setup and scheduling department, to deter- mine the cost drivers for the departmental support costs. How many people work in the setup and scheduling department? I have 12 people who work on setups. Three more are responsible for production scheduling. I spend most of my time supervising them. How do you assign setup workers to production jobs? Almost all the time they set up machines in the machining department. The effort depends only On what does the time spent on scheduling depend? GAMBLE: MORRIS: GAMBLE: MORRIS: on the number of setups GAMBLE MORRIS GAMBLE: It depends on the number of orders So a large batch or order will require the same amount of setup and scheduling time as a small batch or order Yes, that's right MORRIS: Required (a) List the reasons that the old cost accounting system at Petersen Pneumatic may be distorting its product costs (b) Determine the product cost per unit using both the old and new cost accounting systems. Show all the intermediate steps including the cost driver rates, amounts in the three new cost pools, and a breakdown of product costs into each of their components. le Analyze the profitability of the three products. What insight is provided by the new profitability analysis? What should Petersen Pneumatic do to improve the profitability of its Petersburg plant? Include marketing and process changes among your recommendations. (d) Mike Meservy is a veteran production manager, and Shannon Corinth is a marketing manager with considerable experience as a salesperson. Discuss how each is likely to react to your analis and recommendations. Explain how their expected reactions may affect the way you will present your recommendations Product profitability analysis, activity-based management, implementa- LO 1, 3, 4, 5, 10 4-48 tion issues Petersen Pneumatic Company makes three products. Its manufacturing plant in Petersburg has three production departments and three service departments. DEPARTMENT SUPPORT COSTS Machining (MC) Plating (PL) Assembly (AS) Purchasing and inventory (PI) Setup and scheduling (SS) Quality control (QC) 40,000 50,000 15,000 50,000 120,000 70,000 Support costs are first traced to the six departments. The old cost accounting system allocated the service department costs to the production departments using the following cost drivers: DEPARTMENT COST DRIVER Materials cost (MAT) Direct labor hours (DLH) Machine hours (MCH) PI QC The old cost accounting system applied support costs to the three products on the basis of diroct labor hours. A different cost driver rate was determined for each department. The direct labor wage rate at the plant is $10 per hour DRECT LABOR HOURS (DLH) DEPARTMENT GT101 GT102 GT103 MACHINE HOURS (MCH) 7,000 3,500 2,500 MC 2,800 1,700 1,000 2,200 1,800 5,200 1,900 2,900 PL AS 1,000 PRODUCT SALES BATCH-RELATED DRIVERS MATERIALS COST PER UNIT PRODUCT SALES UNITS PRICE ORDERS SETUPS MC PL 500,000 200,000 200,000 GT101 $1.25 1.20 1.30 25 110 $0.30 50.10 GT102 10 43 0.25 0.10 GT103 40 166 0.28 0.10 The profitability of the Petersburg plant has been declining for the past 3 years despite the suc- cessful introductin of the new product, GT103, which has now captured more than a 60% share of its segment of the industry. In an attempt to understand the reasons for its declining profitability the company has appointed a special task force. The task force is considering a new cost accounting system based on activity analysis. This sys- tem employs five cost drivers: three departmental DLH, setups (SET), and orders (ORD). Each departmental cost pool is divided into homogeneous cost pools identified with a unique driver. The following table presents the percent of the departmental support costs that are put into each of the homogeneous cost pools. The total amounts in the five cost pools are allocated to the three products based on their respective cost drivers: DEPARTMENT DLH SET ORD 30% 0% 0% MC 70% 70% 60% 0% 30% PL 40% 0% AS PI 60% 40% 7 30% 70% 0% QC Peter Gamble is the leader of the task force responsible for activity-based cost analysis. He interviewed Nola Morris, who was responsible for the setup and scheduling department, to deter- mine the cost drivers for the departmental support costs. How many people work in the setup and scheduling department? I have 12 people who work on setups. Three more are responsible for production scheduling. I spend most of my time supervising them. How do you assign setup workers to production jobs? Almost all the time they set up machines in the machining department. The effort depends only On what does the time spent on scheduling depend? GAMBLE: MORRIS: GAMBLE: MORRIS: on the number of setups GAMBLE MORRIS GAMBLE: It depends on the number of orders So a large batch or order will require the same amount of setup and scheduling time as a small batch or order Yes, that's right MORRIS: Required (a) List the reasons that the old cost accounting system at Petersen Pneumatic may be distorting its product costs (b) Determine the product cost per unit using both the old and new cost accounting systems. Show all the intermediate steps including the cost driver rates, amounts in the three new cost pools, and a breakdown of product costs into each of their components. le Analyze the profitability of the three products. What insight is provided by the new profitability analysis? What should Petersen Pneumatic do to improve the profitability of its Petersburg plant? Include marketing and process changes among your recommendations. (d) Mike Meservy is a veteran production manager, and Shannon Corinth is a marketing manager with considerable experience as a salesperson. Discuss how each is likely to react to your analis and recommendations. Explain how their expected reactions may affect the way you will present your recommendations

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts