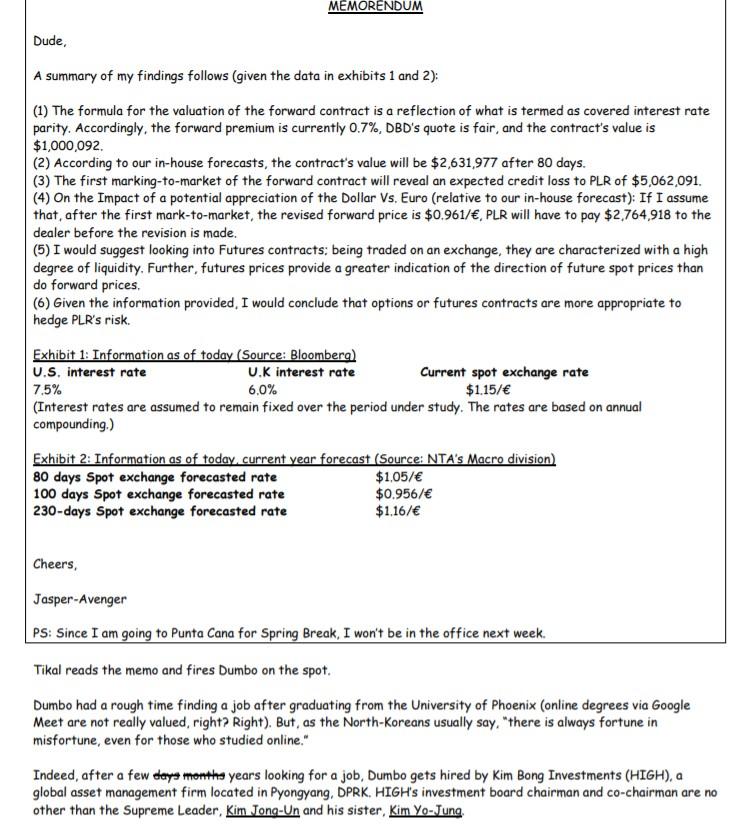

Q18: Regarding Dumbo?s Memo to Tikal, after 80 days, thecurrency forward value is closest to: A. -$2,631,977

Fantastic news! We've Found the answer you've been seeking!

Question:

Q18: Regarding Dumbo?s Memo to Tikal, after 80 days, thecurrency forward value is closest to:

A. -$2,631,977

B. $2,521,898

C. $2,631,977

Q19: Regarding Dumbo?s Memo to Tikal, after 100 days, the creditloss estimate on the forward contract is closest to:

A.0.5M

B.1.5M

C.4.9M

Q20: Regarding Dumbo?s Memo to Tikal, after 100 days and giventhe revised forecast of 0.961, the currency forward value isclosest to:

A. $4,713,701

B. $4,848,490

C. $4,900,912

Expert Answer:

a Critically damped system The steadystate error for a critically damped system can be calculated us... View the full answer

Related Book For

Analysis and Design of Analog Integrated Circuits

ISBN: 978-0470245996

5th edition

Authors: Paul R. Gray, ? Paul J. Hurst Stephen H. Lewis, ? Robert G. Meyer

Posted Date: