Question: Projected Balance Sheet Assets Liabilities Consumer loans - 10% floating rate 375 Demand deposits 2% floating 289 rate Corporate loans -14% floating rate Term deposits

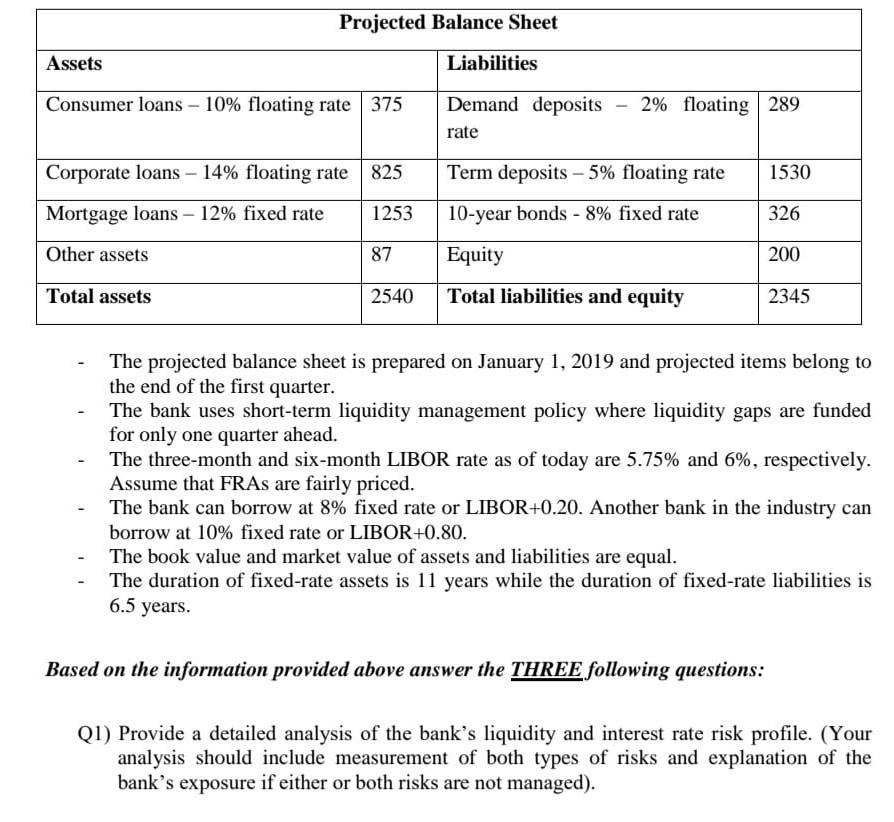

Projected Balance Sheet Assets Liabilities Consumer loans - 10% floating rate 375 Demand deposits 2% floating 289 rate Corporate loans -14% floating rate Term deposits - 5% floating rate 1530 Mortgage loans - 12% fixed rate 1253 10-year bonds - 8% fixed rate 326 Other assets 87 Equity 200 Total assets 2540 Total liabilities and equity 2345 The projected balance sheet is prepared on January 1, 2019 and projected items belong to the end of the first quarter. The bank uses short-term liquidity management policy where liquidity gaps are funded for only one quarter ahead. The three-month and six-month LIBOR rate as of today are 5.75% and 6%, respectively. Assume that FRAs are fairly priced. The bank can borrow at 8% fixed rate or LIBOR+0.20. Another bank in the industry can borrow at 10% fixed rate or LIBOR+0.80. The book value and market value of assets and liabilities are equal. The duration of fixed-rate assets is 11 years while the duration of fixed-rate liabilities is 6.5 years. Based on the information provided above answer the THREE following questions: Q1) Provide a detailed analysis of the bank's liquidity and interest rate risk profile. (Your analysis should include measurement of both types of risks and explanation of the bank's exposure if either or both risks are not managed). Projected Balance Sheet Assets Liabilities Consumer loans - 10% floating rate 375 Demand deposits 2% floating 289 rate Corporate loans -14% floating rate Term deposits - 5% floating rate 1530 Mortgage loans - 12% fixed rate 1253 10-year bonds - 8% fixed rate 326 Other assets 87 Equity 200 Total assets 2540 Total liabilities and equity 2345 The projected balance sheet is prepared on January 1, 2019 and projected items belong to the end of the first quarter. The bank uses short-term liquidity management policy where liquidity gaps are funded for only one quarter ahead. The three-month and six-month LIBOR rate as of today are 5.75% and 6%, respectively. Assume that FRAs are fairly priced. The bank can borrow at 8% fixed rate or LIBOR+0.20. Another bank in the industry can borrow at 10% fixed rate or LIBOR+0.80. The book value and market value of assets and liabilities are equal. The duration of fixed-rate assets is 11 years while the duration of fixed-rate liabilities is 6.5 years. Based on the information provided above answer the THREE following questions: Q1) Provide a detailed analysis of the bank's liquidity and interest rate risk profile. (Your analysis should include measurement of both types of risks and explanation of the bank's exposure if either or both risks are not managed)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts