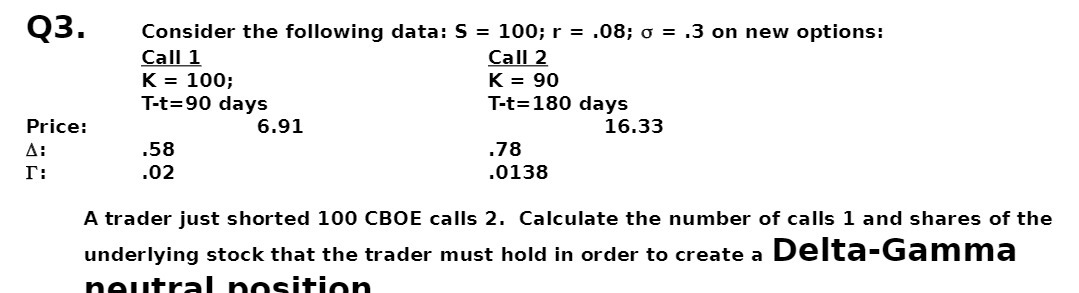

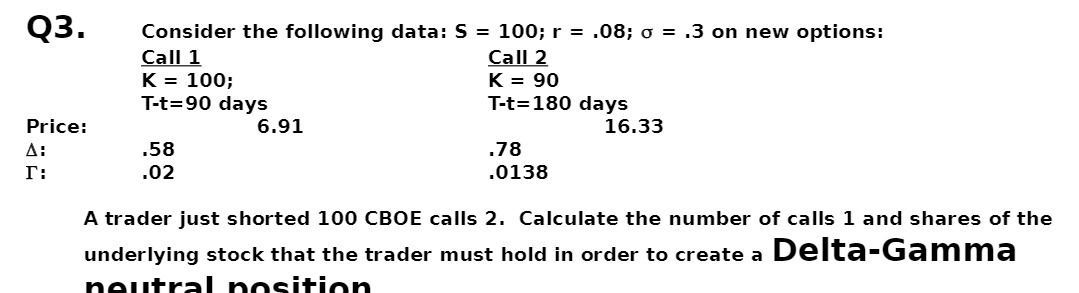

Question: Q3 . Consider the following data : 5 = 100 ; 1 = 1 08: 0 = 1 3 on new options : Call 1

Q3 . Consider the following data : 5 = 100 ; 1 = 1 08: 0 = 1 3 on new options :" Call 1 Call 2 K = 100 , K = 90 T- 1 = 90 days T- 1 = 180 days Price : 6. 91 16. 33 A` .58 . 78 I ' 1 02 . 0138 A trader just shorted 100 CBOE calls 2. Calculate the number of calls I and shares of the underlying stock that the trader must hold in order to create a Delta - Gamma citie

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock