Question: Q. 2 (10 points) Consider a two date environment, t=0 and t=1. At t=1, there are three possible outcomes, B,M, and G. There are three

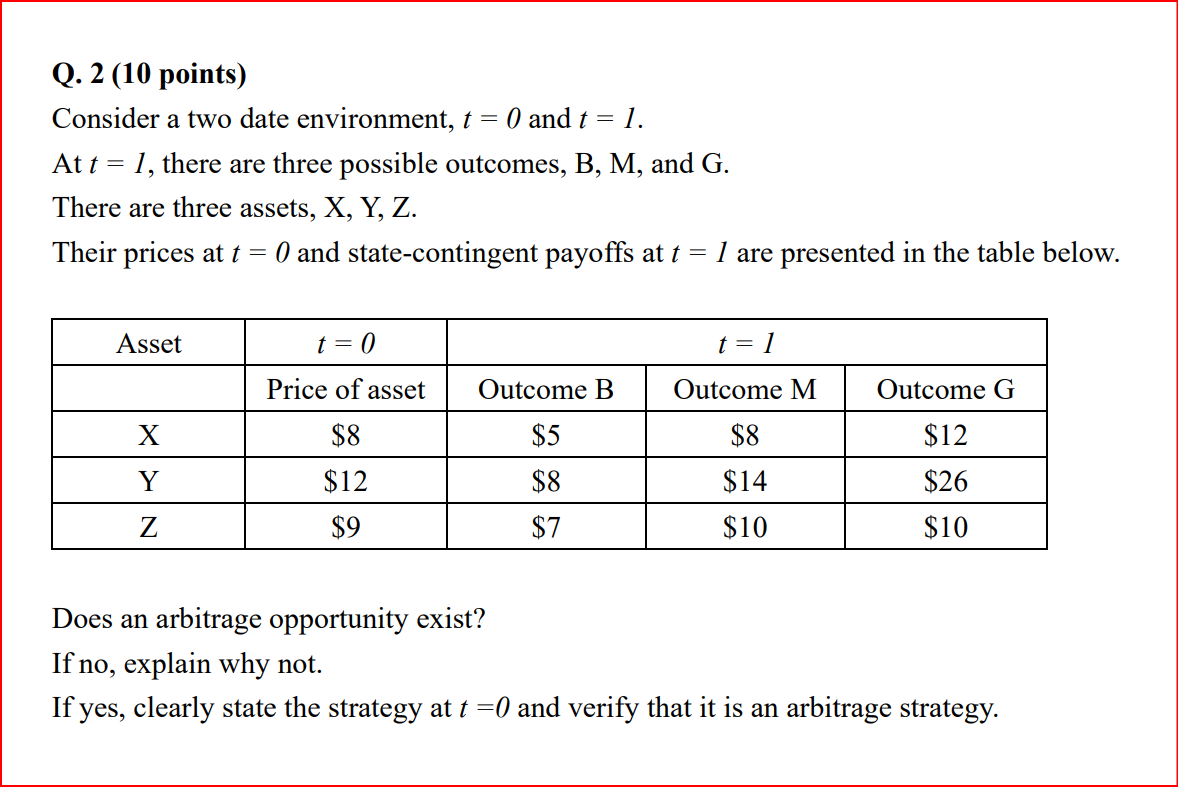

Q. 2 (10 points) Consider a two date environment, t=0 and t=1. At t=1, there are three possible outcomes, B,M, and G. There are three assets, X,Y,Z. Their prices at t=0 and state-contingent payoffs at t=1 are presented in the table below. Does an arbitrage opportunity exist? If no, explain why not. If yes, clearly state the strategy at t=0 and verify that it is an arbitrage strategy

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock