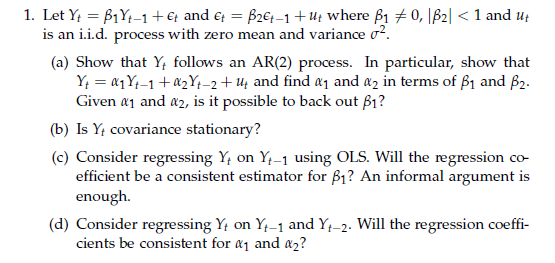

Question: Prove that Y t is an AR(2) model. Hello, how can I solve this exercise? An explanation would be appreciated 1 . Let Y _

Prove that Yt is an AR(2) model.

Hello, how can I solve this exercise? An explanation would be appreciated

1 . Let Y _ BILL_It Er and E = PIE _ 1 + #` where By FO, |BZ| _ I and W` is an lid. process with zero mean and variance IT _ ( a ) Show that " follows an ARIZ) process . In particular, show that " = MY` _ I t MY` _ _ + `` and find a; and a2 in terms of By and Biz . Given ly and Iz , is it possible to back out By ?" (6 ) Is " covariance stationary ?" ( C ) Consider regressing " on*! _ _ using ULIS. Will the regression CO- Efficient be a consistent estimator for By ? An informal argument is Enough. ( I ) Consider regressing ! ! on*! _, and I _1. Will the regression coeHi- cients be consistent for My and my ?"

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts