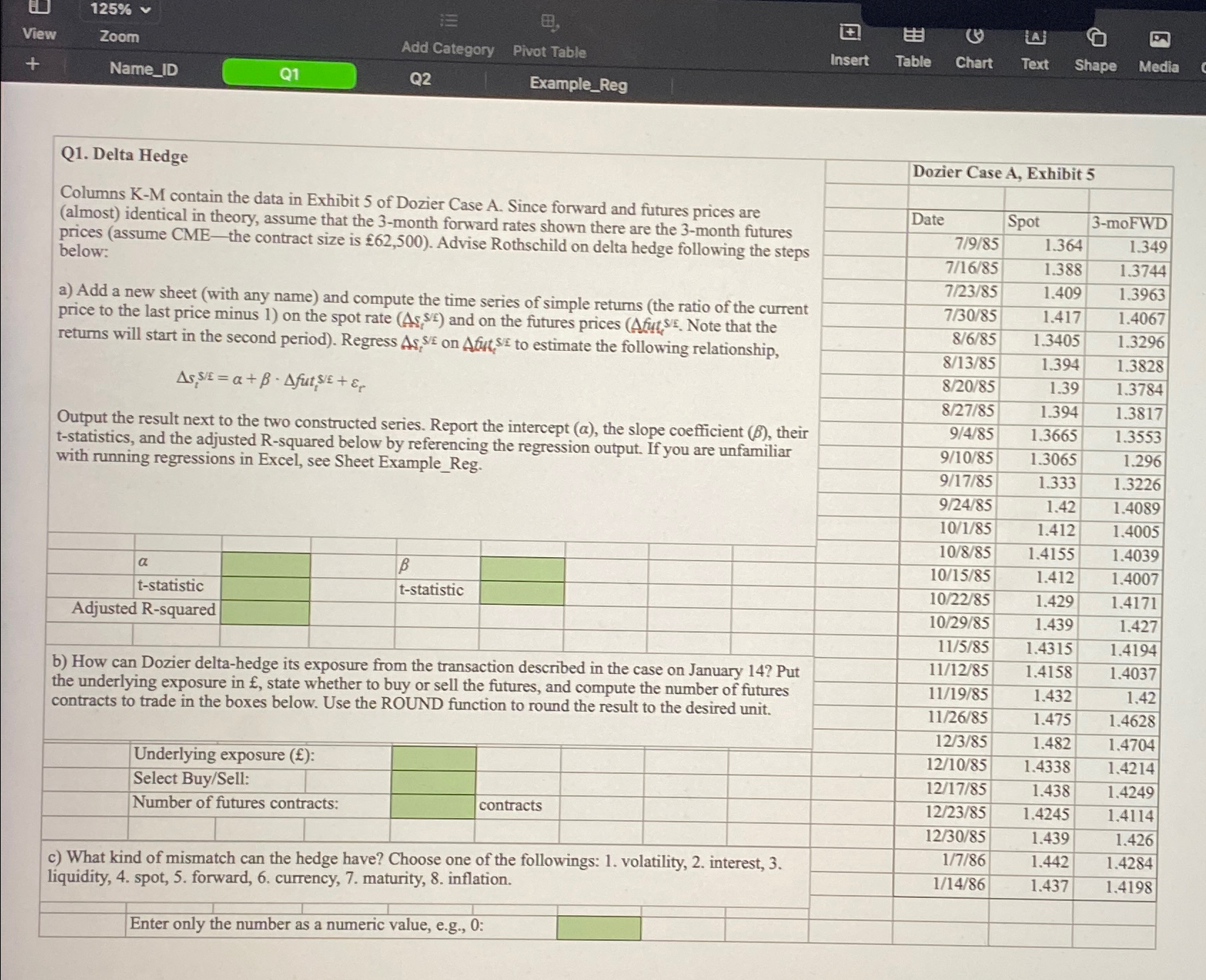

Question: Q 1 . Delta Hedge Columns K - M contain the data in Exhibit 5 of Dozier Case A . Since forward and futures prices

Q Delta Hedge

Columns KM contain the data in Exhibit of Dozier Case A Since forward and futures prices are almost identical in theory, assume that the month forward rates shown there are the month futures prices assume CMEthe contract size is Advise Rothschild on delta hedge following the steps below:

a Add a new sheet with any name and compute the time series of simple returns the ratio of the current price to the last price minus on the spot rate and on the futures prices Note that the returms will start in the second period Regress on A fut to estimate the following relationship,

Output the result next to the two constructed series. Report the intercept the slope coefficient their statistics, and the adjusted squared below by referencing the regression output. If you are unfamiliar with running regressions in Excel, see Sheet ExampleReg.

tabletstatistic,,,tstatistic,,,Adjusted Rsquared,,,,,,

b How can Dozier deltahedge its exposure from the transaction described in the case on January Put the underlying exposure in state whether to buy or sell the futures, and compute the number of futures contracts to trade in the boxes below. Use the ROUND function to round the result to the desired unit.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock