Question: Q. 2 (Another tetranomial model, 25 pts). Consider a one-period tetranomial model on a probability space 2 = {w?,w?,w, we} with two stocks given by

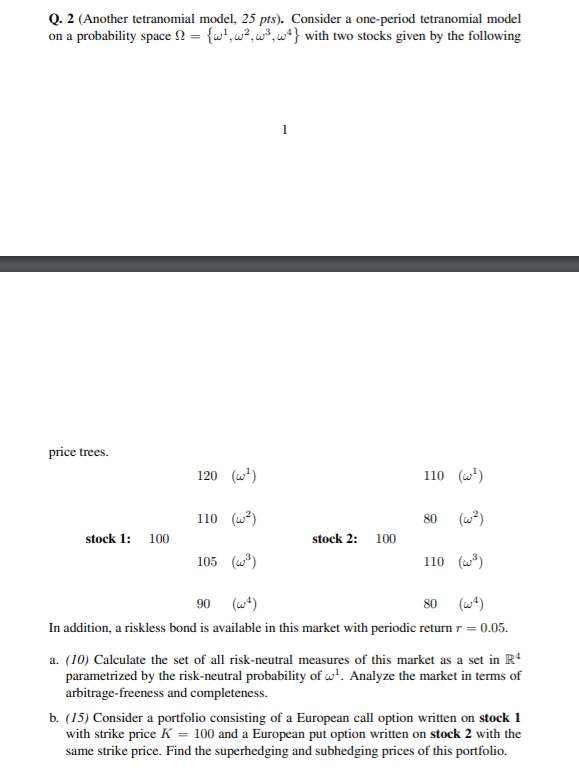

Q. 2 (Another tetranomial model, 25 pts). Consider a one-period tetranomial model on a probability space 2 = {w?,w?,w, we} with two stocks given by the following 1 price trees. 120 (w) 110 w) 110 (2) 80 stock 1: 100 stock 2: 100 105 110 (w) (w) 90 (w) 80 In addition, a riskless bond is available in this market with periodic return r = 0.05. a. (10) Calculate the set of all risk-neutral measures of this market as a set in R4 parametrized by the risk-neutral probability of w?. Analyze the market in terms of arbitrage-freeness and completeness. b. (15) Consider a portfolio consisting of a European call option written on stock 1 with strike price K = 100 and a European put option written on stock 2 with the same strike price. Find the superhedging and subhedging prices of this portfolio. Q. 2 (Another tetranomial model, 25 pts). Consider a one-period tetranomial model on a probability space 2 = {w?,w?,w, we} with two stocks given by the following 1 price trees. 120 (w) 110 w) 110 (2) 80 stock 1: 100 stock 2: 100 105 110 (w) (w) 90 (w) 80 In addition, a riskless bond is available in this market with periodic return r = 0.05. a. (10) Calculate the set of all risk-neutral measures of this market as a set in R4 parametrized by the risk-neutral probability of w?. Analyze the market in terms of arbitrage-freeness and completeness. b. (15) Consider a portfolio consisting of a European call option written on stock 1 with strike price K = 100 and a European put option written on stock 2 with the same strike price. Find the superhedging and subhedging prices of this portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts