Question: Q 5 A and B are two 2 0 - year bonds. A has a coupon of 4 % and B has a coupon of

Q A and B are two year bonds. A has a coupon of and has a coupon of Assuming that both are trading at the same yield, what can be said about the duration of these bonds?

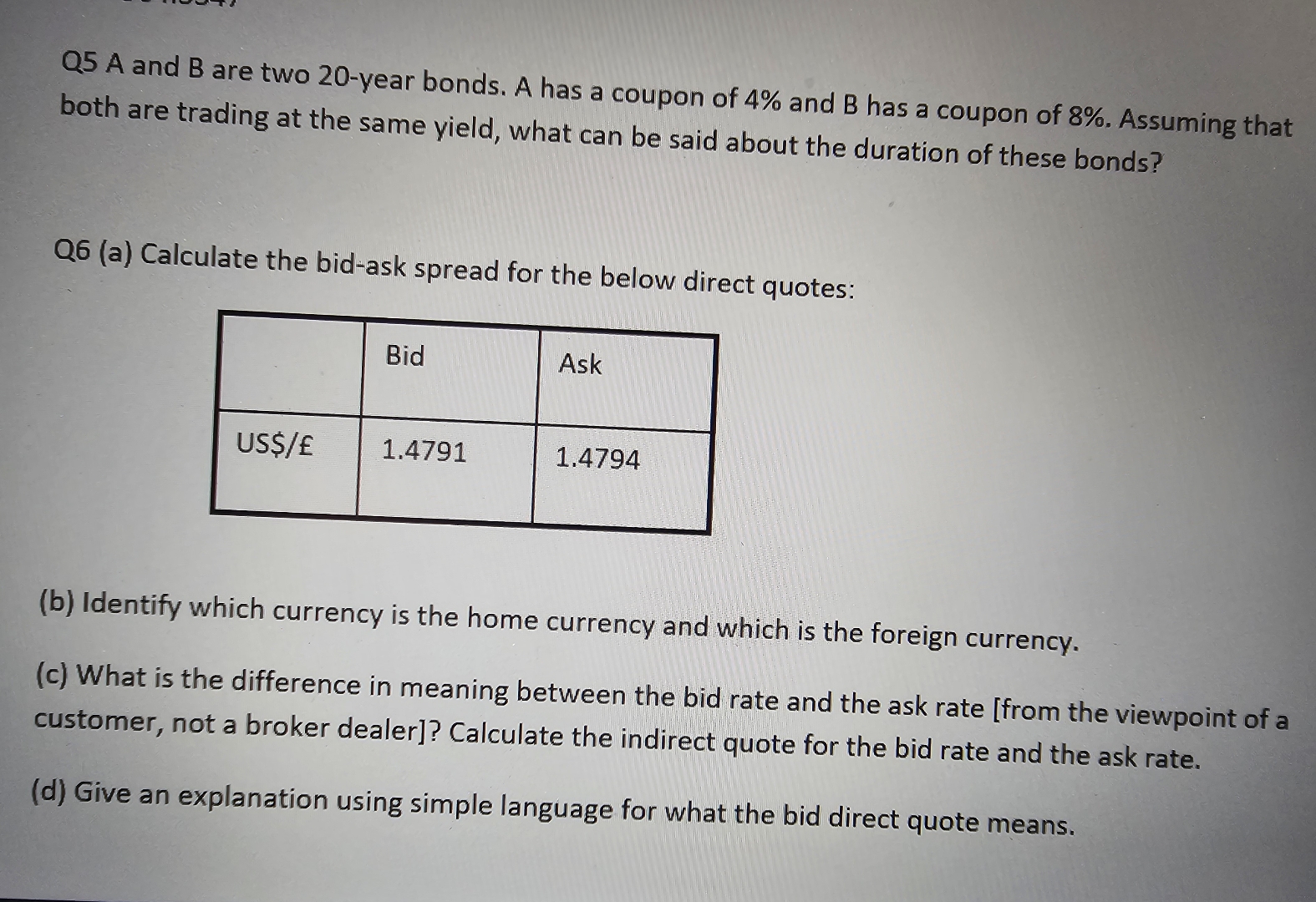

Qa Calculate the bidask spread for the below direct quotes:

tableBid,AskUS$

b Identify which currency is the home currency and which is the foreign currency.

c What is the difference in meaning between the bid rate and the ask rate from the viewpoint of a customer, not a broker dealer Calculate the indirect quote for the bid rate and the ask rate.

d Give an explanation using simple language for what the bid direct quote means.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock