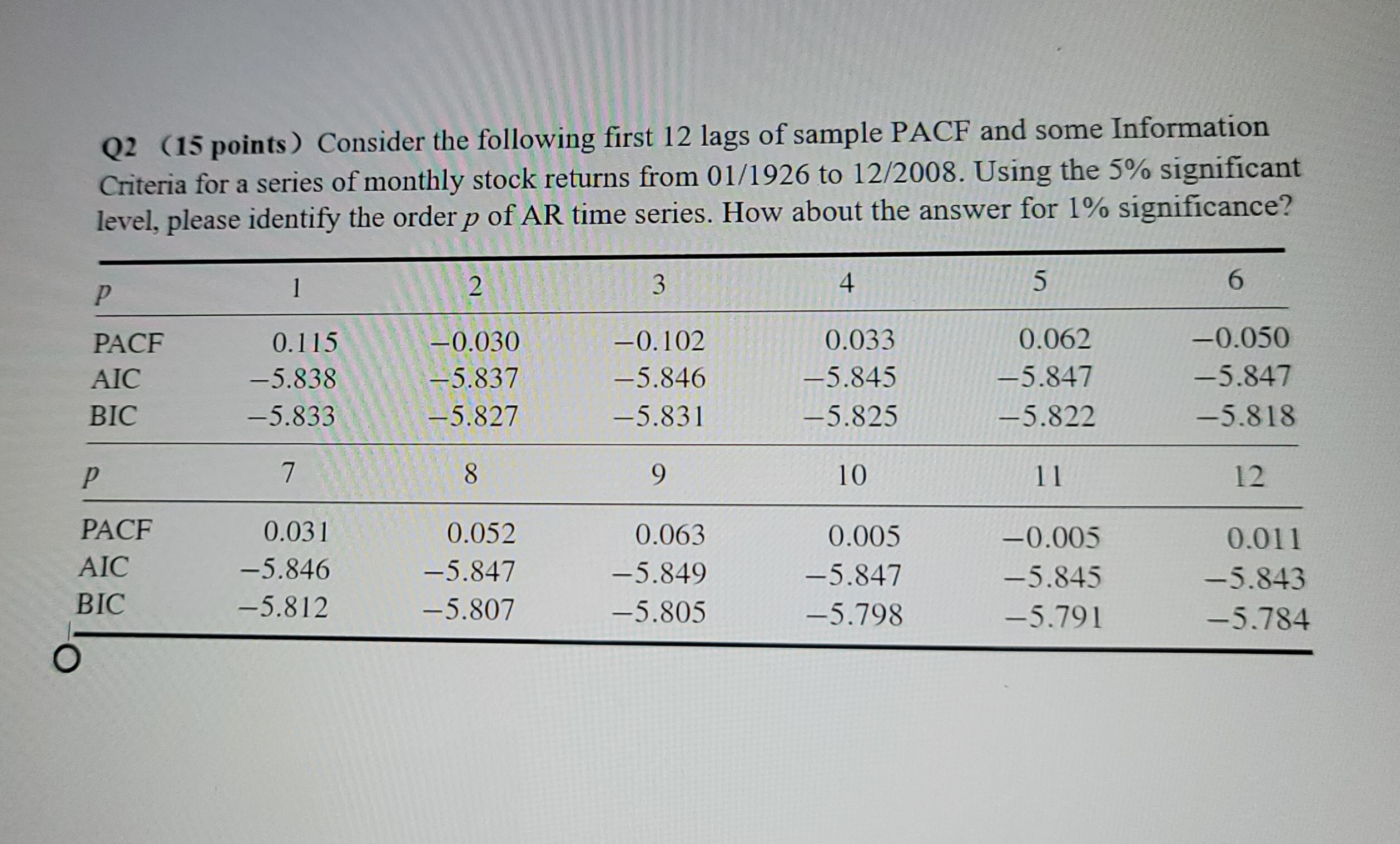

Question: Q 2 ( 1 5 points ) Consider the following first 1 2 lags of sample PACF and some Information Criteria for a series of

Q points Consider the following first lags of sample PACF and some Information Criteria for a series of monthly stock returns from to Using the significant level, please identify the order of AR time series. How about the answer for significance?

tablepPACFAICBICpPACFAICBIC

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock