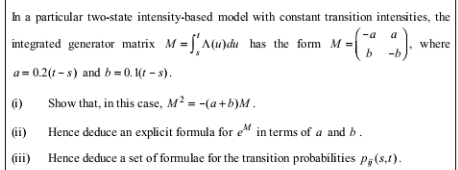

Question: Provide clearly explained answers. In a particular two-state intensity-based model with constant transition intensities, the integrated generator matrix M =|A(u)du has the form M =

Provide clearly explained answers.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock