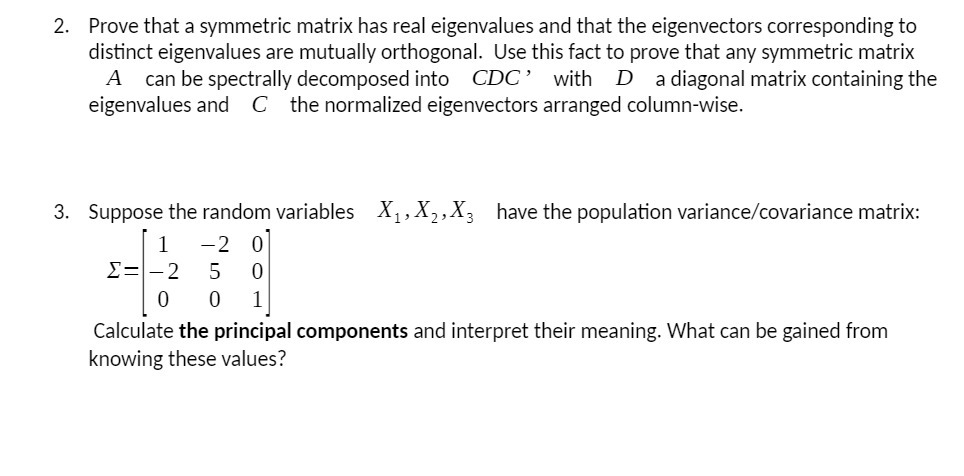

Question: Prove that a symmetric matrix has real eigenvalues and that the eigenvectors corresponding to distinct eigenvalues are mutually orthogonal. Use this fact to prove that

Prove that a symmetric matrix has real eigenvalues and that the eigenvectors corresponding to distinct eigenvalues are mutually orthogonal. Use this fact to prove that any symmetric matrix A can be spectrally decomposed into CDC ' with D a diagonal matrix containing the eigenvalues and C the normalized eigenvectors arranged column-wise. Suppose the random variables X1 .-. X2 ,X3 have the population variance/covariance matrix: 1 2 O E: 2 5 O 0 0 1 Calculate the principal components and interpret their meaning. What can be gained from knowing these values

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock