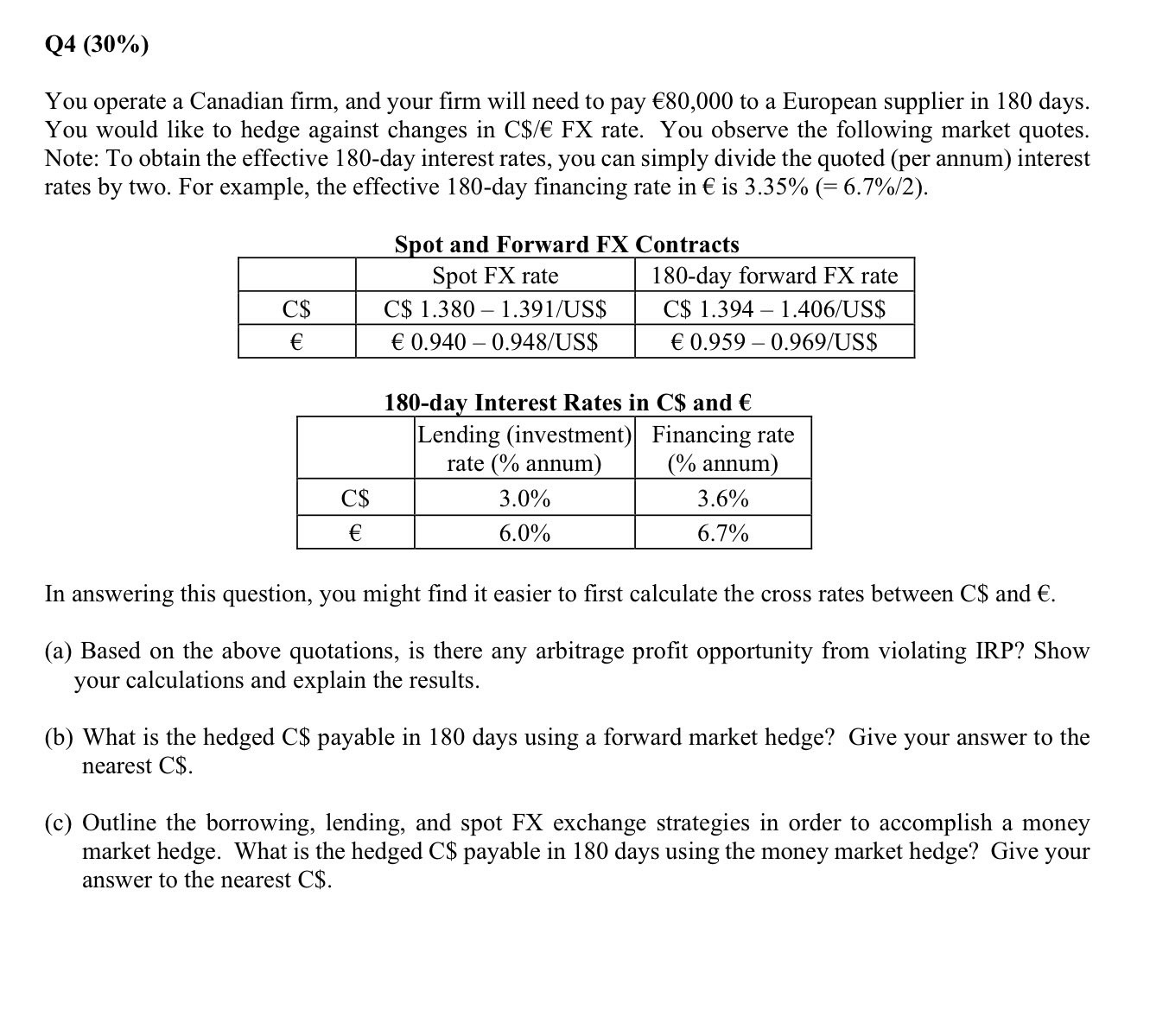

Question: Q 4 ( 3 0 % ) You operate a Canadian firm, and your firm will need to pay 8 0 , 0 0 0

Q

You operate a Canadian firm, and your firm will need to pay to a European supplier in days.

You would like to hedge against changes in rate. You observe the following market quotes.

Note: To obtain the effective day interest rates, you can simply divide the quoted per annum interest

rates by two. For example, the effective day financing rate in is

Spot and Forward FX Contracts

day Interest Rates in $ and

In answering this question, you might find it easier to first calculate the cross rates between $ and

a Based on the above quotations, is there any arbitrage profit opportunity from violating IRP? Show

your calculations and explain the results.

b What is the hedged $ payable in days using a forward market hedge? Give your answer to the

nearest $

c Outline the borrowing, lending, and spot FX exchange strategies in order to accomplish a money

market hedge. What is the hedged C $ payable in days using the money market hedge? Give your

answer to the nearest $

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock